Dollars and sense of downsizing

Don't expect a windfall if you sell your home to downsize

Advertisement

Don't expect a windfall if you sell your home to downsize

If you missed the last blog, I wrote about my godmother who chose to downsize from her 4-bedroom home in Aurora, Ont. to a 2-bedroom rental apartment in North Toronto, a little over 15 years ago.

What prompted her decision was the realization that she was spending money on a home she lived in for only half the year (she still travels extensively across North America).

But for most retirees the decision to downsize isn’t simple. In a 2013, Leger Marketing poll, less than half (43.5%) of Baby Boomers (those born between 1947 and 1966) were interested in moving to a smaller home in their retirement. Of those that did plan on downsizing, 74% cited reduced maintenance, while 48% wanted the extra money the sale of their family home would produce.

My last blog post asked a couple of questions about your lifestyle. Now, to help you sort through the financial aspect of downsizing, I’ve compiled a list of five questions. The answer to each question should move you a step closer to deciding whether or not downsizing is right for you.

#1. Look at your budget For most people their home is their biggest asset, it’s also their biggest expense. In order to appreciate how much you spend on housing, you’ll need to sit down and look at (or create) a budget. If you’ve never built a budget, or you want to help, consider the following reputable sources: Gail Vaz Oxlade’s Guide to Building a Budget, or you can use her online budget form. For tips on creating a balanced budget go to GetSmarterAboutMoney.ca.

If you find that a large portion of your current budget goes to maintaining your home, then it might be wise to consider downsizing—even if you don’t need the money. “If it makes sense to downsize, don’t wait,” explains Steven Sass, an associate director at the Boston College Center for Retirement Research. Sass finds there are two majory reasons retirees are reluctant to pull the trigger and downsize. The first is the erroneous notion that trading a mortgage-free home for a rental apartment or condo with fees will cost more. The second is the idea that kids and grandkids want to stay in old rooms when they visit. “Rather than clinging on to a three-bedroom and paying for the maintenance and heating, it’s cheaper to put relatives up in a hotel room.”

Thankfully downsizing isn’t a zero-sum game. You don’t have to give up a guest room, or family visits, if you opt for a smaller place. Instead, it’s about determining what you pay in your current budget—since even mortgage-free homes cost money—and how much you will realistically pay if you were to downsize. According to Sass, even a mortgage-free home will cost approximately 30% of a retiree’s expenses. Even if you end up paying monthly rent or condo fees, you’ll probably still come out ahead with just the reduction in your utility bills (not to mention the added ummphh a lump sum contribution will have on your nest egg rate of return).

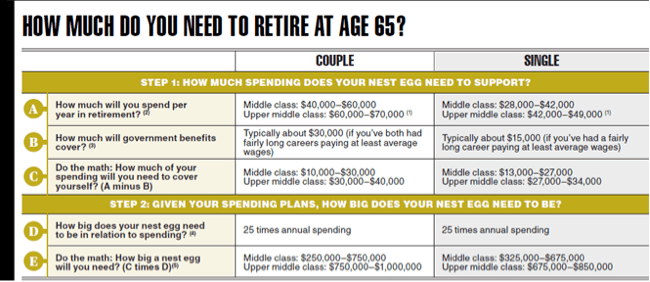

#2. How long will your nest egg last? Ask 10 retirees how big their retirement nest egg needs to be and you’ll get 10 different answers. That’s because we all have different financial circumstances and we all have different retirement aspirations—a one-size fits all answer just doesn’t work.

What will work is determining how long your nest egg will last. First, figure out how much you’ll be drawing from your nest egg each year when you retire. Then, figure out how big your nest egg needs to be. A great summary of this calculation is in the chart below (taken from a Canadian Business article, found here, or go to MoneySense’s own David Aston article).

What this calculation will tell you is whether or not selling your current family home is a necessity, or not. If you have a shortfall then the decision is simple—though probably not easy—you have to sell. If you aren’t in dire need of the extra funds, like my godmother, then you’ll need to determine if your lifestyle should prompt the move and allow you to enjoy the extra funds.

What this calculation will tell you is whether or not selling your current family home is a necessity, or not. If you have a shortfall then the decision is simple—though probably not easy—you have to sell. If you aren’t in dire need of the extra funds, like my godmother, then you’ll need to determine if your lifestyle should prompt the move and allow you to enjoy the extra funds.

#3. Will I benefit from the sale of my current family home? To determine whether or not you’ll benefit from the sale of your family home, consider the following calculations:

→ How much is your home worth in the current housing market? If you’re not sure, ask one or two real estate agents for a market comparison. Realtors will gladly give you this ballpark figure for free, as you may be a future client for them. Ask for a written market comparison, that way you know the realtor has examined comparable homes in your area before determining the proposed list price. Remember, though, this is an initial analysis, so the actual sale price may go up or down, depending on when you list for sale, how your home shows, and a variety of other factors.

→ How much money will you pocket from the sale of your current home? Here’s the good news: Any profit you make from the sale of your primary residence is tax-free. Yup. That’s pure profit in your pocket. But before you break open the bubbly, you’ll have to understand that other expenses will eat into your lump sum.

For illustration purposes, let’s assume your current home will sell for $450,000. If you are mortgage-free, that’s $450,000 of tax-free money in your pocket. However the sale of your home will incur transactional costs. These include:

*realtor commissions (between 1% and 7%, depending on where you live in the country and what you can negotiate. For a $450,000 home in Toronto at the 5% standard realtor rate, you’ll end up paying your realtor $11,250 and the buyer’s realtor $11,250.) *closing costs legal fees (approximately $1,500) *miscellaneous costs (approximately $1,000)

Given these expenses, you’ll be left with $425,000 after you sell your home. But you won’t have a place to live, and this is where you’ll need to make some decisions.

#4. Where I’m going to live? If you’ve been a home owner for most of your adult life, you’ll probably assume that downsizing means selling your current home and buying a smaller home (or townhome, or condo-apartment). But downsizing doesn’t have to mean re-buying property. Like my godmother, it can mean trading in the title to a piece of land for a lease in a well-appointed apartment building. To help you determine the best fit for your needs consider the following:Option #1: Buy a condo-apartment, townhome or smaller home If you absolutely cannot adjust to the idea of paying rent then buying a smaller place may be the only option for you. But this will mean you will not benefit from a large lump sum addition to your retirement savings, as most of the money you earn from the sale of your home will be spent on the purchase of your retirement home. Keep in mind, however, that once you downsize you’re also cutting your monthly housing costs as smaller homes require less maintenance and cost less to heat and cool. To get an idea as to what a downsized place would cost, consider these expenses:

*purchase of two-bedroom condo (approximately $350,000) *land transfer tax on new place (approximately $7,000 if you live in Toronto) *title insurance and legal fees (approximately $1,500) *moving costs (approximately $3,000) *property tax adjustments ($2,000) *cost of new furniture and appliances (at approximately $10,000)

That means after paying all these expenses, you will have $51,500 in your pocket. While it doesn’t sound like a lot, remember, you’re still mortgage-free and you’ve cut your monthly housing expenses by moving into a smaller place. Plus, there’s still some money left to be invested: Based on a 4% return, that $51,500 will earn you an extra $172 per month, or $2,064 each year.Option #2: Rent an apartment My godmother thought long and hard before she sold her Aurora, Ont. home. She wasn’t reluctant to move, she just wanted to make sure that the choice she made for her retirement home would fit both her lifestyle and budget. While she could’ve easily bought a condo (there are plenty in her Bayview community) she just didn’t like the idea of paying maintenance when she was at home only 50% of the time. She’s not alone in her logic. Parent’s of a good friend of mind have been renting a two-bedroom apartment in Newmarket, Ont. for the last 10 years. Rather than invest in a city-home, they opted to buy a vacation-home in the Muskoka-area of Ontario’s cottage country. They love it. They literally lock their apartment door, leave for weeks at a time, and never worry about burst pipes, or maintenance upgrade condo meetings, or shovelling snow, well, you get the gist.

It’s the psychological transition from home owner to renter that is often the hardest leap to make, but by crunching the numbers you may see an incentive to paying someone else’s (massive!) mortgage.

Based on our example, you would still have to factor in costs associated with moving to an apartment, such as:

*First and last month’s rent cheque (approximately $1,800 each, or $3,600 total) *moving costs (approximately $3,000) *cost of new furniture and appliances (at approximately $10,000)

These expenses would cost you $16,600, leaving you with a $408,400 in your pocket. Based on a 4% return, you’ll earn an extra $1,361 per month, or $16,332 each year. Of course, you won’t be mortgage free, you’ll need to factor in $21,600 in rent payments each year (and even if rent appreciates with inflation, at a standard 2% each year, that’s still only a $36/year increase in the first year).

Whether you end up buying or renting, your retirement residence should accommodate you, your lifestyle, and your needs both now and in years to come. More than money is at stake in this decision, says David Schwartz, chief executive at New York’s advisory firm FCE Group. Many of Schwartz’s clients move from suburban houses to apartment complexes because of lifestyle, not money. He states that onsite shopping, easy access to restaurants and transit are the main reasons his clients sell their large family home to move into a smaller or more urban residence in retirement.

If you’re thinking of renting or buying consider what is available, and at what cost, based on your needs. For instance, if you want to interact and socialize with people your age consider an age-restricted building; if you travel a lot, consider a place conveniently located near the airport or highway; if you enjoy the downtown art-scene, pick a place that’s convenient to opera houses, theatres and art galleries. The key is to pick a place that logically satisfies both your lifestyle and your finance.

Stay tuned for my tips on how to plan your downsizing move.

Like Romana King’s Home Owner on Facebook »Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Accessible home renovations can cost tens of thousands of dollars. Learn about grants, tax credits, and practical ways to...

Learn what condo fees pay for, why they rise over time, and how to assess a building's financial health...

If your landlord defaults and the home is sold, your tenancy may still be protected—but rules vary by province....

Thinking of selling your home without a Realtor? Here’s what DIY sellers need to know about commissions, legal risks,...

Short-term rentals can help cover housing costs, but experts say many first-time hosts underestimate the legal, financial, and lifestyle...

As falling home prices leave more Canadians underwater on their mortgages, experts explain the refinancing and renewal options available.

Buying a home can change your life insurance needs fast. Here’s how much coverage young Canadians may actually need—and...

Bank of Canada holds its 2.25% rate for a fourth time amid inflation risks from oil prices, affecting mortgages,...