Condo overbuilding in Canada

Increasing cranes in the skyline is not anecdotal proof of overbuilding

Advertisement

Increasing cranes in the skyline is not anecdotal proof of overbuilding

I’m not at all surprised that our government-backed housing agency—the Canada Mortgage and Housing Corporation—is warning condo builders to sell more of their current inventory before building more condos.

But I don’t think it’s a signal we’re overbuilding. I think it’s a signal that the government doesn’t want another close call.

From the late 1990s to 2008, the government loosened housing and mortgage policies. For instance, the government lowered down payment requirements so that home buyers could avoid default insurance (otherwise known as mortgage insurance); the government also introduced 35-year and 40-year amortizations and introduced government backed 100% financing—even for rental properties; and income documentation to obtain a mortgage was far more lenient than it is today. Then the U.S. housing market took a dive and the 2009 world wide credit crunch made everyone take a step back—including our government.

As such, policies were introduced to tighten up the lax regulations that were previously introduced by the government. This included putting our national $600-billion insurance company, otherwise known as the CMHC, under the watchful-eye of the banking and insurance regulator (the Office of the Superintendent of Financial Institutions).

So…? What does this have to do with CMHC’s recent warnings to condo-developers to slow down on building? It’s the next move in the government’s attempt to reduce any and all exposure it has in Canada’s continually robust housing market. It’s taxpayer money, so this is exactly what the CMHC and the government should be doing—staying conservative. But that doesn’t mean we’re overbuilding.

I recently spoke to Marc Pinsonneault, senior economist with the National Bank of Canada, about the supply of condos in Canada’s big cities. Based on his analysis, there is overbuilding in the Canadian condo market—but not in the cities you’d expect.

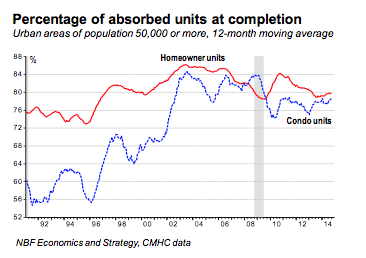

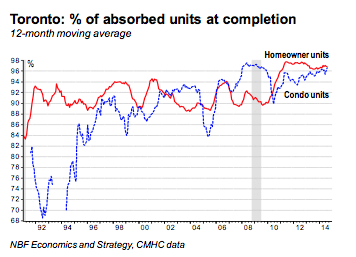

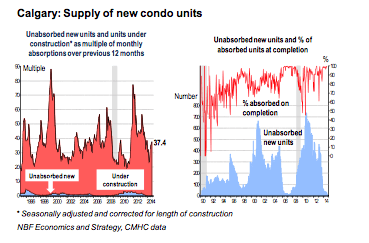

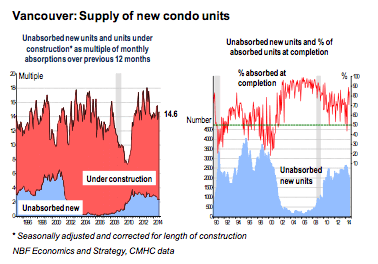

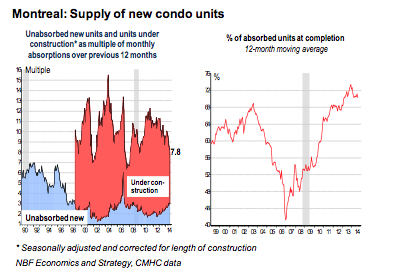

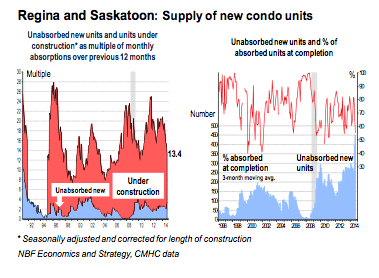

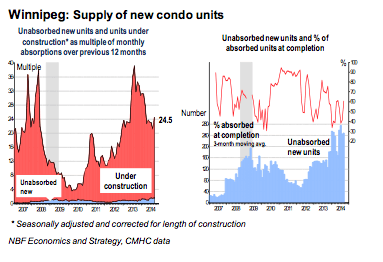

According to Pinsonneault developers are not overbuilding in Toronto, Vancouver or Calgary. However, buyers in Montreal, Saskatoon, Regina and Winnipeg should be careful as developers have overbuilt for these markets, explains Pinsonneault.

A little surprised? I was, particularly given all the commentary about overbuilding in Canada’s three hottest real estate markets. So, how can so many analysts—both within Canada and from international organizations—be so wrong? “It’s all about context,” says Pinsonneault.

When you examine permit applications and building starts we see that the numbers are increasing. Add context to these numbers and we see the bigger picture: Supply is actually keeping up with demand.

DEFINING THE TERMS

Before I jump in and qualify that last statement, I first want to get a few definitions in place.

Housing starts: Measures all developments that have actually started being built. This measurement can be broken down into condo units or freehold units (otherwise known as homeowner units).

Unabsorbed units: This is the number of unsold condos that are currently in the market (often in developer hands). This is measured in terms of real numbers—as in there are 35,000 unabsorbed units currently in the Montreal marketplace—as well as through a length of supply, as in there are two months of unabsorbed units, which means if no other condos are built, it will take approximately two months to sell off existing unsold inventory.

Absorption rate: The rate at which available homes are sold in a specific real estate market during a given time period, usually a 12-month period. It is calculated by dividing the total number of available homes by the average number of sales per month.

Part of the reason why developers have not overbuilt in the three hottest markets in Canada is because demand is high in all three cities. But even from a national perspective demand, in general, is keeping up.

“In Canada as a whole, the number of completed and unabsorbed condo units amounts to only two months [worth of supply], versus the more than four months [of unabsorbed condos that existed] in the 1990s,” explains Pinsonneault.

But could this mean we’re heading into dangerous territory? Wasn’t there a housing bubble and a nationwide price correction in the 1990s and could that happen today? Not likely, says Pinsonneault.

While the quantity of unabsorbed condo units is back up to where it was just before the 1990s housing crash, this number doesn’t take into consideration the “growing importance of the condo market in the last 20 years,” says Pinsonneault. “The rising popularity of condos means that the market is now absorbing almost twice as many new condo units annually as in 1990.” While there may be the same number of unsold condos as there were 20 years ago, demand for these unsold units has more than doubled in the last two decades.

To get an idea of how increased demand in condos has changed the landscape of housing starts in Canada, take a look at this chart from the National Bank of Canada (below):

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Is your salary enough to buy a home in these Canadian cities? Here’s how much you needed to earn...

Learn how to choose a professional appraisal firm in Canada. Get tips on credentials, local expertise, services, and reliable,...

Planning a move to a new city involves budgeting, accounting for hidden costs, and using expert advice to navigate...

From micro-apartments to co-living, Gen Z is finding clever ways to balance cost, convenience, and lifestyle as offices reopen.

GTA housing sales up 8.5% in September as prices decline, with falling interest rates encouraging more buyers into the...

Our “Where to Buy Real Estate in Canada 2025” survey turns up a wealth of cities and neighbourhoods with...

Sponsored By

Coast Capital

Created By

Ratehub

A MoneySense reader asks about survivor benefits for spouses. Here’s how defined benefit and CPP survivor payments work in...

If you’re thinking about buying your first recreational property, now may be the right time. Here's what to know.