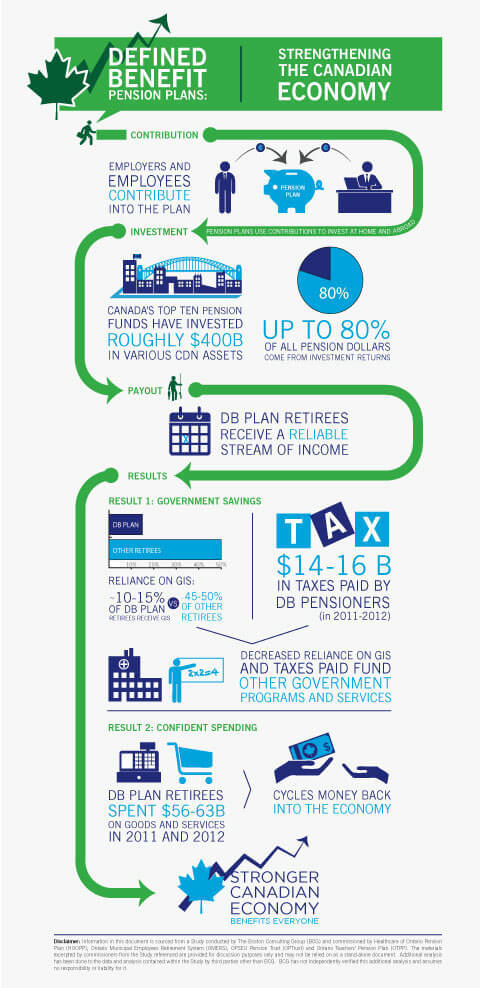

Defined-benefit plans are great: We already knew that

However attractive defined-benefit pension plans are for employees, many employers just don't want to bear the burden any longer.

Advertisement

However attractive defined-benefit pension plans are for employees, many employers just don't want to bear the burden any longer.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

To have liquidity and reduce taxes, Canadians can move money between registered accounts. But what are the tax, contribution...

Here’s how Canada’s Old Age Security pension works, who’s eligible for OAS, when you can start receiving OAS, and...

Here’s how Canada’s retirement pension plan works, who’s eligible for CPP, when you can start receiving CPP, and CPP...

Tax planning in Canada isn’t just for March and April. These smart tax moves need to be made before...

Allison resold her Eras Tour tickets instead of going to the concert. The resale website asked for her SIN,...

Contrary to the conventional advice, taking more than the minimum RRIF withdrawal can at times save tax on your...

Practical advice on how to build your retirement savings for employees at mid-career, the self-employed, single parents and more.

While not guaranteed like an annuity, MyRetirementIncome is a flexible and simple financial product for those needing to convert...

A Certified Financial Planner provides perspective on the TFSA vs. RRSP question for a couple in their late 50s...