Skating on thin ice: The story of a single dad

A single dad tries to find a way to help his teenagers pay for university and still save money for a modest retirement.

Advertisement

A single dad tries to find a way to help his teenagers pay for university and still save money for a modest retirement.

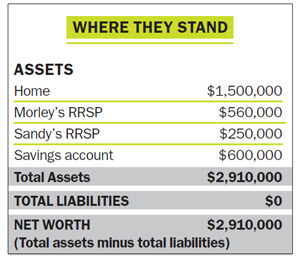

Garbens, meanwhile, thinks George should sell the house. “He should take the money he clears from selling the house (about $36,000 after commissions and legal fees) and pay off his $24,000 car loan,” she says. That will leave him with $12,000. Garbens advises George to leave $6,000 in an emergency fund and put the remaining $6,000 into the RESP for the kids. “He’d get the 20% government grant,” says Garbens. “That’s free money for the kids and it would be a shame not to claim it for them.”

Set up pre-authorized monthly payments. Both experts feel George needs a forced savings plan once he sells his home. After selling the house and paying off his car loan, George will have disposable income of $10,645 annually (the $2,145 his budget shows now, plus $5,500 from annual car loan savings, and about $3,000 from renting instead of owning). Garbens advises George to put half that surplus into RESPs for his kids each year until they’re no longer eligible for the government grant. He should direct the other half into his own RRSP. “He should set up a pre-authorized monthly contribution from his savings account,” Garbens says. “This will allow him to save a decent amount of money for his kids’ post-secondary education. If they need more, they can get it through loans and part-time jobs.”

Keep investing simple. George can reduce his mutual fund fees and get broad diversification in his RRSP with a simple balanced fund that should reward him with a decent 4% annual return over the long run. “Pick one good balanced fund and reinvest all the dividends,” says Garbens. “He’ll do just fine.”

Focus on retirement savings when the nest is empty. When Lucas and Patrick head off to university in five years, George won’t have to foot the $6,500 bill for the kids’ activities. The $5,000-plus he was putting into RESP savings will also end. He should redirect most of that money to his TFSA and RRSP for the next 15 years, until he’s 65. If he can do that, George will be able to retire at age 65 with enough to fund a simple but comfortable lifestyle.

Julie Cazzin is an award-winning business journalist and personal finance writer based in Toronto. Read previous Family Profiles and other stories by Julie.

Garbens, meanwhile, thinks George should sell the house. “He should take the money he clears from selling the house (about $36,000 after commissions and legal fees) and pay off his $24,000 car loan,” she says. That will leave him with $12,000. Garbens advises George to leave $6,000 in an emergency fund and put the remaining $6,000 into the RESP for the kids. “He’d get the 20% government grant,” says Garbens. “That’s free money for the kids and it would be a shame not to claim it for them.”

Set up pre-authorized monthly payments. Both experts feel George needs a forced savings plan once he sells his home. After selling the house and paying off his car loan, George will have disposable income of $10,645 annually (the $2,145 his budget shows now, plus $5,500 from annual car loan savings, and about $3,000 from renting instead of owning). Garbens advises George to put half that surplus into RESPs for his kids each year until they’re no longer eligible for the government grant. He should direct the other half into his own RRSP. “He should set up a pre-authorized monthly contribution from his savings account,” Garbens says. “This will allow him to save a decent amount of money for his kids’ post-secondary education. If they need more, they can get it through loans and part-time jobs.”

Keep investing simple. George can reduce his mutual fund fees and get broad diversification in his RRSP with a simple balanced fund that should reward him with a decent 4% annual return over the long run. “Pick one good balanced fund and reinvest all the dividends,” says Garbens. “He’ll do just fine.”

Focus on retirement savings when the nest is empty. When Lucas and Patrick head off to university in five years, George won’t have to foot the $6,500 bill for the kids’ activities. The $5,000-plus he was putting into RESP savings will also end. He should redirect most of that money to his TFSA and RRSP for the next 15 years, until he’s 65. If he can do that, George will be able to retire at age 65 with enough to fund a simple but comfortable lifestyle.

Julie Cazzin is an award-winning business journalist and personal finance writer based in Toronto. Read previous Family Profiles and other stories by Julie.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Tax season can push Canadians deeper into debt as many rely on refunds. Here’s why it’s happening, and how...

The first quarter finally broke the pattern of steadily rising markets, but energy stocks soared.

Robert has been taking RRIF withdrawals beyond the minimum required amount to gift to his kids and to reinvest...

Geopolitics, rising oil prices and ETF inflows are shaping Bitcoin’s outlook. Is now the right time for Canadian investors...

Wealthsimple's direct indexing brings a tax-saving investing strategy to a wider group of investors, but the number likely to...

A University of Calgary study found that over one-third of senior homeowners worry about affording basic home maintenance, suggesting...

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

Whether you want the highest interest rate or no service fees, these savings accounts will meet your needs.

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...