Where does the down payment come from?

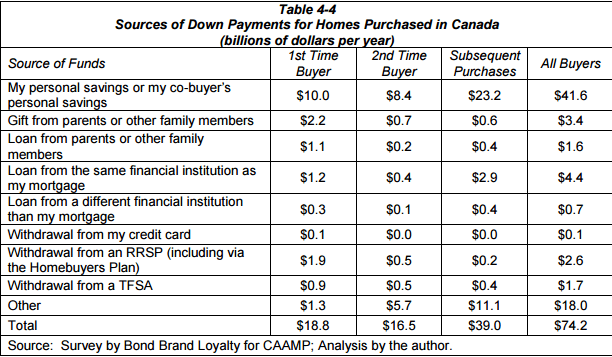

Here's a breakdown for down payment money

Advertisement

Here's a breakdown for down payment money

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Created By

Ratehub.ca

The Bank of Canada holds its key rate steady amid the U.S. trade war and economic uncertainty.

Whether you have renters in your home or another property, know that the money you make can affect your...

Here’s how proposals from the NDP, Liberals, Conservatives and Green Party could affect your cash flow—and maybe help decide...

What to consider when deciding to incorporate a company with friends to buy real estate and more.

Sponsored By

Coast Capital

Can you retroactively change the valuation of a rental property before selling it to reduce capital gains tax in...

On the heels of a pandemic boom, the recreational real estate market has slowed. But property prices are still...