The “final hurrah” of Vancouver’s home prices?

Despite a slower sales pace, Vancouver home prices still posted double-digit growth, as did other markets in Canada

Advertisement

Despite a slower sales pace, Vancouver home prices still posted double-digit growth, as did other markets in Canada

As predicted at the start of this year, Canada’s residential real estate market continued to grow in the third quarter of 2016. But we’re probably near the end of Vancouver’s “expansionary cycle,” says Royal LePage CEO, Phil Soper.

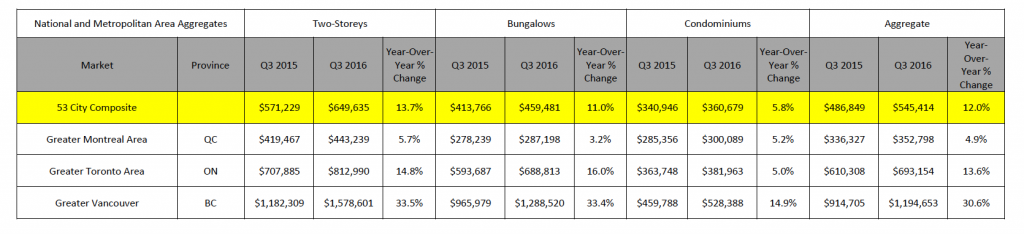

According to the Royal LePage House Price Survey, the price of a home in Canada increased 12.0% year-over-year to $545,414 by the end of the third quarter in 2016.

The largest price increase was in the much-sought after single family detached, which are dominated by two-storey homes. As such, the year-over-year increase for a two-story rose 13.7% to $649,635, while the price of a bungalow increased 11.0% to $459,481. During the same period, the price of a condominium increased 5.8% to $360,679.

But the real news is that Vancouver home buyers may finally be seeing the tail-end of almost a decade of hot housing prices.

“In what may be a final hurrah for this expansionary cycle, Greater Vancouver posted another quarter of unsustainably high price appreciation,” Soper stated in a press release. According to the Royal Lepage house price composite, the median value of homes in the “tiny West Vancouver suburb” increased by nearly 40%, year-over-year. That’s “an astonishing million dollar” gain in just 12 months, explained Soper.

But there’s hope, said Soper. The number of homes actually trading hands has been declining for months, and “slower sales volumes lead to moderating prices.”

One contributing factor to the slower sales pace in Vancouver was the Government of British Columbia’s new 15% property transfer surtax on foreign nationals and foreign-controlled corporations, introduced early in the third quarter. But even with the slower pace of sales, prices have yet to drop. In fact, the west coast city actually led the country in year-over-year appreciation with home prices increasing by 30.6% in the third quarter.

Over the same time period, house prices increased in the Greater Toronto Area (GTA) by 13.6%.

“Nationally, our real estate markets remain healthy, with home values showing modest to strong (yet rational) price appreciation in almost every Canadian city,” Soper said. “Even in the hardest hit oil patch regions, prices have held up well, with small single-digit declines, year-over-year.”

Vancouver posted an aggregate 34.1% year-over-year house price increase to $1,464,507.

West Vancouver posted a year-over-year price increase of 39.6% to $3,411,578.

Victoria posted an aggregate 8.8% year-over-year house price to $537,228.

Kelowna posted an aggregate 10.9% year-over-year house price to $554,289.

This western province continues to face a slowdown in the energy sector and most analysts continue to predict further economic contractions of about 2% in 2016. This makes it one of the most significant downturns in the province’s history and this economic drop has directly impacted housing prices in the province’s key markets. But not nearly to the degree many observers anticipated.

Calgary posted a -1.6% year-over-year drop to $457,044, while Edmonton posted a -3.1% to $374,712.

Similar to Alberta, this energy-dependent province was also hit by the downturn in the resource sector. Effects can be observed in the employment sector, as the province lost 6,500 jobs in September when compared to the same period in 2015. Employment insurance recipients are up, earnings are falling and payroll employment is down. Despite the traditionally negative effects of a poor economy on the housing market, the region’s home prices have remained relatively stable.

Aggregate house prices in Regina increased year-over-year by 0.6% to $332,540.

As predicted, this province is relatively strong and remains on track for expansion through 2017 and this favours well for the bigger real estate markets in this province, particularly for the City of Winnipeg. City officials announced that the city will surpass the one-million resident mark by 2035. Demand for housing with grow as a result.

This province continues to be one of the fastest growing economies in Canada. Concerns about the fate of the U.S. economy have kept employers cautious about hiring, ultimately slowing the economic gains expected for the region, but that hasn’t dampened home valuations.

GTA posted an aggregate house price growth of 12.1% to $714,002.

Kitchener/Waterloo/Cambridge are also appreciating, posting a year-over-year increase in aggregate house price of 9.1% to $371,474.

Hamilton, which stands above the provincial average in retaining and attracting millennials, had year-over-year growth in its aggregate house price of 10.3% to $419,830.

Ottawa saw moderate year-over-year growth of 3.6% to $411,654.

The Belle Province continues to maintain a steady economy, despite export volumes coming in below expectations. Better still, Quebec’s unemployment rate in September sat below the national average and the province has recently been showing solid job growth.

Greater Montreal Area home prices increased by 4.9% year-over-year to $352,798.

The eastern provinces saw mixed results, with Newfoundland and Labrador conceivably falling into recession as a result of challenges associated with the energy sector downturn.

St. John’s saw a decline in aggregate home prices by -3.2% to $332,597.

Moncton posted a small increase in home prices at 1.5% to $182,529.

Halifax also showed slight year-over-year increase in aggregate house prices of 0.8% to $308,017.

Charlottetown increased year-over-year by 2.3% to $224,219 and 2.9 per cent to $246,696, respectively.

Fredericton posted a 2.9% to $246,696.

The Royal LePage National House Price Composite is compiled from proprietary property data in 53 of the nation’s largest real estate markets.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Sponsored By

Coast Capital

Can you retroactively change the valuation of a rental property before selling it to reduce capital gains tax in...

On the heels of a pandemic boom, the recreational real estate market has slowed. But property prices are still...

How much can you afford on your first home? Should you buy or continue renting? We answer these questions...

When is capital gains tax payable on the sale of property? And at what rate are capital gains taxed?...

You have so many options for finding the best mortgage rate for you. Here’s how you can compare some...

Here are the considerations before becoming a power of attorney for property and what to do if you’re unable...