Making sense of the markets this week: July 10

The worst start for markets since 1962, rate-hike fears, the pending real estate collapse and bank brokerages hide high-interest savings ETFs.

Advertisement

The worst start for markets since 1962, rate-hike fears, the pending real estate collapse and bank brokerages hide high-interest savings ETFs.

This week, Cut the Crap Investing founder Dale Roberts shares financial headlines and offers context for Canadian investors.

The S&P 500 entered a bear market last month and recorded its worst first half since 1962, down 20.6%. The NASDAQ fell almost 30%, while the S&P/TSX Composite ended the first six months down 11%.

And of course, there was no safety in bonds. Thanks to rising rates, bonds did not go up in price as stocks got crushed. Central bankers turned hawkish to combat inflation. Yields on global bonds rose from an average of 1.3% on January 1, 2022 to 3% by the end of June, leading to a 14% drop in global bond returns.

Here’s a table outlining the returns for Canadian sectors, factors and bonds. You’ll also find broad international equity markets for comparison. All are listed in Canadian dollars (CAD).

As for U.S. sectors, you’ll find these in this Liz Sonders tweet.

The defensive sectors are doing as promised.

We are now seeing more attractive valuations for equities and bonds. The one-year forward price-to-earnings (P/E) multiple for the S&P 500 dropped from 21 times at the start of the year to around 16 times last month. (Since 1990, the median multiple is 15.4 times.)

That said, with economic growth slowing down, this could be a headwind for corporate profits.

Earnings season starts next week.

According to its Q3 outlook report last month, BlackRock is positioning portfolios “more defensively.” The asset manager recommended a “barbell” strategy (balancing assets, such as holdings for corrections and recessions). “The optimal portfolio to combat inflation is very different from the optimal portfolio for a recession,” it said. Energy and financials can serve as inflation fighters, while health care provides “a dose of resilience.”

I’d add consumer staples, utilities and pipelines to that list of defensive holdings.

And speaking of defense, bonds are getting some love again.

Bond yields are more attractive, so bonds might start being bonds again. Bonds should benefit as—rather, if—recession risks start to outweigh inflation concerns.

Scott Barlow shared this on Twitter. (FYI: 1H represents the first half of 2022, 2H the second half of 2022.)

“Historically, a negative 1H has led to a negative 2H 44% of the time, vs. just 19% when 1H was positive…”

Need some good news? Rare these days, I know.

Despite a multitude of factors—including historically high levels of inflation, recession fears and year-to-date asset losses—the funded positions of most defined benefit (DB) pension plans improved during the second quarter of 2022, according to the Mercer Pension Health Pulse (MPHP) study. That includes CPP, too.

The MPHP, which tracks the median solvency ratio of the DB pension plans within Mercer’s pension database, increased from 108% as at March 31, 2022, to 109% as at June 30, 2022.

Here is the mid-year review of the Beat The TSX Portfolio. Simple rules-based BTSX beats the thinking of experts such as the John Heinzl portfolio, writes Matt Poyner at dividendstrategy.ca.

The high-yield dividend strategy has had a good run in Canada and in the U.S. in 2022. I also track the Beat The TSX Portfolio on my blog.

A few banks in Canada do not offer high-interest savings (cash) exchange-traded funds (ETFs) at their discount brokerages. The discount brokerages at Royal Bank of Canada (RBC Direct), Bank of Montreal (BMO InvestorLine) and Toronto-Dominion Bank (TD Direct) don’t offer cash ETFs. Why not? Who knows, but I do know these cash ETFs would compete with the banks’ own paltry “savings” accounts that pay next to nothing with respect to interest rates.

I connected with Mark Noble of Horizons ETFs over email. He says if you’re a TD client, you can call in to access cash ETFs, but you would not be able to purchase them online.

That’s similar to the TD e-series index funds listed in the Canadian Couch Potato series. They are a wonderful option, but good luck getting a TD advisor to help you find them.

“Scotiabank, CIBC and National Bank are offering these cash ETFs, as well as all of the non-bank owned discount brokerages” wrote Noble.

The above situation is “curious” as investors can access higher-risk offerings from the bank discount brokerages.

Noble wrote me this via email:

“Restrictions on ETFs have been commonplace in the full-service channel (ie: IIROC licensed advisors) since there are regulatory and fiduciary obligations that can make offering some ETFs (ie: leveraged ETFs, Marijuana ETFs and cryptocurrencies) difficult. These restrictions have never historically been in place at the self-directed brokerages, where effectively investors have been able to buy any Canadian-listed ETF.”

Here are a few considerations on cash ETFs vs holding a high-interest savings account (HISA) or guaranteed investment certificates (GICs) directly with a bank, such as EQ Bank. Rates have certainly taken off the last few months, with EQ Bank GIC yields well above the cash ETFs. Thanks to Mark Noble for the below details.

So with all that, know that here are six cash ETFs in Canada:

The average yield before fees is about 1.95%.

There are distinct advantages for cash ETFs with high interest savings accounts and GICs. The main point may be there are cash options that allow you to stay away from the very poor savings accounts from the major banks.

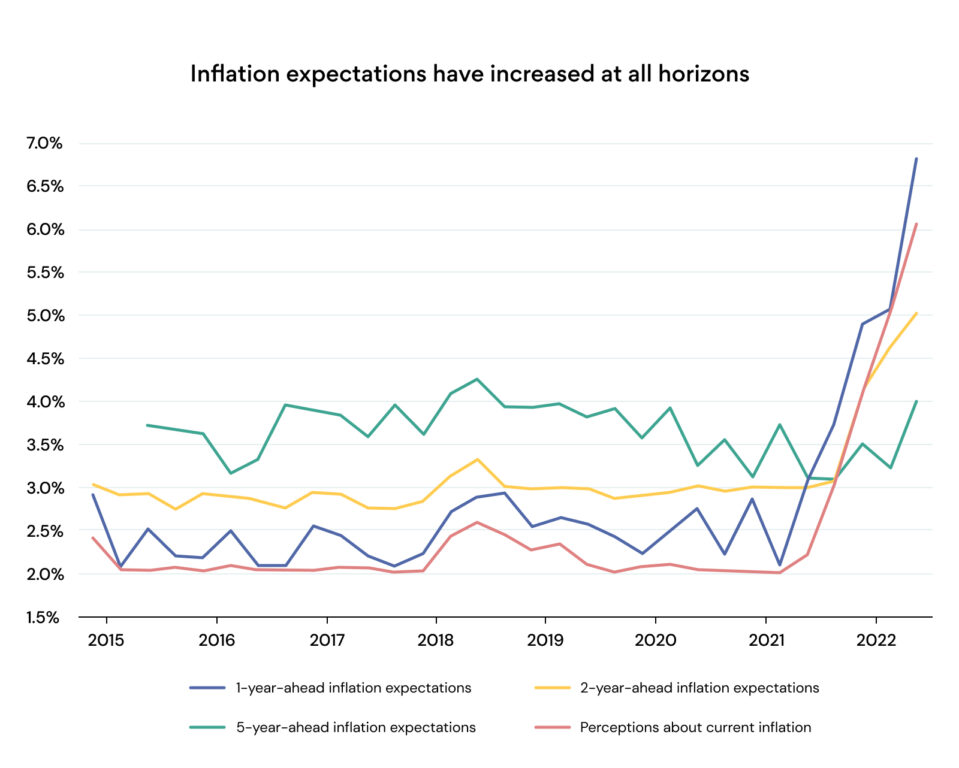

The BoC recently released two surveys—one polling consumers and the other, business leaders. Essentially the two show that Canadians are expecting higher inflation over the next year, as well as over the next three and five years.

Business leaders expect inflation will still be running at 5% a year from now. And a source of that inflation rise can be caused by wage increases.

When consumers (i.e. workers) expect higher inflation, they often demand higher wages.

The BoC will announce another rate increase next week, and it is expected that it will move rates higher by another 75 bps, or 0.75%. The rate hikes are likely to cause a recession.

CP24 cites a Canadian Centre for Policy Alternatives (CCPA) study:

“The study showed that, in the last 60 years, the central bank has in three cases managed a 5.7% reduction in the inflation rate by quickly raising interest rates, and each case was followed by a recession.”

However, past central bank performance does not guarantee future results. As I always write, anything can happen.

South of the border, the Fed released its minutes from its June meetings. The report is three weeks old and is based on economic data that is already stale. Oil and commodity prices are falling. There are many signs that consumers’ wills have been broken. The economies of the world are already slowing down and earnings projections are tumbling.

The Fed lifted its main policy interest rate by three-quarters of a percentage point last month, as it attempts to cool down consumer and business demand. The move followed a half-point increase in May 2022 and a quarter-point increase in March this year.

In its notes, Fed officials acknowledged they need to raise interest rates to a point where they would start to meaningfully weigh on economic growth.

There are hopes the Fed won’t need to be overly aggressive with rate hikes. This week the markets are signaling that possibility and are putting in a string of positive days.

I’ve suggested for several weeks now that it will not be hard to break the back of the consumer and prick the real estate bubbles, especially in Canada.

See the story below.

While no one knows how far things will go, the cracks in the Canadian real estate market are showing—and growing.

If you were looking to sell, well, you probably missed the peak prices for this cycle. You can close the door on that notion and face the new reality—real estate enthusiasm has left the building.

In Canada’s most expensive market, home sales are dropping by $2,200 per day according to this Better Dwelling article.

Most estimates I read suggest home prices could fall 15% to 20%. That’s good news if you’re a buyer. But know that you will likely face higher borrowing costs. The rising rate environment is bringing down housing prices, and that impacts the borrowing front.

The ideal situation for wannabe home buyers might be tumbling home prices and a recession. At that point, we might be looking at rates that are reduced to stimulate the economy. This is not advice as any type of market timing—even with real estate—is more than tricky, but I think that scenario will play out. If I were in the market for a home, I’d wait for a recession and falling rates. Yet, a prospective home buyer might simply watch the prices decline. And when the price and borrowing costs hit your affordability zone, go home shopping.

And be sure to check out the MoneySense complete guide for first-time home buyers.

Dale Roberts is a proponent of low-fee investing, and blogs at cutthecrapinvesting.com. Find him on Twitter @67Dodge for market updates and commentary, every day.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Here’s how Canada’s Old Age Security pension works, who’s eligible for OAS, when you can start receiving OAS, and...

Here’s how Canada’s retirement pension plan works, who’s eligible for CPP, when you can start receiving CPP, and CPP...

There’s more than one way to optimize your income after retiring. Some strategies can boost wealth, and others may...

The senior vice president of retail and wealth at Meridian shares the importance of budgeting and investing in your...

Can Gen Z really afford to retire early? Here are some ways young Canadians can rethink the FIRE approach...

Here are the considerations before becoming a power of attorney for property and what to do if you’re unable...

Here are two ways to manage the effects of tariffs in Canada, plus three statements to prepare to ensure...

Economic uncertainty, inflation and the decline of workplace pensions have left growing numbers of seniors unable to leave their...

Canadians must begin taking RRIF withdrawals the year after converting an RRSP. What happens if you convert only part...

Hey Dale, just back from a month in the UK and Ireland, spending my hard earned investment income! This year my portfolio is down 2.84

% since January 1 and is down 7.9% from its YTD high in April. All in all based on what I’m seeing, I’m quite pleased with my self determined investment strategy. It’s very much like some of your recommended portfolios. 40% banks, 20% energy, 15% utilities, 25% telecoms. It’s working and has been for 8 years. Looks like my average weighted dividend increases are 6.6%. Hopefully enough to keep me at the pace of inflation! Great catching up with your blog – always interesting and reaffirming info in there. Cheers, A

Thanks Andrew for that. And sorry I missed your comment. Very interesting on the portfolio mix. Yes many Canucks go that route. We’d be best with some other sectors and U.S. stocks IMHO.

I recently posted on the retirement stock portfolio on my blog.