Making sense of the markets this week: September 25

Stats Canada lets air out of inflation, the loonie’s performance, FedEx delivers some bad news, and how historically bad the market is right now.

Advertisement

Stats Canada lets air out of inflation, the loonie’s performance, FedEx delivers some bad news, and how historically bad the market is right now.

Kyle Prevost, editor of Million Dollar Journey and founder of the Canadian Financial Summit, shares financial headlines and offers context for Canadian investors.

It’s looking more and more like the 8.1% annualized inflation reading from June 2022 was the peak of post-pandemic price increases.

On Tuesday, Statistics Canada reported that Canada’s inflation rate cooled to 7% in August. Experts had been predicting a slight decrease to 7.3% (continuing the downward trend established by the decrease to 7.6% in July). The lower-inflation news was welcomed by several economists as proof that contractionary monetary policy by the Bank of Canada (BoC)was achieving its goal, and that the worst-case scenario of massive interest rate increases were now unlikely to be required.

The significant drop in inflation was quite unexpected after last week’s 0.1% CPI increase in the U.S.

Here are the major takeaways from Canada’s Consumer Price Index (CPI) report for August:

While hourly Canadian wages have increased by 5.4% over the past year, you don’t have to be a math whiz to note that the average pay cheque isn’t going to go as far as it did last summer.

Many investors are likely hoping this encouraging inflation data allows Canada’s central bank to show patience and restraint when it comes to interest rate raises. Generally speaking, the lower that the eventual peak interest rate is capped—and the more quickly we arrive at that point—the sooner riskier investments like equities are likely to continue their long-term climb upwards.

Meanwhile, the U.S. Federal Reserve announced on Wednesday that as anticipated, it would be hiking interest rates by three-quarters of a percentage point to the 3.00%-to-3.25% range. The news continued to accelerate the downward momentum in market prices, as the main U.S. indices finished the day down about 1.7% after being up prior to the Fed’s announcement.

One of the spin-off effects of Canada’s disinflationary momentum is that it has lowered the worth of our currency when compared to the U.S. dollar. There are a few reasons for why this is the case, but most of the movement can be chalked up to expectations for future demand for the Canadian dollar, based on how high we are forced to raise interest rates. The higher we are forecasted to raise rates, the more incentive there will be to hold onto Canadian dollars.

As you can see from the chart below, the markets are now anticipating the U.S. central bank will face more pressure to raise interest rates going forward than the BoC.

Source: Google Finance

While the Canadian dollar had a rough year, when compared to the U.S. dollar, it’s important to remember it has actually performed pretty well versus most of the other leading currencies in the world.

Here’s how the loonie has fared versus the euro, Japanese yen, Chinese renminbi and British pound:

Here are four of my takeaways in regards to the worth of the loonie at the moment:

In earnings news, it was mostly quiet on the Canadian front. FedEx, on the other hand, may wish things were quieter.

Going back to Friday, September 16, FedEx (FDX/NYSE) announced some bad news ahead of its earnings call this week. And share prices subsequently collapsed to the tune of a 21% decrease. CEO Raj Subramaniam made headlines by telling CNBC’s Jim Cramer that he expected a worldwide recession given what FedEx’s bottom line looked like. Notably, UPS and DHL didn’t have nearly the same apocalyptic view on things in their recent investor communications, so it’s quite possible that it’s just a well-compensated CEO looking to scapegoat poor performance on macroeconomic economic conditions.

On Thursday, FedEx announced USD$2.7 billion in cost cuts and the shares rose slightly on the news. Earnings per share fell 21.3% (roughly in line with what the company had warned about last week) even though revenues were up about 5.5%. Because of their guidance update last week, analyst predictions were quite accurate.

General Mills (GIS/NYSE) put out a more upbeat earnings call, as the food conglomerate posted an earnings per share beat of USD$1.11 (versus $0.99 predicted). With shares up nearly 6% on the day, and 11% YTD, the experts who advocated playing it safe with consumer staples are looking pretty smart on this one.

Despite Costco’s (COST/NASDAQ) earnings and revenue beat, the stock was down about 3% in after hours trading. This simply appears to be the result of very bearish sentiment when it comes to retailers at the moment. With earnings per share coming in at USD$4.20 (versus $4.17 predicted) and total revenues up 15% from last year, to USD$72.10 billion (versus USD$72.04 predicted) Costco is clearly benefiting from folks looking to shop in bulk as they fight inflationary cost raises. That said, the fly in the ointment was that the big-box giant was holding on to 26% more inventory than in past years.

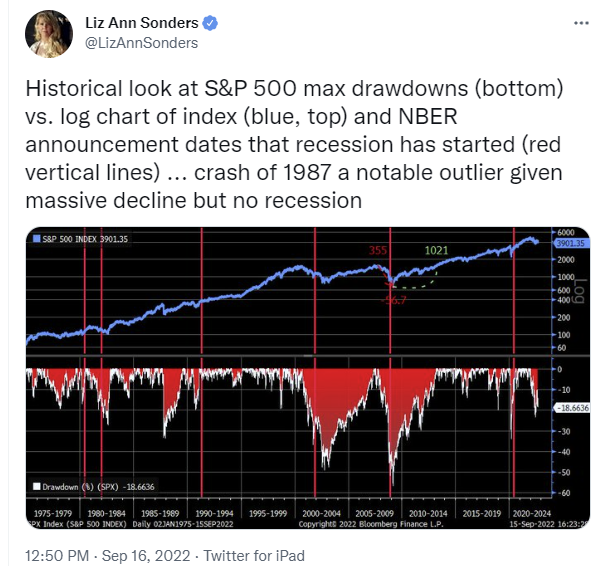

Our favourite market chart Tweeter Liz Ann Sonders, was back at it again this week with an interesting look at investor behaviour.

By comparing the value of the S&P 500 index to the amount of investments that people are selling off (a.k.a. “drawdowns”), you get a sense of how long stock-market panics have lasted in the past, and just how drastic the recent downturn has been in a historical sense.

I find this chart interesting in that I would’ve expected the recent drawdown to be substantially higher, given all the terrifying headlines out there at the moment, like “ugly recession” and comparing 2022 to 2008. Investor sentiment is down, the dominant phrases we hear from the talking heads on TV are “recession” and “stagflation.” You could think—given all the pessimism, as well as the newfound attractiveness of GIC rates—that more investors would be selling off their equity portfolios in order to get ahead of the worst-case scenario.

I suspect that more and more investors are becoming wise to how irrational market timing is for the average investor. Vanguard and Fidelity data would support my hypothesis. The rise of passive investing via robo advisors, as well as all-in-one index ETFs (more ETFs here), will very likely reward buyers who automatically maintain their target asset allocation during these volatile times.

It has been said by those much smarter than me: “It’s not market timing that matters, it’s the time in the market.” And that’s for good reason.

Kyle Prevost is a financial educator, author and speaker. When he’s not on a basketball court or in a boxing ring trying to recapture his youth, you can find him helping Canadians with their finances over at MillionDollarJourney.com and the Canadian Financial Summit.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Here’s how Canada’s retirement pension plan works, who’s eligible for CPP, when you can start receiving CPP, and CPP...

In this excerpt from her new book, Making Bank, Shannon Lee Simmons guides young Canadians (and their parents) through...

Presented By

Equifax

Presented By

Equifax

Eligible Canadians will still receive their last carbon rebate payments in April.

Here are two ways to manage the effects of tariffs in Canada, plus three statements to prepare to ensure...

Economic uncertainty, inflation and the decline of workplace pensions have left growing numbers of seniors unable to leave their...

Canada’s employers put hiring on ice in February ahead of tariff impacts.

COVID normalized remote work, but is it really here to stay in Canada?