Making sense of the markets this week: October 16

The Taiwanese company that could bring the world to its knees, positive U.S. earnings news, Canadian vs U.S. markets, and the rewards for investors that usually follow bear markets.

Advertisement

The Taiwanese company that could bring the world to its knees, positive U.S. earnings news, Canadian vs U.S. markets, and the rewards for investors that usually follow bear markets.

Kyle Prevost, editor of Million Dollar Journey and founder of the Canadian Financial Summit, shares financial headlines and offers context for Canadian investors.

It looks more and more likely that companies in North America will start to see their profits decline at some point in the next year or so. By and large though, it doesn’t appear we’re at that point just yet. (All values are in U.S. currency unless otherwise stated.)

Pepsi (PEP/NASDAQ) kicked off the earnings season with a substantial earnings beat, cashing in to the tune of $1.97 in earnings per share (versus $1.84 predicted). Revenues were also strong at $21.97 billion (versus $20.84 billion predicted). Shares were up 4% on Wednesday after the earnings report.

Delta’s earnings (DAL/NYSE) arrived on time, coming at $1.51 per share (versus $1.53 predicted) on $12.84 billion in revenues (versus $12.87 billion predicted). The massive airline credited a strong international demand (specifically to Europe) for its increased profits. Given the increased value of the U.S. dollar versus the euro and the pound, that trend should continue. Delta announced that its pre-pandemic capacity should be fully restored by next summer. Delta stock finished Thursday up 4%.

As the world’s biggest asset manager (at one point managing $10 trillion, or roughly a quarter of the entire planet’s assets), BlackRock’s (BLK/NYSE) financial health is often looked at as a bellwether for the broader economy.

While BlackRock announced a very solid quarter, it did forecast some strong economic headwinds. Earnings per share were $9.55 (versus $7.93 predicted). While the company was obviously happy to announce such a strong earnings report amidst declining expenses, revenues were down 14.6% on a year-over-year basis. Critics will note the value of assets under management slid to $8 trillion (below the $8.3 trillion predicted by analysts). Falling equities markets have evidently taken their toll on Blackrock investors, but management can’t be too worried as they announced more than $375 million in share buybacks for the quarter. Shares were up 6.63% at market close on Thursday after the earnings announcement.

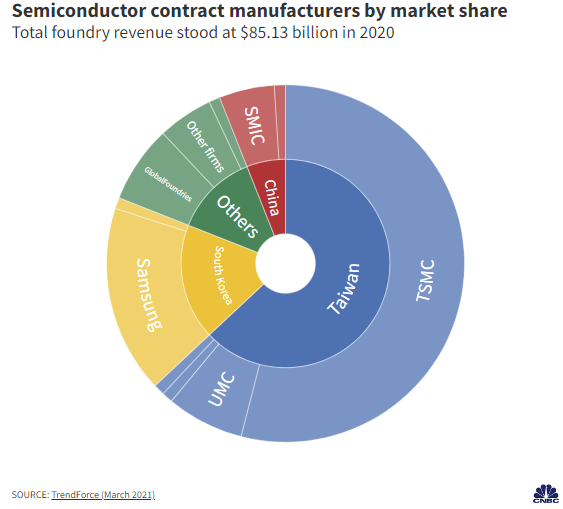

Taiwan Semiconductor Manufacturing Company (2330/TWSE) is one of the most unique companies on the planet. (You read that right, 2330 is the ticker. It also trades as an ADR on the NYSE under the ticker TSM.) As the king of semiconductors, this global behemoth supplies the world’s tech heavyweights (ahem, Apple, Intel, Nvidia and Qualcomm) with the chips needed to create hardware.

TSMC isn’t just the biggest chipmaker, it’s pretty much an island, as there isn’t even a real competitor for the company. It’s notable that the third biggest chipmaker, UMC, is also Taiwanese.

TSMC is absolutely dominant when it comes to the most advanced processing techniques. The company has roughly 55% of the global market for contract chip fabrication.

For comparison’s sake, all of OPEC (Saudi Arabia + 12 other oil-exporting countries) supplies roughly 40% of the world’s oil. TSMC is so powerful and its expertise so essential to the world economy, that it is often called “a silicon shield,” in reference to the company’s value to the Chinese supply chain. The theory is that mutually assured economic destruction might be more successful at preventing invasion than old-fashioned kinetic deterrents.

Given the market cap of the company is roughly $327 billion—making it the 14th largest company in the world—it should come as no surprise TSMC makes up a substantial portion of many exchange traded funds (ETFs). It sits atop the iShares MSCI Emerging Markets ETF (EEM/NYSE) making up 5.85% of the fund.

TSMC also makes up 21.3% of the iShares MSCI Taiwan ETF (EWT/NYSE) and 3.69% of the iShares Semiconductor ETF (SOXX/NASDAQ). Consequently, even if TSMC isn’t exactly a household name in your house, if you’re an ETF investor, you might own more of it than you’re aware of.

On Thursday morning, TSMC announced an earnings beat and reported third-quarter net income of $8.81 billion on $20.23 billion in revenues. However, negative news in regards to U.S.-China relations and reduced Apple sales led the company to announce a 10% cut to capital spending.

Negative growth forecasts had been leaking out of TSMC all week, and shares have lost more than 37% year-to-date. With Russia’s recent invasion of Ukraine, fears of territorial invasion from superpower geopolitical neighbours are clearly factoring into current market sentiment.

While it’s concerning anytime a company boosts year-over-year profit by 80% and still sees its share price trend downward, the silver lining may be that the computer chip supply chain issues should finally start to ease if the TSMC forecasts are correct.

I’m sure given the last few years of world news everyone expects their portfolios to triple in value over the next decade right? Well…

Chartered financial analyst Ben Carlson recently presented some interesting data over at AWealthOfCommonSense.com.

The gist of Carlson’s data is that when coming out of deep bear markets, like the one we’re currently in (the S&P 500 is currently down more than 25% year-to-date), the black skies generally turn blue pretty quickly.

I don’t know about you, but I’d definitely settle for something in the neighbourhood of an 83.3% return over the next five years. And if we realize a total return of over 200% in the next 10 years, the 2022 recession-that-wasn’t-a-recession-but-could-be-a-recession will look like a blip in the rearview mirror.

When you realize that investors would have, on average, tripled their money if they just held tight during the nine bear markets of the past 70 years, it puts things in perspective. Compare how bad the circumstances of these bear markets were, suddenly the 7% inflation rate and 4% to 5% interest rates don’t look like a “massive crisis.”

As you’ve heard me and other Canadian investing experts say before, our ability to master our behavioural impulses will likely determine how much of these future gains we’ll get to enjoy versus how much we’ll lose out on “waiting for the real recovery” to begin.

Looking at the respective valuations of equities in Canada and the U.S. right now, Canadian investors could plausibly believe the S&P/TSX Composite (Canada’s equities index) will increase in value faster than the S&P 500 over the next decade.

Turns out that Bank of America’s strategists, Ohsung Kwon and Savita Subramanian, agree with that thesis. In fact, they’ve been thinking along these lines for a while now.

Here are some of the reasons for Canada’s predicted outperformance:

Mr. Kwon went on to say that the last time TSX stocks had an average P/E that was so much lower than the S&P 500’s P/E, it was all the way back in the early 2000s tech bubble. The Bank of America forecasts that TSX index investors can expect 6.5% growth, plus 3.4% in dividends over the next 10 years, while the S&P 500 would see combined returns of only 8% over the next 10 years.

We’d venture to add that we shouldn’t forget about the massive tailwinds that a supercharged U.S. dollar could provide for Canadian companies looking to sell goods to U.S. customers.

All that said, we’ve written about the historical outperformance of the U.S. stock market versus the Canadian stock market over at MillionDollarJourney.com, so I think I’ll stick with my broadly diversified portfolio.

Kyle Prevost is a financial educator, author and speaker. When he’s not on a basketball court or in a boxing ring trying to recapture his youth, you can find him helping Canadians with their finances over at MillionDollarJourney.com and the Canadian Financial Summit.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

From severing ties and becoming a non-resident to learning about departure and withholding taxes, here’s what expats can expect...

Here’s how Canada’s Old Age Security pension works, who’s eligible for OAS, when you can start receiving OAS, and...

Here’s how Canada’s retirement pension plan works, who’s eligible for CPP, when you can start receiving CPP, and CPP...

In this excerpt from her new book, Making Bank, Shannon Lee Simmons guides young Canadians (and their parents) through...

The retailer is confident new initiatives are drawing in customers, so what’s hampering the company’s growth prospects in the...

Sponsored By

Simplii Financial

Sponsored By

Simplii Financial

There’s more than one way to optimize your income after retiring. Some strategies can boost wealth, and others may...