Making sense of the markets this week: August 18, 2024

Falling U.S. inflation leads to rate cut certainty, Walmart’s strong quarter, Barrick beats Franco-Nevada for the gold metal, and the Sahm Rule rules.

Advertisement

Falling U.S. inflation leads to rate cut certainty, Walmart’s strong quarter, Barrick beats Franco-Nevada for the gold metal, and the Sahm Rule rules.

Kyle Prevost, creator of 4 Steps to a Worry-Free Retirement, Canada’s DIY retirement planning course, shares financial headlines and offers context for Canadian investors.

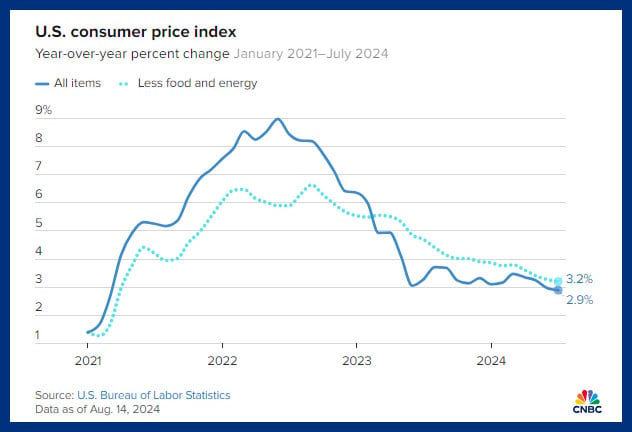

After much speculation about when the U.S. will finally begin cutting its interest rates, the CME FedWatch tool reports a 100% chance that the U.S. Federal Reserve will cut its rates in September. Market watchers are pretty confident, with a 36% chance that the U.S. Fed will go right to a 0.50% cut instead of nudging the rate down. And looking ahead, the futures market predicts a 100% chance of 0.75% in rate cuts by December this year, with a 32% chance of a 1.25% rate decrease. The forecasts became stronger this week as the annualized inflation rate in the U.S. slowed to 2.9%, its lowest rate since March 2021. There are a lot of percentages here, but the gist is people are expecting big interest rate cuts.

Those probabilities should take some of the currency pressure off of the Bank of Canada (BoC) when it makes its next interest rate decision on September 4. If the BoC were to continue to cut rates at a faster pace than the U.S. Fed, the Canadian dollar would substantially depreciate and import-led inflation would likely become an issue.

Here are some top-line takeaways from the U.S. Labor Department July CPI report:

When combined with the meagre July jobs report, it’s pretty clear the U.S. consumer-led inflation pressures are receding. As the U.S. cuts interest rates and mortgage costs come down, it’s quite likely that shelter costs (the last leg of strong inflation) could come down as well.

Get up to 4.00% interest on your savings without any fees.

Lock in your deposit and earn a guaranteed interest rate of 3.55%.

Earn 3.9% interest for the first five months. No minimum balance required and no fees.

MoneySense is an award-winning magazine, helping Canadians navigate money matters since 1999. Our editorial team of trained journalists works closely with leading personal finance experts in Canada. To help you find the best financial products, we compare the offerings from over 12 major institutions, including banks, credit unions and card issuers. Learn more about our advertising and trusted partners.

Despite slowing U.S. consumer spending, mega retailers Home Depot and Walmart continue to book solid profits.

Here are the results from this week. All numbers below are reported in USD.

While Home Depot posted a strong earnings beat on Wednesday, forward guidance was lukewarm, resulting in a gain of 1.60% on the day. Walmart, on the other hand, knocked the ball out of the park and raised its forward guidance and booked a gain of 6.58% on Thursday.

Walmart Chief Financial Officer John David Rainey told CNBC, “In this environment, it’s responsible or prudent to be a little bit guarded with the outlook, but we’re not projecting a recession.” He went on to add, “We see, among our members and customers, that they remain choiceful, discerning, value-seeking, focusing on things like essentials rather than discretionary items, but importantly, we don’t see any additional fraying of consumer health.”

Same-store sales for Walmart U.S. were up 4.2% year over year, and e-commerce sales were up 22%. The mega retailer highlighted its launch of the Bettergoods grocery brand as a way to monetize the trend toward cheaper food-at-home options, and away from fast food.

The mood was not quite as upbeat over at Home Depot. Chief Financial Officer Richard McPhail told CNBC that Home Depot customers were delaying major purchases with a “deferral mindset.” Comparable earnings were down slightly from the second quarter of 2023; that marks the seventh consecutive quarter of negative comparable sales since the pandemic-inspired home renovation binge of 2021 and 2022. Management stated that it believed headlines about future lowered interest rates were incentivizing customers to delay borrowing the money needed for their next big home projects.

Franco-Nevada Corp. (FNC) is often seen as a less risky way to invest in gold relative to Barrick Gold. That’s due to FNC’s low-debt royalties-based structure. FNC doesn’t own and operate its own mines like Barrick, and its upside is also capped. With gold prices so high, Barrick had a better quarter than FNC.

Both companies report their revenues, expenses, and earnings in U.S. dollars.

Shares of Barrick were up more than 8% on Monday after the company announced its earnings, while FNC was down 6.26%.

Barrick reported that the average realized price of gold was up 19% over the same period, while total gold production had fallen 6% year over year. Its cost of sales increased to $1,441 per ounce. It doesn’t take a genius to figure out that you’re going to make some pretty serious money if you can sell gold for $2,344 and it costs $1,441 to take it out of the ground. Barrick’s key focus for the next quarter is to expand its large gold-mining operations in Nevada.

Meanwhile, FNC saw overall revenues dip 21.2% year-over-year. Operating cash flow dropped from $472 million, in the first half of 2023, to $373 million, over the first half of 2024. Production struggles at the Antapaccay and Candelaria mines in South America were the main reasons for the performance regression. FNC reports that it is looking into diversifying its gold-heavy royalty portfolio to include lithium extraction.

Barrick and FNV share prices are both heavily dependent on gold prices. For more information on gold exposure within a portfolio, check out my article on how to invest in gold as a Canadian on MillionDollarJourney.ca.

Telling investors we’re in a recession six months after the recession actually happened is:

Since a recession is technically two consecutive quarters of shrinking gross domestic product (GDP), we only have to look at government-produced data at the end of every two quarters to say definitively whether we just experienced a recession. By that point, however, the market has largely noticed that businesses are having a harder time growing profits, and the damage to share prices has already happened.

What would be far more beneficial to investors? A way to determine whether we are in the midst of a recession. Or—even better—to accurately predict when a recession would begin.

This quest for recession indicators led to the creation of the Sahm Rule in 2019. Spoiler alert: The Sahm Rule warning light appears to be flashing bright red right now!

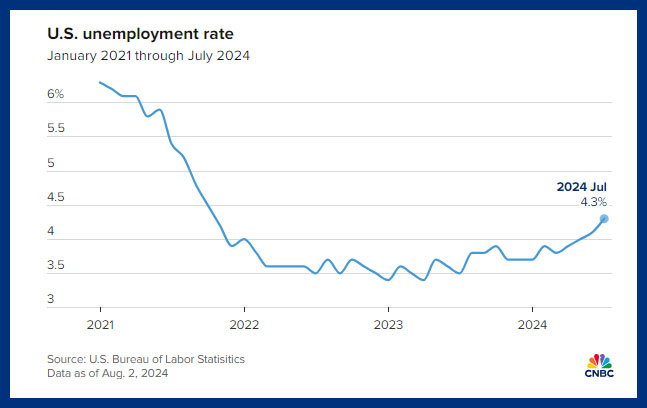

The Sahm Rule secret sauce is the three-month moving average for U.S. unemployment. A recession is happening if the three-month moving average unemployment rate increases more than 0.5% above the highest three-month average over the previous 12 months. The Sahm Rule makes intuitive sense—it essentially measures the data that a lot of people are losing their jobs.

Claudia Sahm created the rule. She’s a macroeconomist who worked at the U.S. Federal Reserve for 12 years (from 2007 to 2019) and was on the White House Council of Economic Advisers during the Obama administration. She’s been booked for many media appearances over the past couple of weeks, as the July jobs report confirmed the Sahm Rule was triggered. American unemployment has been going up. The speed the rate is rising has increased over the last few months. (However, it should be noted that while the unemployment rate is increasing, it is still near the lows of the past three years.)

Perhaps the most interesting point about the Sahm Rule-breaking is that Sahm herself isn’t even sure it’s an accurate indicator at the moment. Sahm has said, despite what her rule indicates, “We are not in a recession now—contrary to the historical signal from the Sahm rule—but the momentum is in that direction.”

Sahm went on to explain, “Our understanding of what is happening right now is so very challenged and what that means is—and I’ll be the first to say it as someone who has a rule attached to her name—don’t just rely on one tool.”

So, if we want to apply the Sahm rule (which has proven to be quite an effective prediction tool in the past) then the U.S. economy is in for a very rough ride. And in six months, the U.S. Fed will say that we had a recession. In this case, though, it might be better to listen to the creator of the rule. We should understand there is no guarantee we will see two consecutive quarters of negative GDP growth, while the momentum is headed in a negative direction.

Bank of Nova Scotia (BNS/TSX) made news this week with an announcement that it will be investing USD$2.8 billion to buy 14.9% of KeyCorp, a regional U.S. bank based in Cleveland. The deal appears to signal a move away from investment in Latin America and toward a more developed market closer to home. Is it a great use of Scotiabank’s limited capital? We’re not sure. Shareholders would likely see dividend increases or stock buybacks as less risky ways to use surplus cash. Read the full story: Scotiabank increases U.S. foothold with stake in KeyCorp

The other big merger headline came on Wednesday, when privately owned U.S. snacking and petcare giant Mars, Inc. announced its plans to acquire snacking and cereal maker Kellanova (K/NYSE).

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Presented By

Equifax

With all the personal finance advice on social media, it can be challenging to filter good from bad. Here’s...

Presented By

Equifax

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Students have a wide selection of banking options, from student offers at major banks to no-fee accounts with online...