What to expect for GICs in 2024

The rates offered on guaranteed investment certificates have skyrocketed over the past two years. Here are considerations for investors going into 2024.

Advertisement

The rates offered on guaranteed investment certificates have skyrocketed over the past two years. Here are considerations for investors going into 2024.

In late 2020, major banks were offering 5-year guaranteed investment certificates (GICs) with rates of less than 1%. Now, just three years later, bank GIC rates for 5-year terms are over 4%. Some credit unions and trust companies are offering rates over 6% for short-term GICs, though 4- and 5-year rates are just under 6%.

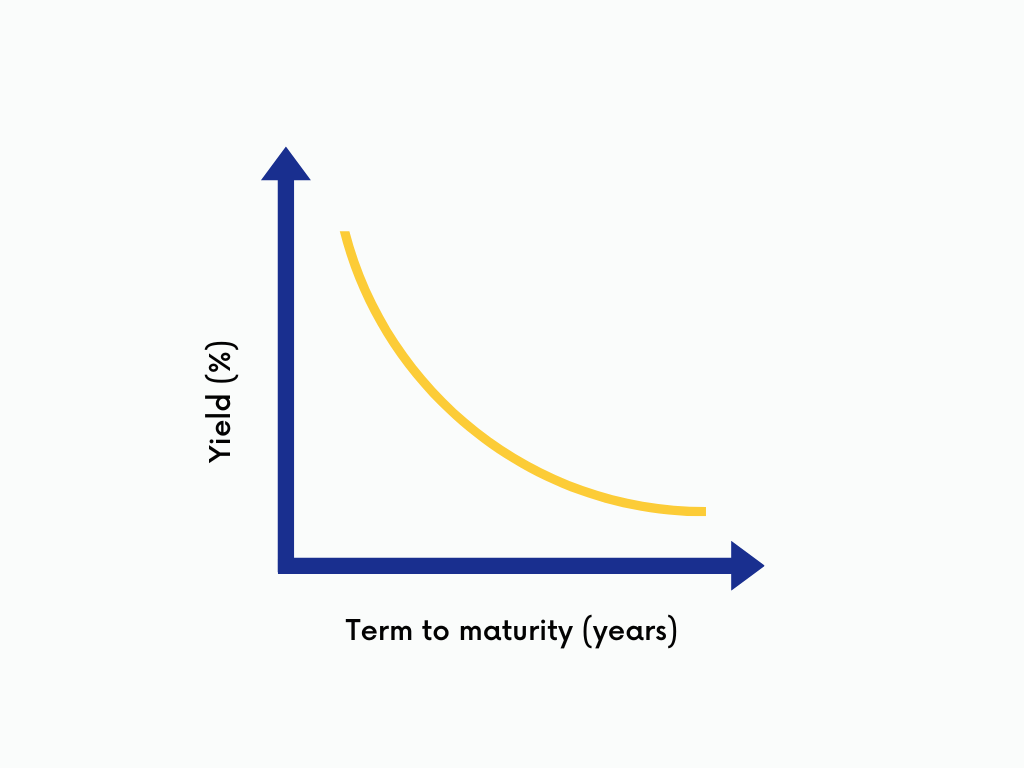

It is uncommon to see long-term rates lower than short-term rates. This is a situation called an inverted yield curve. It signals expectations that interest rates will fall in the future. It can also forecast a recession, which tends to result in lower interest rates to stimulate a weakening economy.

Most interest rate forecasts see rates declining in Canada in 2024. RBC Economics predicts the Bank of Canada’s overnight rate will drop by 1% by the fourth quarter of 2024. Scotiabank agrees with RBC, and TD is forecasting a 0.75% decline by the end of 2024.

Forecasts are not always accurate, but the consensus seems to be that rates could be lower next year. So, what does this mean for investors who are considering GICs?

MoneySense is an award-winning magazine, helping Canadians navigate money matters since 1999. Our editorial team of trained journalists works closely with leading personal finance experts in Canada. To help you find the best financial products, we compare the offerings from over 12 major institutions, including banks, credit unions and card issuers. Learn more about our advertising and trusted partners.

Bonds got slaughtered in 2022, with the FTSE Canada Universe Bond Index returning a loss of nearly 12% to investors for the calendar year. The reason? Interest rates shot up, and rates and bond prices move in opposite directions.

If interest rates fall in 2024, bonds could perform well, rising as rates decline.

The weighted average yield to maturity for the FTSE Canada Universe Bond Index is about 4.6% currently. The duration for the index is about 7.1 years. Duration measures how responsive a bond or a bond index is to interest rate changes. It is similar to a bond’s term to maturity but is adjusted based on the forecasted cash flows from interest payments.

If interest rates fall by 1%, a bond or bond index with a 7.1-year duration should rise by about 7.1%. As a result, if rates do fall in 2024, bonds could potentially provide double-digit returns between their price appreciation and their yield.

Longer term bonds could perform even better. The longer the duration, the more the potential upside if rates fall. But on the flipside, the more the potential losses if rates rise further.

The point? If a GIC investor is looking to lock in a good long-term interest rate, they may want to consider some bond exposure as well to diversify. If rates do in fact fall, bonds could do very well.

Regardless, for a conservative investor, earning a return in the 6% range from a GIC is pretty enticing.

If you’re buying a GIC or bond in a tax-sheltered account, the tax implications do not matter. Interest income in a registered retirement savings plan (RRSP) or tax-free savings account (TFSA) is tax-free, although RRSP withdrawals are eventually taxable.

If you are considering a GIC in a taxable account like a personal non-registered account or a corporate investment account, tax is a factor.

If an Ontario investor with $100,000 of income earns a dollar of interest income, they pay a marginal tax rate on that dollar of about 31%. So, buying a 6% GIC leaves only about 4.1% after tax.

If that same investor bought Canadian stocks and earned a 6% return with 2% from dividends and 4% from capital gains, selling after a year, the tax would be less. The tax rate on the dividend income would be about 9% and on the capital gain would be about 16%. The after-tax return would be about 5.2%, over 1% higher than the GIC investor earning the same 6%.

Depending on the dollar value of the GIC or stock, the income could push the investor into a higher tax bracket than the marginal rates referenced above, but the outcome would be similar, with stocks being more tax efficient. The tax savings for stocks over GICs would also apply in other provinces.

As a result, a stock investor could earn a lower rate of return than a GIC investor in a taxable account and still keep more of their after-tax return. Stocks generally return more than GICs or bonds over the long run, despite the year to year volatility. This is an important consideration for a GIC investor when tax is considered. After all, it is your after-tax return that really matters.

In summary, GIC rates are very high right now—higher than they have been in almost 30 years. They seem poised to decline in 2024, but interest rates are very difficult to predict. A lot of investors got blindsided by rate increases in 2022, causing steep losses for bonds. Bonds could bounce back nicely in the year ahead if rates do fall.

Investors with taxable investment accounts should consider the tax implications of their investment income. A 6% GIC return in a tax-sheltered account is pretty good but in a taxable account, high-income investors may lose over half of their return to income tax. Stocks are more tax efficient and for an investor with a medium or long time horizon and moderate to high risk tolerance, stocks should be considered for their potential to provide higher pre- and post-tax returns.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

It’s almost impossible to do, but the mindset around spending all your savings can help you make the best of the...

In the likelihood of a protracted conflict, these experts think people in or close to retirement need to review...

Filing your 2025 taxes in 2026? Here are the key changes, cancelled credits, and CRA updates Canadians need...

Look under the hood before buying some popular Canadian sector ETFs. There may be alternatives that better represent the...

Global conflicts affect Canadians’ finances in real time. Learn how rising costs, volatility, and uncertainty can impact your budget...

If you leave Canada and own a rental property, or you are a non-resident and you buy a rental...

Gen Z faces an “experience gap” as AI and employer expectations rise. Co-ops, apprenticeships, and hands-on learning are now...

Rental property investors need to report their annual income and expenses on their tax return. You must also track...

The Canada Caregiver Amount can help families supporting loved ones with infirmities. Learn who qualifies and how much you...

Bitcoin extends losses, down 47% since October 2025. When will the crypto bear market reverse, and what does the...

“The reason? Interest rates shot up and rates and bond yields move in opposite directions.”

Isn’t that rates and bond prices move in opposite directions?

Hi Christopher, Thank you for bringing this to our attention. We have updated the article.

Nice article!

Good article – but seniors also need to keep in mind the “dividend gross-up” of 38% on stocks, (and equity mutual funds and ETFs) which will be used to calculate taxable income. This nasty attack on seniors is used to claw back, or even wipe, out Old Age Security payments!