RRSP vs TFSA: Which should you top up in retirement?

The TFSA wins because it's flexible

Advertisement

The TFSA wins because it's flexible

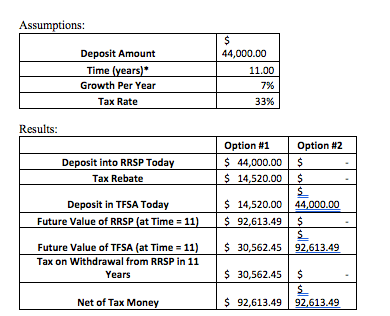

Q: I’m a 60-year-old retired school teacher as of this past July 2017. I have $44,000 in unused RRSP contribution room. Should I max out my contribution room on my 2017 taxes? Or just stick to topping up my TFSA?

—Chris

A: Hi Chris. Thanks for the question. Please note that RRSP only counts as a deduction against “earned income” which includes:

Q: I’m a 60-year-old retired school teacher as of this past July 2017. I have $44,000 in unused RRSP contribution room. Should I max out my contribution room on my 2017 taxes? Or just stick to topping up my TFSA?

—Chris

A: Hi Chris. Thanks for the question. Please note that RRSP only counts as a deduction against “earned income” which includes:

Conclusion: Both result in the same end value since you are facing a constant tax rate. Further, your RRSP must be converted upon your 71st birthday whereas you can leave your TFSA to grow for as long or short as you desire. Additionally, it is usually recommended to draw out of your RRSP rather than your TFSA earlier in retirement as your TFSA will incur no tax upon your passing or any withdrawals as compared to your RRSP which will be taxed fully.

What we can conclude is this. If your income will be staying constant throughout your retirement I would advise you to top up your TFSA rather than your RRSP for the following reasons

Conclusion: Both result in the same end value since you are facing a constant tax rate. Further, your RRSP must be converted upon your 71st birthday whereas you can leave your TFSA to grow for as long or short as you desire. Additionally, it is usually recommended to draw out of your RRSP rather than your TFSA earlier in retirement as your TFSA will incur no tax upon your passing or any withdrawals as compared to your RRSP which will be taxed fully.

What we can conclude is this. If your income will be staying constant throughout your retirement I would advise you to top up your TFSA rather than your RRSP for the following reasons

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

There are several personal, trust and corporate income-tax-filing extensions for Canadians this year. Which ones apply to you? ...

What to consider when deciding to incorporate a company with friends to buy real estate and more.

There’s more than one way to optimize your income after retiring. Some strategies can boost wealth, and others may...

Can you retroactively change the valuation of a rental property before selling it to reduce capital gains tax in...

Presented By

Equifax

RRSP contributions can reduce capital gains tax. How does that work, and when might a different tax strategy be...

Want to give or loan money to your children? Here are the factors that determine who pays tax in...

Power of attorney compensation can be high, but the role can be a lot of work. Here’s what happens...

Canadians must begin taking RRIF withdrawals the year after converting an RRSP. What happens if you convert only part...

A Certified Financial Planner looks at the different strategies to ask your own advisor: Is life insurance the answer?