Train your investing brain

Don't let the market slide get the best of you

Advertisement

Don't let the market slide get the best of you

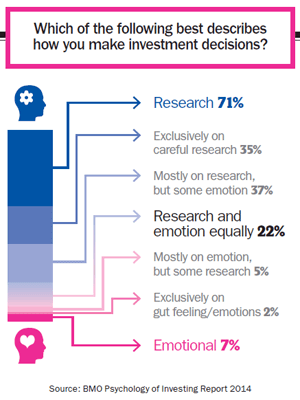

What’s the biggest threat to your portfolio? Most people would say low interest rates, high investment fees, looming inflation or the threat of a global crisis like the one that nearly brought down the financial system in 2008. But in the words of the legendary Benjamin Graham, “The investor’s chief problem—and even his worst enemy—is likely to be himself.”

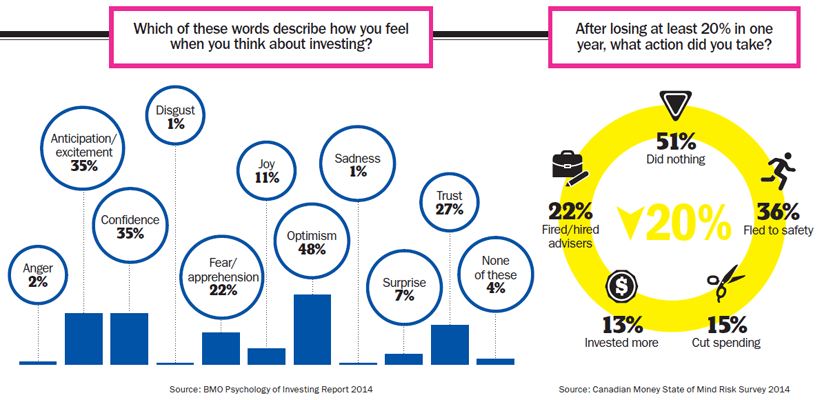

Don’t take that personally. Humans simply aren’t programmed to be rational, disciplined investors. We all have what psychologists call “cognitive biases,” or mental blind spots that interfere with good decisions. We also have to fight against emotions that make it difficult to stick to a long-term strategy.

Mastering your behaviour can have a dramatic impact on your investing performance—but it won’t be easy. “Not many people are emotionally detached from their money,” says Edwin Weinstein, a psychologist and president of The Brondesbury Group, a Toronto-based research firm specializing in financial services. “We’re certainly capable of learning to do better, though sometimes it’s only after being burned.” Weinstein says investors should recognize which biases they’re most prone to and use a strategy that suits their temperament. “The first principle is know yourself and work with that.” So let’s look at the most common behavioural biases and consider ways you can overcome them.

What’s the biggest threat to your portfolio? Most people would say low interest rates, high investment fees, looming inflation or the threat of a global crisis like the one that nearly brought down the financial system in 2008. But in the words of the legendary Benjamin Graham, “The investor’s chief problem—and even his worst enemy—is likely to be himself.”

Don’t take that personally. Humans simply aren’t programmed to be rational, disciplined investors. We all have what psychologists call “cognitive biases,” or mental blind spots that interfere with good decisions. We also have to fight against emotions that make it difficult to stick to a long-term strategy.

Mastering your behaviour can have a dramatic impact on your investing performance—but it won’t be easy. “Not many people are emotionally detached from their money,” says Edwin Weinstein, a psychologist and president of The Brondesbury Group, a Toronto-based research firm specializing in financial services. “We’re certainly capable of learning to do better, though sometimes it’s only after being burned.” Weinstein says investors should recognize which biases they’re most prone to and use a strategy that suits their temperament. “The first principle is know yourself and work with that.” So let’s look at the most common behavioural biases and consider ways you can overcome them.

We all love choices. But whether it’s desserts or mutual funds, a huge number of options often leads to worse decisions and lower satisfaction. In one study commissioned by the investment firm Vanguard, researchers found 75% of employees enrolled in their workplace retirement plans when they had just four funds to choose from, but only 60% did so when they had 59 options. Many employees who were overwhelmed by choice did nothing. A host of others simply picked the most conservative choices (bond or money market funds) rather than making any attempt to learn about the funds with more potential for growth.

The psychological culprit here is called regret aversion: people tend to put off making decisions because they fear their choice will lead to a poor outcome. It often leads investors to sit on large amounts of cash, especially after they have sold at a loss. At other times it reveals itself as plain old procrastination. “Among people who are managing their own portfolios, or who are controlling the decisions of their advisers, there is a tendency to procrastinate everything from making monthly contributions to rebalancing properly,” says Keith Matthews, portfolio manager at Tulett, Matthews & Associates in Montreal and author of The Empowered Investor.

You can overcome analysis paralysis by automating many decisions: setting up preauthorized monthly contributions is an ideal way to avoid the stress of investing lump sums. For very large amounts (such as the proceeds from selling a business) Matthews sometimes eases into the market to reduce the risk of bad timing, but he’ll do so over just nine to 12 months. “Think about making a few big steps,” he says, “because if you’re doing a lot of little steps, somewhere along the way something is going to spook you and you’re going to stop.”

We all love choices. But whether it’s desserts or mutual funds, a huge number of options often leads to worse decisions and lower satisfaction. In one study commissioned by the investment firm Vanguard, researchers found 75% of employees enrolled in their workplace retirement plans when they had just four funds to choose from, but only 60% did so when they had 59 options. Many employees who were overwhelmed by choice did nothing. A host of others simply picked the most conservative choices (bond or money market funds) rather than making any attempt to learn about the funds with more potential for growth.

The psychological culprit here is called regret aversion: people tend to put off making decisions because they fear their choice will lead to a poor outcome. It often leads investors to sit on large amounts of cash, especially after they have sold at a loss. At other times it reveals itself as plain old procrastination. “Among people who are managing their own portfolios, or who are controlling the decisions of their advisers, there is a tendency to procrastinate everything from making monthly contributions to rebalancing properly,” says Keith Matthews, portfolio manager at Tulett, Matthews & Associates in Montreal and author of The Empowered Investor.

You can overcome analysis paralysis by automating many decisions: setting up preauthorized monthly contributions is an ideal way to avoid the stress of investing lump sums. For very large amounts (such as the proceeds from selling a business) Matthews sometimes eases into the market to reduce the risk of bad timing, but he’ll do so over just nine to 12 months. “Think about making a few big steps,” he says, “because if you’re doing a lot of little steps, somewhere along the way something is going to spook you and you’re going to stop.”

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email