Last year’s edition of the MoneySense ETF All-Stars was our first attempt to spotlight Canada’s best exchange-traded funds. It was easy to assemble a great portfolio from those building blocks, but there were still a few holes in the Canadian ETF marketplace, especially when it came to U.S. and international equities. We’re happy to report that several new product launches in 2013 have plugged these gaps, and we’ve included a handful of new funds in this year’s All-Star lineup.

For this second annual edition, we again consulted five investment professionals for their thoughts on the best funds in the major asset classes. By selecting between three and six ETFs from our list, anyone can build a well-diversified, low-cost portfolio.

Before we get to the picks, a few words about methodology. When investors research actively managed mutual funds, they often dwell on absolute performance. However, that makes little sense when looking at traditional ETFs, which try simply to capture the returns of a specific asset class. So we looked for the funds that did the best job of harnessing those market returns. Our picks tend toward ETFs tracking traditional indexes rather than those using more elaborate strategies. “We’re looking to get exposure to the broad elements of the economy,” says Mark Yamada of PUR Investing in Toronto, “and that’s what ETFs allow us to do very cost-effectively.”

Low cost is always paramount. To keep comparisons fair, our table (see p. 50) lists only a fund’s management fee rather than its full management expense ratio (MER). The MER is higher and more useful, since it also includes taxes and incidental costs. But some ETFs on our list have been around less than a year, so their full MERs are not yet known.

In this year’s All-Star lineup, we’ve included only ETFs listed on the Toronto Stock Exchange. Canadian investors can also use ETFs listed on U.S. exchanges—indeed, many of these have even lower fees and are more tax-efficient. But you’ll need to buy and sell them in U.S. dollars, and converting currency can be expensive. “The average retail investor is better off using Canadian-listed ETFs so they’re not getting burned by currency spreads,” says Alan Fustey, portfolio manager at Index Wealth Management in Winnipeg. “It doesn’t make sense to worry about 0.10% of MER, then go out and pay 2% to convert the currency.”

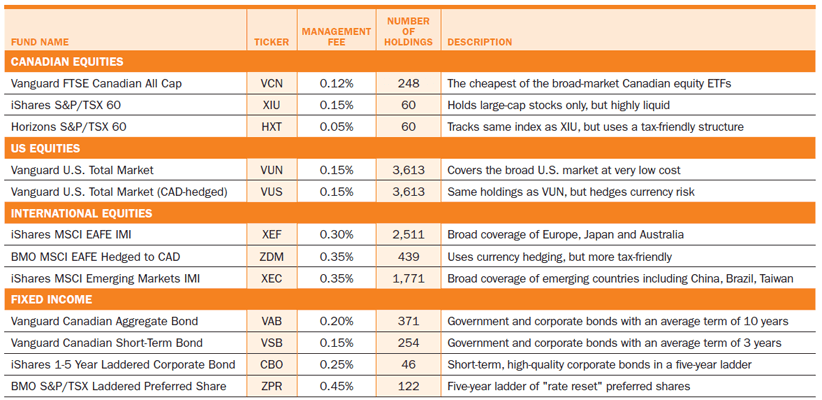

Canadian equities

Most Canadians—like investors around the world—keep the bulk of their stock holdings in their home country. For many years the go-to index for the broad Canadian market has been the S&P/TSX Composite, which includes about 250 stocks. However, last year Vanguard Canada launched a new ETF tracking an almost identical benchmark: the Vanguard FTSE Canada All Cap (VCN). With a management fee of just 0.12%, it’s now the cost leader.

Some investors and advisers avoid new ETFs, concerned they may eventually close if they don’t gather enough assets. Justin Bender, portfolio manager at PWL Capital in Toronto, doesn’t feel that’s a concern with VCN and has already begun to use it with clients. “Vanguard is going to be here for a long time and I expect VCN to grow quickly, since it’s now the cheapest of the broad-market Canadian equity ETFs.”

Our other experts have a preference for iShares S&P/TSX 60 (XIU), the country’s oldest and largest ETF, with $12.5 billion under management. While its fee is slightly higher, the added liquidity is an advantage. “VCN has only $30 million in assets and seems to trade with a bid-ask spread of two or three cents, compared to one cent for XIU,” says Fustey. “So there is a cost that goes beyond just the MER.”

While VCN holds about four times as many stocks as XIU, that difference isn’t as big as it sounds. “I don’t feel it’s terribly important if ETFs hold few or many stocks,” says Fred Kirby, a fee-for-service financial planner in Armstrong, B.C. “What matters is if they have consistently high correlations with similar returns.” XIU’s performance is likely to be very similar to VCN’s, since the 60 largest companies make up more than 70% of the broad market.

The Horizons S&P/TSX 60 (HXT) appeals to investors using taxable accounts, as long as they don’t need to generate income from dividends. HXT tracks the same index as XIU but uses an instrument called a “total return swap” to make it more tax-efficient. This structure carries extra risk but has helped the ETF track its index almost perfectly. It also lets investors defer tax on dividends until they eventually sell units in the ETF, at which point they’re taxed as capital gains.

U.S. equities

Another of Vanguard’s new products is our choice for U.S. stocks: the Vanguard U.S. Total Market (VUN). The largest U.S. equity ETFs in Canada track the S&P 500, which covers large-cap stocks only. But VUN widens the net considerably with a portfolio of more than 3,600 companies. And it does so for an annual fee of just 0.15%. “You get a little more of a small-cap effect, which has tended to be positive over time,” says Ioulia Tretiakova of PUR Investing, “plus more diversification.”

Kirby notes the exposure to small-cap stocks allowed the U.S. version of this ETF to outperform the S&P 500 by almost a full percentage point annually since mid-2001.

VUN has a sister fund that uses currency hedging, which is designed to remove the effect of the exchange rate between the U.S. dollar and the loonie. Without currency hedging, a rise in the Canadian dollar will cause U.S. holdings to fall in value, so the Vanguard U.S. Total Market CAD-Hedged (VUS) uses currency futures to reduce that risk.

“If you don’t have a view about exchange rates and it’s a short time horizon of less than three years, then currency hedging makes sense,” says Yamada. “But it is expensive over time, so if you intend to hold the position for longer, we would not hedge.”

International equity

Now that domestic stocks have lagged the rest of the world for three years, Canadians finally seem to be warming to the idea of investing overseas. Given the lack of diversification in the Canadian market—which is dominated by banks, energy and mining companies—international equities should be part of any long-term portfolio.

In last year’s inaugural edition of the ETF All-Stars, we lamented the fact that most Canadian-listed international equity ETFs used currency hedging, and many were quite expensive. The good news is 2013 saw the launch of two new funds that give investors more options and lower costs.

Like most of our other experts, Justin Bender uses U.S.-listed ETFs for international equities in clients’ portfolios. But for DIY investors he recommends the new iShares MSCI EAFE IMI (XEF), which tracks a total-market index of more than 2,500 large, mid-sized and small companies in the developed markets of Europe, the Far East and Australia. He also likes its sister fund, the iShares MSCI Emerging Markets IMI ETF (XEC), which covers more than 1,700 companies in developing countries, including China, Taiwan, Brazil and South Korea. The ETFs have management fees of just 0.30% and 0.35%, respectively, and neither uses currency hedging.

For investors who do want to hedge the currency in their foreign investments, our pick is the BMO MSCI EAFE Hedged to CAD (ZDM). The international equity ETFs from Vanguard and iShares simply hold a U.S.-listed ETF rather than buying the underlying stocks directly, which results in a layer of foreign withholding taxes on dividends, Bender points out. ZDM, by contrast, holds its 400-plus stocks directly; his analysis shows it’s more tax-efficient, which may compensate for its higher MER.

Fixed income

Bonds had a difficult time in 2013: the DEX Universe Bond Index saw its first negative year of the new millennium. Concerns about rising interest rates continue to scare investors away from bonds—which fall in value when rates climb—but just about every portfolio needs some fixed income.

In a low-rate environment, keeping costs low is more important than ever. The cost leader among broad-market bond ETFs is the Vanguard Canadian Aggregate Bond Index ETF (VAB). It includes about 80% government and 20% corporate bonds, with an average maturity of about 10 years. For long-term investors who have no view on interest rates, this ETF makes an excellent core holding—but understand it will lose value if and when interest rates rise.

Our panel of experts tends to favour short-term bonds, which are less volatile and will outperform during periods of rising interest rates. The Vanguard Canadian Short-Term Bond (VSB) can be substituted for VAB: it holds about 30% corporate bonds and has an average maturity of just three years.

Corporate bonds offer additional yield, and the iShares 1-5 Year Laddered Corporate Bond (CBO) uses a time-honoured strategy to smooth out interest rate risk: it holds one fifth of its portfolio in five different “rungs,” with maturities of one to five years. “You don’t have to guess what interest rates are going to do: you just roll with rate movements,” says Yamada.

Many advisers, including Fustey, use preferred shares as part of their fixed-income portfolios. Buying preferreds is a challenge for DIY investors, because they can have many complicated features and tend to be illiquid. BMO S&P/TSXLaddered Preferred Share (ZPR) offers an easy way to get access: it uses the same one-to-five-year laddered structure as CBO, but holds “rate reset” preferreds instead of corporate bonds. These preferreds have a maturity date, at which point the company will reissue them at current rates or redeem them at par. “Rate resets are the place you want to be over the next five years because interest rates are probably going higher, not lower,” says Fustey. “So I think the strategy in ZPR is hugely timely.”

Our ETF Portfolio Picks for 2014

By charging low fees to harness market returns, these ETFs are the ideal building blocks in a diversified portfolio.

One final word of advice. Our ETF All-Stars are designed to highlight the best products available, but the differences between ETFs are often quite small. Long-term investors should avoid the temptation to jump from one ETF to another every time there’s a new launch. “Just because a new ETF has a slightly lower MER or holds more stocks, I don’t think investors should be switching in and out of ETFs on an annual basis,” says Kirby.

Bender agrees and says investors need to consider whether transaction costs and taxes will outweigh the benefit of switching to a marginally cheaper fund. “After the last few years, many older ETFs have large unrealized capital gains,” he says. “Selling them and taking that tax hit just doesn’t make sense.”

Frequent switching also undermines the discipline and patience you need to be a successful investor. So hold off on any new purchases until the next time you make a large contribution, do some tax-loss selling or rebalance your portfolio.

Our ETF Experts

Alan Fustey is a portfolio manager at Index Wealth Management in Winnipeg and author of Risk, Financial Markets & You. He has been using ETFs with clients for more than a decade.

Justin Bender is a portfolio manager at PWL Capital in Toronto, where he uses ETFs with his full-service clients and helps do-it-yourself investors set up their own ETF portfolios.

Fred Kirby is a fee-for-service financial planner who writes an investment and retirement planning newsletter from the outskirts of Armstrong, B.C.

Mark Yamada is CEO of Toronto’s PUR Investing, and Ioulia Tretiakova is the firm’s director of quantitative strategies. They build ETF portfolios for both individual and institutional clients.

Dan Bortolotti writes the Canadian Couch Potato blog and is author of the MoneySense Guide to the Perfect Portfolio. He has partnered with PWL Capital to help DIY investors manage their own ETF portfolios.

One final word of advice. Our ETF All-Stars are designed to highlight the best products available, but the differences between ETFs are often quite small. Long-term investors should avoid the temptation to jump from one ETF to another every time there’s a new launch. “Just because a new ETF has a slightly lower MER or holds more stocks, I don’t think investors should be switching in and out of ETFs on an annual basis,” says Kirby.

Bender agrees and says investors need to consider whether transaction costs and taxes will outweigh the benefit of switching to a marginally cheaper fund. “After the last few years, many older ETFs have large unrealized capital gains,” he says. “Selling them and taking that tax hit just doesn’t make sense.”

Frequent switching also undermines the discipline and patience you need to be a successful investor. So hold off on any new purchases until the next time you make a large contribution, do some tax-loss selling or rebalance your portfolio.

Our ETF Experts

Alan Fustey is a portfolio manager at Index Wealth Management in Winnipeg and author of Risk, Financial Markets & You. He has been using ETFs with clients for more than a decade.

Justin Bender is a portfolio manager at PWL Capital in Toronto, where he uses ETFs with his full-service clients and helps do-it-yourself investors set up their own ETF portfolios.

Fred Kirby is a fee-for-service financial planner who writes an investment and retirement planning newsletter from the outskirts of Armstrong, B.C.

Mark Yamada is CEO of Toronto’s PUR Investing, and Ioulia Tretiakova is the firm’s director of quantitative strategies. They build ETF portfolios for both individual and institutional clients.

Dan Bortolotti writes the Canadian Couch Potato blog and is author of the MoneySense Guide to the Perfect Portfolio. He has partnered with PWL Capital to help DIY investors manage their own ETF portfolios.