A sudden change of plan

Joel Wilson had a prosperous career, until disaster struck. Can he train for a new career and look after his family at the same time?

Advertisement

Joel Wilson had a prosperous career, until disaster struck. Can he train for a new career and look after his family at the same time?

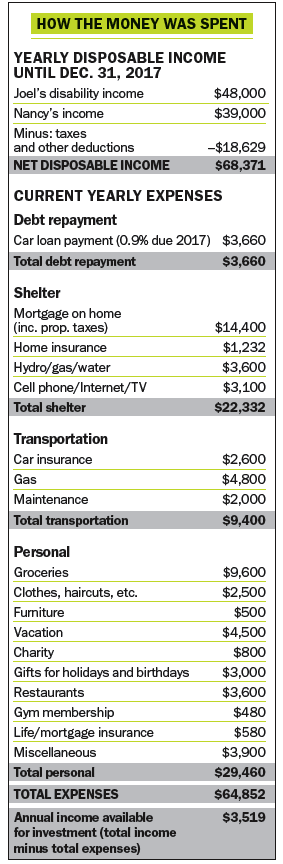

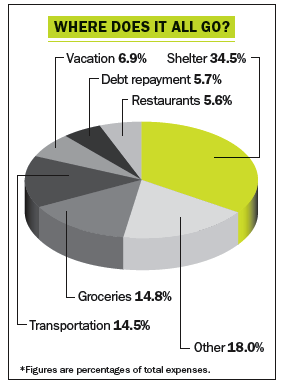

Before Joel went on disability, the couple had been earning a household income of about $125,000, most of that from Joel’s $85,000-a-year pay (which includes $16,000 in overtime). His current disability payments amount to 70% of his base salary of $69,000, and the paramedics union will continue to pay into his pension and benefits—but only until December 2017. “Then I’ll have to make a decision about whether I leave or continue as a paramedic,” says Joel.

One option may be to take a desk job in the paramedics office, which pays half of what field operatives make. “I’m trained to be a paramedic and not much else,” says Joel. “But I don’t want to languish in a low-paying job I don’t like just for the sake of having a job with benefits.” Still, he adds, “Nancy has no benefits, so the push is for me to stay.” Meanwhile, Nancy feels they can scrape by on a household income of $80,000 gross annually if they have to, but she’d prefer to maintain the $125,000 income they’re accustomed to. “It’s what we are comfortable living on,” she admits.

Despite all of the hand-wringing over what Joel should do with his current job, being a paramedic isn’t something he ever actually aspired to do. “I saw an ad for it in my final year of high school,” says Joel (he and Nancy attended the same high school before she went on to college). “I applied but never thought I’d get in. But then I got picked.”

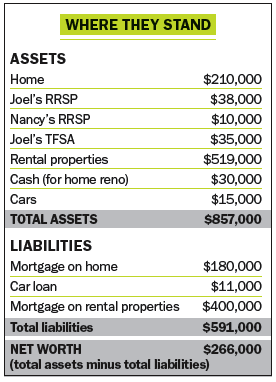

One of his real passions, he’s discovered over the years, is real estate investing. To that end, he and Nancy have spent the last seven years putting most of their disposable income towards the purchase of five small rental properties north of Chatham that are all worth a little over $100,000 each. “We think of them as our retirement plan,” says Nancy. “They’ll be paid off in 25 years. Then we’ll use the rents to supplement our retirement income.”

But that’s not been without its problems either. With the local real estate market flat, the properties have seen absolutely no capital appreciation. And with a hefty total of $400,000 in mortgages on those properties, the couple is starting to question whether they should hold on to them. “If Joel does the maintenance and repairs, the income carries the expenses,” says Nancy. “But we’re not sure he can keep doing that.”

On top of that, it was only last year that the couple spent $210,000 on a two-storey fixer-upper—situated on a leafy street near a great public school—to live in themselves. Before his illness and surgery, Joel had been doing some work on the home, in preparation for the children they had hoped to start trying for. While they still have the $30,000 set aside for renovations to the bathroom, kitchen and main floor, Joel’s now wondering if it’s time to put those plans on hold, too.

The fact is, that money would come in handy if he did decide to go back to school after his current salary and benefits expire in 2017. But because Nancy has waited a long time for them to start growing their family, he says he’d feel like he was letting her down if they delayed.

All the same, he feels strongly that their future rests in him finding another well-paying job—hopefully, one that is well-suited to him and that he can happily ride out until retirement. In particular, Joel has been giving a lot of thought to a job in business or finance, or possibly even running his own small business. Just recently, he started index investing with exchange-traded funds (ETFs*) and has $48,000 of assets in his RRSPs*, as well as $35,000 in his TFSAs*. “I’m really enjoying it,” he says.

Before Joel went on disability, the couple had been earning a household income of about $125,000, most of that from Joel’s $85,000-a-year pay (which includes $16,000 in overtime). His current disability payments amount to 70% of his base salary of $69,000, and the paramedics union will continue to pay into his pension and benefits—but only until December 2017. “Then I’ll have to make a decision about whether I leave or continue as a paramedic,” says Joel.

One option may be to take a desk job in the paramedics office, which pays half of what field operatives make. “I’m trained to be a paramedic and not much else,” says Joel. “But I don’t want to languish in a low-paying job I don’t like just for the sake of having a job with benefits.” Still, he adds, “Nancy has no benefits, so the push is for me to stay.” Meanwhile, Nancy feels they can scrape by on a household income of $80,000 gross annually if they have to, but she’d prefer to maintain the $125,000 income they’re accustomed to. “It’s what we are comfortable living on,” she admits.

Despite all of the hand-wringing over what Joel should do with his current job, being a paramedic isn’t something he ever actually aspired to do. “I saw an ad for it in my final year of high school,” says Joel (he and Nancy attended the same high school before she went on to college). “I applied but never thought I’d get in. But then I got picked.”

One of his real passions, he’s discovered over the years, is real estate investing. To that end, he and Nancy have spent the last seven years putting most of their disposable income towards the purchase of five small rental properties north of Chatham that are all worth a little over $100,000 each. “We think of them as our retirement plan,” says Nancy. “They’ll be paid off in 25 years. Then we’ll use the rents to supplement our retirement income.”

But that’s not been without its problems either. With the local real estate market flat, the properties have seen absolutely no capital appreciation. And with a hefty total of $400,000 in mortgages on those properties, the couple is starting to question whether they should hold on to them. “If Joel does the maintenance and repairs, the income carries the expenses,” says Nancy. “But we’re not sure he can keep doing that.”

On top of that, it was only last year that the couple spent $210,000 on a two-storey fixer-upper—situated on a leafy street near a great public school—to live in themselves. Before his illness and surgery, Joel had been doing some work on the home, in preparation for the children they had hoped to start trying for. While they still have the $30,000 set aside for renovations to the bathroom, kitchen and main floor, Joel’s now wondering if it’s time to put those plans on hold, too.

The fact is, that money would come in handy if he did decide to go back to school after his current salary and benefits expire in 2017. But because Nancy has waited a long time for them to start growing their family, he says he’d feel like he was letting her down if they delayed.

All the same, he feels strongly that their future rests in him finding another well-paying job—hopefully, one that is well-suited to him and that he can happily ride out until retirement. In particular, Joel has been giving a lot of thought to a job in business or finance, or possibly even running his own small business. Just recently, he started index investing with exchange-traded funds (ETFs*) and has $48,000 of assets in his RRSPs*, as well as $35,000 in his TFSAs*. “I’m really enjoying it,” he says.

Once Joel’s health benefits run out on Dec. 31, 2017, Joel shouldn’t take a job simply because it offers benefits. Instead, he should buy insurance coverage through an insurance broker. He’s certainly eligible. “Private insurance is available—especially at Joel’s young age,” says independent insurance broker Lorne Marr. For many people, private insurance is a good—often temporary—solution. Marr notes that health and dental insurance policies will usually exclude pre-existing conditions. Annual premiums for the Wilsons, according to Marr, would cost about $1,900 annually. Most disability plans, too, will not cover pre-existing conditions, but Joel can easily get a good disability policy. “The premiums will depend on the type of occupation Joel chooses,” says Marr. Assuming an office job, a policy offering $2,000 a month in benefits with payments ending at age 65 will cost Joel about $80 a month. For Nancy, the cost would be $110 a month.

For life insurance coverage, Joel can get a simplified issue policy where there are no medical tests. Instead, he’ll have to answer a short series of health questions. “The more questions Joel can answer ‘no’ to, the lower the premium,” explains Marr. A $500,000 simplified issue term 20 policy for Joel costs about $70 a month. Similar coverage for Nancy costs $23. Total cost for all benefits? $5,296 annually. “The couple would be entitled to tax credits and deductions for some of those costs at tax time,” says Marr. “Of course, if Joel gets a new job with full benefits, the private insurance costs will go.”

Once Joel’s health benefits run out on Dec. 31, 2017, Joel shouldn’t take a job simply because it offers benefits. Instead, he should buy insurance coverage through an insurance broker. He’s certainly eligible. “Private insurance is available—especially at Joel’s young age,” says independent insurance broker Lorne Marr. For many people, private insurance is a good—often temporary—solution. Marr notes that health and dental insurance policies will usually exclude pre-existing conditions. Annual premiums for the Wilsons, according to Marr, would cost about $1,900 annually. Most disability plans, too, will not cover pre-existing conditions, but Joel can easily get a good disability policy. “The premiums will depend on the type of occupation Joel chooses,” says Marr. Assuming an office job, a policy offering $2,000 a month in benefits with payments ending at age 65 will cost Joel about $80 a month. For Nancy, the cost would be $110 a month.

For life insurance coverage, Joel can get a simplified issue policy where there are no medical tests. Instead, he’ll have to answer a short series of health questions. “The more questions Joel can answer ‘no’ to, the lower the premium,” explains Marr. A $500,000 simplified issue term 20 policy for Joel costs about $70 a month. Similar coverage for Nancy costs $23. Total cost for all benefits? $5,296 annually. “The couple would be entitled to tax credits and deductions for some of those costs at tax time,” says Marr. “Of course, if Joel gets a new job with full benefits, the private insurance costs will go.”

Affiliate (monetized) links can sometimes result in a payment to MoneySense (owned by Ratehub Inc.), which helps our website stay free to our users. If a link has an asterisk (*) or is labelled as “Featured,” it is an affiliate link. If a link is labelled as “Sponsored,” it is a paid placement, which may or may not have an affiliate link. Our editorial content will never be influenced by these links. We are committed to looking at all available products in the market. Where a product ranks in our article, and whether or not it’s included in the first place, is never driven by compensation. For more details, read our MoneySense Monetization policy.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

In this excerpt from Wealthier, authors Daniel R. Solin and Mark McGrath offer practical tips on estate and financial...

First-time home buyers in Canada can pull from savings in registered accounts to fund their down payment. Here’s how...

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Swedish death cleaning is catching on in Canada. Learn how it can help you save money, simplify estate planning...

To minimize taxes and maximize benefits, learn the difference between deductions, credits and other forms of tax relief by...

Use the mortgage rate finder to compare the most current mortgage rates from the big banks and brokers instantly.

The federal government has made a last-minute change to its capital gains inclusion rate increase. However, other tax changes...

Ottawa defers effective date of capital gains changes to 2026 and promises exemptions for the tax inclusion increase.

If you’re looking for extra income to keep up with the rising cost of living, look no further than...