What is an RDSP?

Sponsored By

Concentra Trust

In Canada, people with disabilities and their families can open a registered disability savings plan to save for the future. Here’s how RDSPs work.

Advertisement

Sponsored By

Concentra Trust

In Canada, people with disabilities and their families can open a registered disability savings plan to save for the future. Here’s how RDSPs work.

When Selena Gusikoski and her family first came across promotional materials for the registered disability savings plan (RDSP), they didn’t open one right away. Gusikoski has five siblings, and her youngest brother, Cody, has a disability. The family works closely to make sure Cody can live an independent and fulfilling life, but because of his low income, the RDSP didn’t initially seem to make sense for him.

“We as a family had quite often received information about RDSPs from different organizations, but we always put it on the back burner,” says Gusikoski. “It was like, ‘Yeah, we’ll get to that.’”

Her family isn’t alone. More than 1.45 million Canadians are eligible to open an RDSP, but only about 36% of them had one as of the end of 2022, according to the most recent data from Statistics Canada.

A mere 17% of Canadians surveyed know about RDSPs, and many don’t understand how these registered accounts work, according to a recent study commissioned by Concentra Trust, an Equitable Bank company that provides services to a majority of Canada’s credit unions. Gusikoski, who is the director of registered plans at Concentra Trust, recounts how she didn’t realize the RDSP would be a good fit for Cody until she herself began exploring offering the RDSP as part of the company’s work with credit unions. Once she did, the benefits were immediately apparent.

“That was actually the perfect opportunity for me to go through the process from beginning to end,” says Gusikoski. “I quickly realized that the lack of awareness around the RDSP—including its government grants, its growth potential and how it works—has led to a huge missed opportunity for Canadians with disabilities.”

Introduced by the Canadian government in 2008, the registered disability savings plan is a registered account designed to help eligible people with a disability to save for the long term. RDSPs are offered by a variety of financial institutions, including credit unions.

To become an RDSP beneficiary, an individual must be approved to receive the federal disability tax credit (DTC), have a social insurance number (SIN), be a Canadian resident, and be under age 60. A beneficiary can only have one RDSP.

Like other registered accounts, an RDSP offers tax advantages: any growth in the account is not taxed until the funds are withdrawn. Grants, bonds and interest are taxed in the hands of the beneficiary, and personal contributions are not taxed.

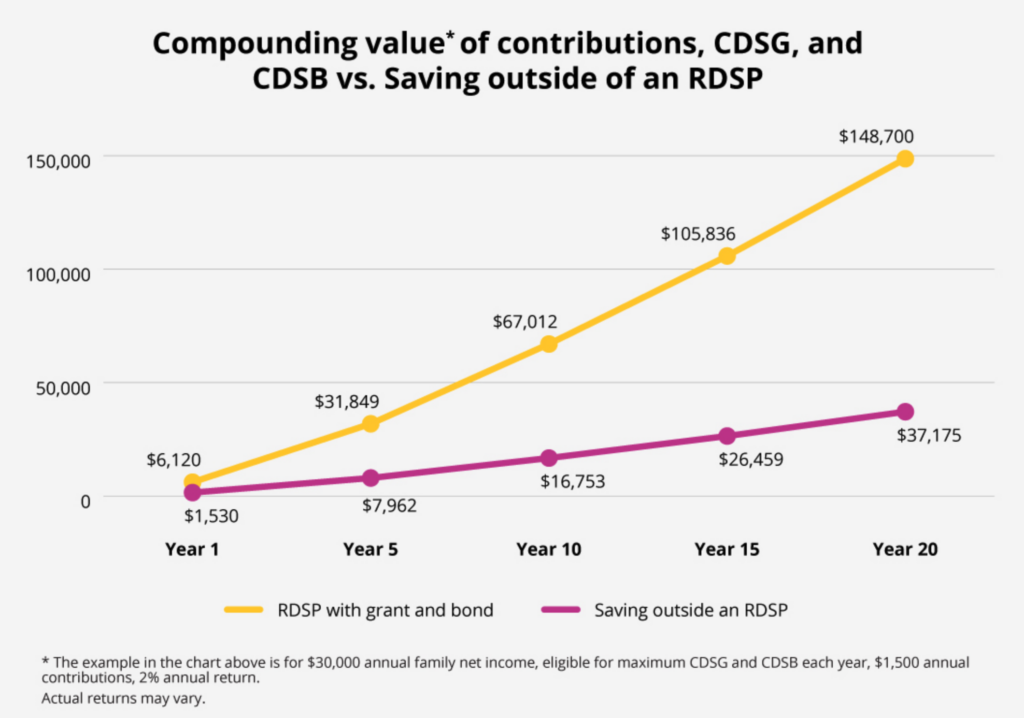

An RDSP consists of three segments: contributions, grants and bonds. Contributions are what you or your family make to the RDSP. Here’s how the grants and bonds work:

| Canada Disability Savings Grant (CDSG) | Canada Disability Savings Bond (CDSB) | |

|---|---|---|

| How it works | Paid out by the Government of Canada based upon how much you contribute and your family’s net income reported on tax returns two years prior (for example, 2024 grants and bonds are based on 2022 tax returns). The income thresholds are indexed annually by the Canada Revenue Agency (CRA). The CDSG is payable on contributions made until December 31 of the year the beneficiary reaches age 49. | Provided to RDSP holders with low to modest income, with no personal contribution necessary. The income thresholds are indexed annually by the CRA. The CDSB is payable until December 31 of the year the beneficiary reaches age 49. |

| Amount | For the 2025 calendar year, the maximum RDSP grant amount is $3,500 a year for those whose family income is $114,750 or less, and $1,000 for those with a family income over $114,750. | For the 2025 calendar year, $1,000 per year for those whose net family income is $37,487 or less, and a portion of $1,000 for those whose families earn a net income between $37,487 and $57,375. |

| Lifetime maximum | Up to $70,000 | Up to $20,000 |

You can check the Government of Canada’s website for RDSP matching rates for past years. And, to help Canadians estimate RDSP grants and bonds, the government has an RDSP calculator on its website.

Bonds and grants can help beneficiaries grow a modest contribution into a sizable safety net. Plus, the RDSP offers the ability to catch up on your contributions, grants and bonds over the previous 10 years once you’re approved for the DTC—this is known as a “carry forward”—so beneficiaries may be eligible for additional funds.

Gusikoski says that having money tucked away gives Cody a sense of pride and her family a sense of confidence that, should anything happen, he has a safety net of his own.

“It made a difference for our entire family,” she says. “Our mom was quite happy to know that there was a little nest egg for Cody in case he needs financial assistance in his later years. If his disability or his health declines, he has a little bit of money set aside. But it also made a difference for us siblings, because we’re a very close family and we do help each other out. If Cody needed something, it would be us, as his siblings, that would have to step in.”

RDSP contributions can be made via the financial institution that holds the RDSP or through a financial advisor or investment company that helps you manage your money.

The RDSP has no annual contribution limit, and the lifetime contribution limit is $200,000. An RDSP can hold more than cash, too—qualifying investments include guaranteed investment certificates (GICs), mutual funds and more.

You can make single RDSP withdrawals, called disability assistance payments (DAPs), or you can set up recurring withdrawals, called lifetime disability assistance payments (LDAPs).

Payments can be taken at any time, but generally grants and bonds must remain in the RDSP for 10 years to avoid repayment. You must make a request to your financial institution for each DAP, but LDAPs require just one request to set up. These recurring payments must start by the end of the calendar year you turn 60. Once you start receiving LDAPs, you’ll keep getting them until the end of your life or until the money is depleted, whichever comes first. In either situation, the RDSP will be closed.

Beneficiaries should be aware of the RDSP’s 10-year repayment rule. If any of the following things happen, all of the grants and bonds contributed to the account in the preceding 10 years must be returned to the federal government:

There are also provisions for when you can retrieve the money, like if your life expectancy drops below five years, or if you reach the age of 60, but Gusikoski cautions those looking at opening an RDSP to consider it a medium to long-term investment.

If you’re contemplating opening an RDSP, Gusikoski says that you’re doing something that is vital for the program’s health: educating yourself.

“Whether it’s $50 or $1,000, if you can get a minimum of 100% return on your money [from government grants], at a minimum, that is significant,” says Gusikoski. “And I think that if more people understood that, and if more people shared that information, contributions for people with RDSPs could really add up.”

But beyond that, for Gusikoski, there’s the joy of seeing her brother have a sense of financial independence. “It was really cool when I looked at his account statement with him, and we went through it and I explained everything to him. It made him feel really excited and empowered.”

Learn more about Concentra Trust’s RDSP program.

The survey was conducted by Equitable Bank for Concentra Trust among members of the Angus Reid Forum. The survey was conducted between Sept. 26 and 30, 2024, among a representative sample of 1,510 online Canadians who are members of the Angus Reid Forum. The survey was conducted in English and French. For comparison purposes only, a probability sample of this size would carry a margin of error of +/- 3 percentage points, 19 times out of 20.

Equitable Bank, and its wholly owned subsidiaries including Concentra Trust, does not offer tax advice. Please consult your financial advisor to discuss the tax-free benefits of an RDSP.

This is a paid post that is informative but also may feature a client’s product or service. These posts are written, edited and produced by MoneySense with assigned freelancers.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Financial milestones are changing for young Canadians. Here’s why experts say budgeting, saving, and consistency matter more than following...

Prediction markets are booming, but critics warn they can resemble gambling. Here's what investors need to know before trying...

Markets keep climbing despite economic headwinds. Allan Small explains why AI is driving growth and how investors can benefit...

The right cash allocation depends on your goals and stage of life. Here's how to think about cash in...

Reitmans narrowed its quarterly loss and Empire raised its dividend, but investors sent Groupe Dynamite and Gildan shares sharply...

Writing a will is easier and more affordable than many people think. Here's how Canadians can protect their assets,...

Investors seeking cash flow from real assets and inflation resistance should consider these infrastructure ETFs.

Optimization culture says that every dollar must be maximized and every latte is a betrayal of your future self,...

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.