Am I on track to retire early and travel?

Time to travel and spend more time with the grandkids

Advertisement

Time to travel and spend more time with the grandkids

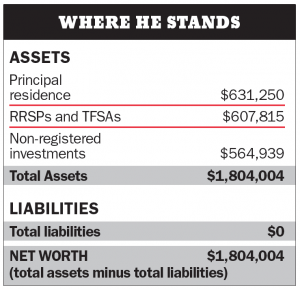

Rick Morrison, 58, would like to retire now. After working full time as an accountant in Edmonton for 35 years and raising five kids, he and his wife Anne, also 58, would like to kick back and enjoy some travel as well as spend more time with their two grandchildren in Calgary. After 15 years of marriage—a second marriage for both—Anne received an inheritance two years ago from her deceased mother’s trust that gives her a monthly income of $5,000 gross for life. Rick would like to match that monthly income, and hopes his $1.8 million in net worth—which includes a $1.17-million investment portfolio—will be enough. Right now, Rick says that 50% of his investments are in exchange-traded funds (ETFs) invested in Canadian dividend-paying shares, preferred shares and Canadian income trusts in a non-registered account. The average yield is 4.2% annually. The remaining 50% of his portfolio is in RRSPs and TFSAs that hold government and corporate bonds that yield 3.1%. Rick is eligible for full CPP and OAS at age 65. “I want to enjoy my grandkids and travel more to Europe and Asia,” says Rick. “I’m hoping my portfolio will be able to fund that.”

Rick Morrison, 58, would like to retire now. After working full time as an accountant in Edmonton for 35 years and raising five kids, he and his wife Anne, also 58, would like to kick back and enjoy some travel as well as spend more time with their two grandchildren in Calgary. After 15 years of marriage—a second marriage for both—Anne received an inheritance two years ago from her deceased mother’s trust that gives her a monthly income of $5,000 gross for life. Rick would like to match that monthly income, and hopes his $1.8 million in net worth—which includes a $1.17-million investment portfolio—will be enough. Right now, Rick says that 50% of his investments are in exchange-traded funds (ETFs) invested in Canadian dividend-paying shares, preferred shares and Canadian income trusts in a non-registered account. The average yield is 4.2% annually. The remaining 50% of his portfolio is in RRSPs and TFSAs that hold government and corporate bonds that yield 3.1%. Rick is eligible for full CPP and OAS at age 65. “I want to enjoy my grandkids and travel more to Europe and Asia,” says Rick. “I’m hoping my portfolio will be able to fund that.”

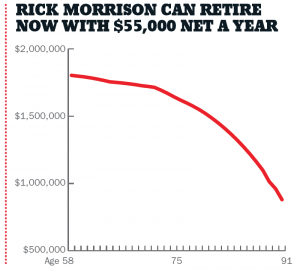

In order to take maximum advantage of the preferential tax treatment for dividends and capital gains, Rick should make withdrawals from his non-registered accounts until age 71, when he can convert his RRSP to a RRIF and make any future withdrawals from the RRIF. Gray recommends he take reduced CPP of $9,200 annually starting at age 60 and OAS of $5,700 annually at age 65—and to decrease the withdrawals from his portfolio to accommodate the extra retirement income. And what if Anne dies first and her $5,000 in monthly trust fund payments end? Or if Rick is still alive at age 90? “He can downsize his house and add the extra cash to his portfolio,” says Gray.

Do you want MoneySense to see if you’re on track to meet your own financial goal? If so, drop us a line at [email protected]

In order to take maximum advantage of the preferential tax treatment for dividends and capital gains, Rick should make withdrawals from his non-registered accounts until age 71, when he can convert his RRSP to a RRIF and make any future withdrawals from the RRIF. Gray recommends he take reduced CPP of $9,200 annually starting at age 60 and OAS of $5,700 annually at age 65—and to decrease the withdrawals from his portfolio to accommodate the extra retirement income. And what if Anne dies first and her $5,000 in monthly trust fund payments end? Or if Rick is still alive at age 90? “He can downsize his house and add the extra cash to his portfolio,” says Gray.

Do you want MoneySense to see if you’re on track to meet your own financial goal? If so, drop us a line at [email protected]

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Here’s how Canada’s Old Age Security pension works, who’s eligible for OAS, when you can start receiving OAS, and...

Here’s how Canada’s retirement pension plan works, who’s eligible for CPP, when you can start receiving CPP, and CPP...

There’s more than one way to optimize your income after retiring. Some strategies can boost wealth, and others may...

The senior vice president of retail and wealth at Meridian shares the importance of budgeting and investing in your...

Can Gen Z really afford to retire early? Here are some ways young Canadians can rethink the FIRE approach...

Here are the considerations before becoming a power of attorney for property and what to do if you’re unable...

Here are two ways to manage the effects of tariffs in Canada, plus three statements to prepare to ensure...

Economic uncertainty, inflation and the decline of workplace pensions have left growing numbers of seniors unable to leave their...

Canadians must begin taking RRIF withdrawals the year after converting an RRSP. What happens if you convert only part...