Making it on his own

Sam Omeretti's parents aren’t so sure he's ready to live on his own

Advertisement

Sam Omeretti's parents aren’t so sure he's ready to live on his own

This past spring, Sam quit college and got a full-time security job at the local mall. In July, he moved out of his parent’s home. While Gwen and Mauro are happy Sam is taking steps toward independence, they’re worried his new responsibilities will be difficult for him. “Two years of my coaching on prioritizing his spending has fallen on deaf ears,” says Gwen.

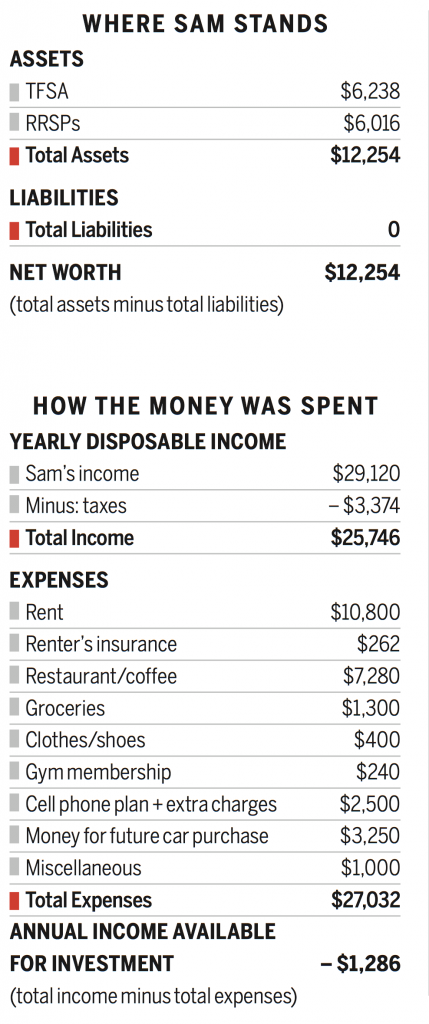

Truth is, Sam scraped through high school and dropped out in the first semester of college. “His free pass in high school caught up with him in college, which was a disaster,” says Gwen. Still, Sam does have a goal—to buy a used car. Right now, he earns $560 a week. And while Sam has set up a TFSA savings plan where he deposits $125 biweekly, the Omerettis worry about his free-spending ways. “He spends $20 a day on coffee and lunches out, not to mention the $140-a-month cell phone bill,” says Gwen. “And I don’t see how he’ll be able to afford the insurance and maintenance costs of a car.”

But Sam says he’s doing fine. “I don’t have debt and only borrow from friends when money is tight. I plan to buy a car when my account hits $10,000.”

For now, Sam says he’s done with school. Still, he’d like to budget better. His biggest expense is his cell phone bill—almost every month he goes over his data limit. It gets pricey with his August bill coming in near $400. While Sam plans to work full time this year, he doesn’t rule out college. “If I go back to college, I want to be ready,” he says, “but right now I’m doing okay and don’t want to be pushed.”

What the experts say

“Sam should take things one step at a time,” says Certified Financial Planner Julia Chung. “Rome wasn’t built in a day and the foundations of good money management aren’t either.” Here’s what Sam should do.

Check your cell phone usage. Sam should call his provider, get a usage analysis that includes asking how much data, talk and text he uses both on average and on evenings and weekends. Then he should ask what plan would best suit his usage. If it costs nothing, he should make the switch. But he should also find out when his cell phone contract ends, before shopping around at other providers, to find out if there’s a better offer elsewhere. “If he’s on a contract, it may not make good financial sense to move—or it might,” says Chung. “But a good analysis and a different plan should help lower his bill.”

Draw up a budget. “Sam needs a structure that make sense,” says Chung. His current net monthly pay is $2,125, while his current monthly bills are $1,239, but this doesn’t include the $240 he saves monthly to buy a car or his discretionary expenses. Since he’s paid biweekly, Chung suggests Sam create two bank accounts. One that’s not attached to his ATM card, where he puts his savings, and the other he’ll use to pay his bills. Then, “every paycheque he should allocate about half of his total monthly costs to the bill-paying account,” says Chung. After paying bills, Sam has about $443 left over from each paycheque, yet spends about $607 on restaurant meals and coffee. “Teaching Sam to meal plan, cook and grocery shop would be the way to go,” says Chung. “But if he doesn’t like cooking, then he should buy pre-packaged frozen meals which can cut his food bills in half.” If he manages to reduce his cell phone bill and spend less on food, he’ll be a bit ahead. “And he should stop lending between friends,” says Chung. “If one loan goes unpaid, friendships can be ruined.”

Set priorities. When he’s ready, Sam should find a mentor and start exploring career paths, while getting some help from people who specialize in job placement. “Formal education is not the only way to build a career,” says Chung. Once he’s made a decision about what the next five years of his life look like, then he can determine if it makes sense to put his money towards buying a car, or funding different goals. At that time, he’ll have to figure out what he’s willing to forgo in order to achieve these goals. “Then he can start talking to his parents about how they might want to help him fund his dreams,” says Chung. “When young adults are committed to a career path, most parents are more than willing to help.”

This past spring, Sam quit college and got a full-time security job at the local mall. In July, he moved out of his parent’s home. While Gwen and Mauro are happy Sam is taking steps toward independence, they’re worried his new responsibilities will be difficult for him. “Two years of my coaching on prioritizing his spending has fallen on deaf ears,” says Gwen.

Truth is, Sam scraped through high school and dropped out in the first semester of college. “His free pass in high school caught up with him in college, which was a disaster,” says Gwen. Still, Sam does have a goal—to buy a used car. Right now, he earns $560 a week. And while Sam has set up a TFSA savings plan where he deposits $125 biweekly, the Omerettis worry about his free-spending ways. “He spends $20 a day on coffee and lunches out, not to mention the $140-a-month cell phone bill,” says Gwen. “And I don’t see how he’ll be able to afford the insurance and maintenance costs of a car.”

But Sam says he’s doing fine. “I don’t have debt and only borrow from friends when money is tight. I plan to buy a car when my account hits $10,000.”

For now, Sam says he’s done with school. Still, he’d like to budget better. His biggest expense is his cell phone bill—almost every month he goes over his data limit. It gets pricey with his August bill coming in near $400. While Sam plans to work full time this year, he doesn’t rule out college. “If I go back to college, I want to be ready,” he says, “but right now I’m doing okay and don’t want to be pushed.”

What the experts say

“Sam should take things one step at a time,” says Certified Financial Planner Julia Chung. “Rome wasn’t built in a day and the foundations of good money management aren’t either.” Here’s what Sam should do.

Check your cell phone usage. Sam should call his provider, get a usage analysis that includes asking how much data, talk and text he uses both on average and on evenings and weekends. Then he should ask what plan would best suit his usage. If it costs nothing, he should make the switch. But he should also find out when his cell phone contract ends, before shopping around at other providers, to find out if there’s a better offer elsewhere. “If he’s on a contract, it may not make good financial sense to move—or it might,” says Chung. “But a good analysis and a different plan should help lower his bill.”

Draw up a budget. “Sam needs a structure that make sense,” says Chung. His current net monthly pay is $2,125, while his current monthly bills are $1,239, but this doesn’t include the $240 he saves monthly to buy a car or his discretionary expenses. Since he’s paid biweekly, Chung suggests Sam create two bank accounts. One that’s not attached to his ATM card, where he puts his savings, and the other he’ll use to pay his bills. Then, “every paycheque he should allocate about half of his total monthly costs to the bill-paying account,” says Chung. After paying bills, Sam has about $443 left over from each paycheque, yet spends about $607 on restaurant meals and coffee. “Teaching Sam to meal plan, cook and grocery shop would be the way to go,” says Chung. “But if he doesn’t like cooking, then he should buy pre-packaged frozen meals which can cut his food bills in half.” If he manages to reduce his cell phone bill and spend less on food, he’ll be a bit ahead. “And he should stop lending between friends,” says Chung. “If one loan goes unpaid, friendships can be ruined.”

Set priorities. When he’s ready, Sam should find a mentor and start exploring career paths, while getting some help from people who specialize in job placement. “Formal education is not the only way to build a career,” says Chung. Once he’s made a decision about what the next five years of his life look like, then he can determine if it makes sense to put his money towards buying a car, or funding different goals. At that time, he’ll have to figure out what he’s willing to forgo in order to achieve these goals. “Then he can start talking to his parents about how they might want to help him fund his dreams,” says Chung. “When young adults are committed to a career path, most parents are more than willing to help.”

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

The Alberta Child and Family Benefit is a provincial financial assistance program. Learn who’s eligible for the ACFB...

Want an idea of how much tax you paid—or will be paying—for 2024? Here are the federal and provincial...

Sponsored By

Coast Capital

Here’s how Canada’s retirement pension plan works, who’s eligible for CPP, when you can start receiving CPP, and CPP...

In this excerpt from her new book, Making Bank, Shannon Lee Simmons guides young Canadians (and their parents) through...

With all the personal finance advice on social media, it can be challenging to filter good from bad. Here’s...

Learn about Canada’s carbon tax, launched in 2019 and ended in 2025.

Here are two ways to manage the effects of tariffs in Canada, plus three statements to prepare to ensure...