Are they on track to retire at 50?

Adam Danyleko, 28, and Justine Oshust, 25, have a big mortgage but want to retire early with $100,000 in net income annually

Advertisement

Adam Danyleko, 28, and Justine Oshust, 25, have a big mortgage but want to retire early with $100,000 in net income annually

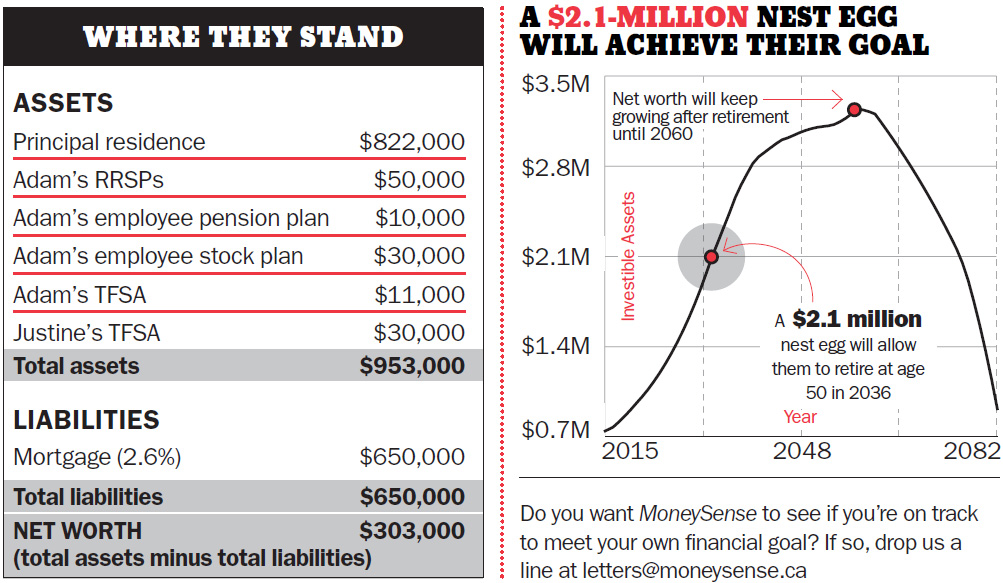

Do you want MoneySense to see if you’re on track to meet your own financial goal? If so, drop us a line at [email protected]

Do you want MoneySense to see if you’re on track to meet your own financial goal? If so, drop us a line at [email protected]

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

A University of Calgary study found that over one-third of senior homeowners worry about affording basic home maintenance, suggesting...

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

It’s almost impossible to do, but the mindset around spending all your savings can help you make the best of the...

Global conflicts affect Canadians’ finances in real time. Learn how rising costs, volatility, and uncertainty can impact your budget...

Silent divorces can quietly drive up financial stakes. Delays, hidden assets, and lack of formal separation can turn emotional...

Learn how to protect your family from inherited debt, unexpected taxes, and estate pitfalls. Experts share tips on wills,...

Explore retirement living options—from aging in place to assisted care—and learn how to start supportive, practical conversations with aging...

Retirement planning for couples with a significant age difference calls for realistic projections but also flexibility.

Money stress is straining relationships across Canada. Here’s what a new survey reveals, and how couples can have healthier,...

Many adult children know the basics of their parents’ money, but not the details. Discover why full financial visibility...