By Dale Roberts on October 14, 2022 Estimated reading time: 6 minutes

While the core Couch Potato philosophy is simple, effective and has yielded good historic concerns, the author feels they don't go far enough to protect against a broad range of economic conditions. Welcome to the advanced class.

This article is 2 years old. Some details may be outdated.

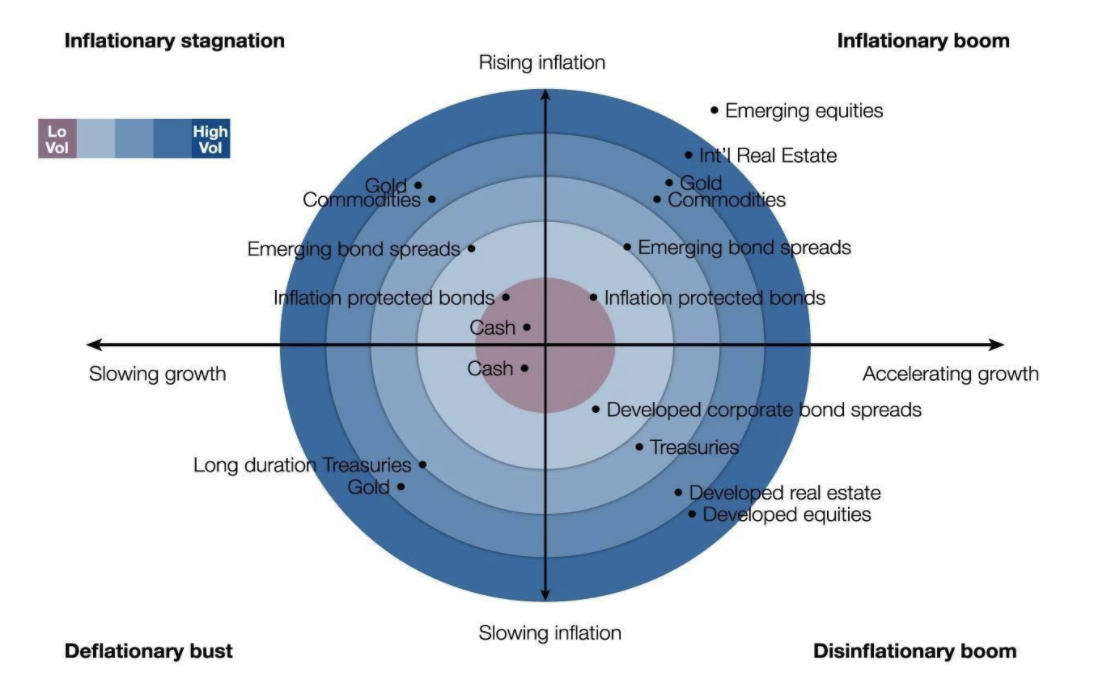

While the traditional Couch Potato portfolio mix of global equities and Canadian bonds is a simple and effective approach with good historical returns, it’s a bit too simple for my taste. The main problem is that it doesn’t cover investors for all economic conditions and fluctuations, which leaves numerous portfolio holes. For example, in the 1970s and early ’80s, there was an extended period of high inflation and stagnant economic growth, or what’s referred to as stagflation. It was a terrible combination in which few assets performed well. Gold, commodities, and real estate would have greatly helped portfolio returns during that period, as shown in the chart below. But those assets are mostly missing from a traditional Couch Potato portfolio, as well as many typical investment portfolios.Inflation may not be a concern for those in the accumulation stage, as stock markets are a very good long-term inflation hedge. And in fact, commodities can be a drag in the accumulation stage. That said, for those who are in retirement, or in the retirement risk zone, inflation and stagflation are both serious risks. Those retirees and near-retirees might consider these all-weather portfolio models. As you may have noticed, we have moved into a stagflation environment in 2022. In this article, I compared the returns of the core and advanced Couch Potato models.

Asset performance in various economic conditions

Source: ReSolve Asset Management

All-weather ETF portfolios

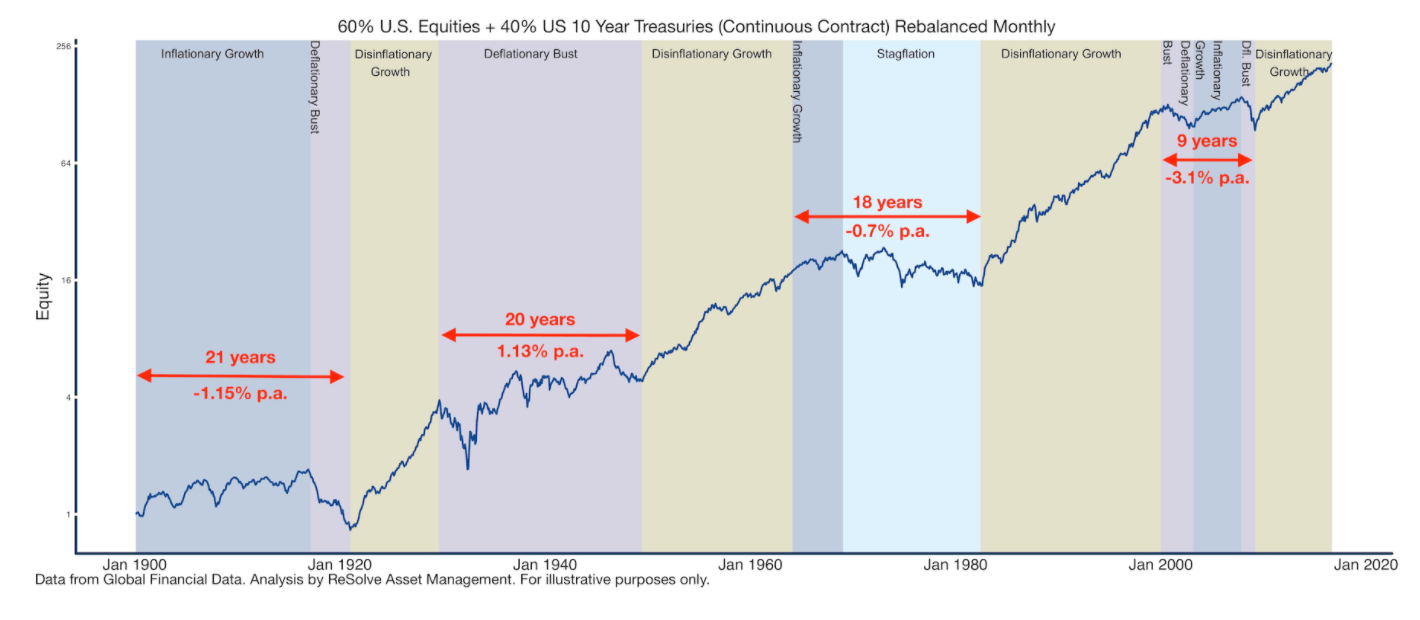

We can increase diversification and potentially reduce portfolio risk by adding some of these asset classes into our Couch Potato mix. This way, no matter what the economic conditions—growth or contraction accompanied by either inflation or deflation—you can hopefully have at least one asset that is delivering positive returns. There is always something working. A good example of the portfolio strategy is demonstrated by the Permanent Portfolio. In other words, we can build an “all-weather” Couch Potato portfolio. It is not well known, but even a balanced portfolio can fail for many years. The following chart uses U.S. stocks and U.S. bonds. An investor could improve the situation slightly by adding Canadian and global stocks, but the theme and risk to the balanced portfolio prevails. Source: ReSolve Asset ManagementStocks and bonds don’t always cut it. And sorry that I put a jinx on that. The traditional balanced portfolio is having one of its worst periods ever in 2022. Stocks have been correcting as well as bonds, the latter due to interest rates rising rapidly in the attempt to tame inflation. Here are the main assets we’ll add into our all-weather portfolios, with suggested ETFs:

U.S. treasuries. Long-term treasuries punch above their weight as risk managers for stock markets, because they increase to a greater degree than a total bond market fund. (Suggested: BMO Long-Term US Treasury Bond Index ETF, ticker ZTL, MER of 0.22%.)

Short-term bonds. These bonds can work like cash protecting against a rising rate environment, as is often experienced during inflationary periods. (Suggested:iShares Core Canadian Short Term Bond Index ETF, ticker XSB, MER of 0.1%.)

Long-term bonds. They are known to punch above their weight as stock market risk managers. That is, they offer more convexity (the ability to go up when stocks go down). (Suggested: BMO Long Federal Bond Index ETF, ticker ZFL, MER of 0.22%.)

Gold and commodities. These “real” assets are arguably the best inflation fighters. Gold is known as an inflation asset (although it doesn’t have a perfect record) and is also a safe-haven asset for when big geopolitical shocks occur. A basket of gold plus other commodities may offer a greater chance of success during a bout of serious inflation or stagflation. (Suggested: Purpose Diversified Real Asset ETF, ticker PRA, MER of 0.6%.)

Real estate investment trusts (REITs). Real estate is known for providing additional inflation protection. It is also an asset that often does not necessarily move in tandem with stock or bond markets, potentially adding additional diversification for a balanced portfolio. (Suggested: iShares Global Real Estate Index ETF, ticker CGR, MER of 0.72%. Note that PRA also holds REITs as a real asset; however, the total portfolio REIT exposure from PRA is small at just over 1%.)

Other. You could also consider adding real return bonds or TIPS that offer a yield plus an inflation adjustment as an additional inflation asset, and/or that new digital gold known as bitcoin. (Here’s an article on bitcoin that will help you to gain an understanding of this new asset.) Neither of these assets, however, are included in the sample all-weather portfolios below. To add bitcoin—many suggest a 5% portfolio weighting—you could trim from your real assets holding (PRA).

To round out the bond portfolio you could certainly consider corporate bonds and high yield corporate bonds.

A note on the regional allocation of stocks within the all-weather portfolios. We will add developing markets to the mix, and use separate ETFs for each of the Canadian, U.S. and developing markets. This avoids the global index weighting that currently greatly overweights the U.S. stock market, and instead allows us to hold Canadian, U.S. and international stock markets in equal weight.

Dale Roberts is a former investment advisor and proponent of low-fee investing. He created the Cut The Crap Investing blog in 2018. Find him on Twitter for market updates and commentary, every day.

I disagree. This is unnecessarily complicated for most investors. With investing simple invariably beats complex. As Jack Bogle says “Simplicity is the master key to financial success”.

It is also disingenuous to use a graph consisting of only US stocks and US 10 year treasuries to pan a 60/40 portfolio. That is nothing like a globally diversified portfolio of stocks and bonds such as VBAL. Let’s redo the graph with that evidenced based portfolio.

Interesting portfolio structure. Is there a minimum portfolio size you recommend for these investments? Especially if you have varied sided accounts in RRSP, SRRSP, TFSA and LIRAs.

Trying to get my around the fixed income side of things. Why is there not more discussion about convertible bonds? I currently have iShares CVD yielding 4.48% I guess there is risk to the principle but it doesn’t seem like much.

Would we as Canadians not be better suited to purchase the ZTL.F which is hedged to the Canadian dollar?

The bond portion of our portfolio should safe and we would not want our US treasuries to lose value if the Canadian dollar increased.

On the other hand if one bought ZTL.F, and the US dollar went up relative to CAD then our investment would decease.

Perhaps owning 50% ZTL.F and 50% ZTL for the US treasuries portion of the portfolio is the best bet.

Bogle would not approve of this complexity but I like the premise.

I really don’t see a difference between the Advanced Balanced Growth and Advanced Growth portfolios. Am I missing something?

I don’t see any difference in the last two portfolios, Advanced Balanced Growth Portfolio and Advanced Growth Portfolio?

The last two portfolios are exactly the same

Thanks for pointing out the error, Shawn Lawrence, BadDogTitan and Colin Reid – the copy has now been corrected, and the graphics will follow.

Where is the Advanced Growth Portfolio? Thanks

Sorry. Disregard last comment. I was looking for a 80 stock/20 fixed example

Hi.

Look like very good portfolios. Is there any performance data for these portfolios?

Thanks

I disagree. This is unnecessarily complicated for most investors. With investing simple invariably beats complex. As Jack Bogle says “Simplicity is the master key to financial success”.

It is also disingenuous to use a graph consisting of only US stocks and US 10 year treasuries to pan a 60/40 portfolio. That is nothing like a globally diversified portfolio of stocks and bonds such as VBAL. Let’s redo the graph with that evidenced based portfolio.

Sorry I don’t see the Advanced Growth portfolio in the article?

I’m hoping you’ll track these portfolios over time and report back to us.

Interesting portfolio structure. Is there a minimum portfolio size you recommend for these investments? Especially if you have varied sided accounts in RRSP, SRRSP, TFSA and LIRAs.

Trying to get my around the fixed income side of things. Why is there not more discussion about convertible bonds? I currently have iShares CVD yielding 4.48% I guess there is risk to the principle but it doesn’t seem like much.

Would we as Canadians not be better suited to purchase the ZTL.F which is hedged to the Canadian dollar?

The bond portion of our portfolio should safe and we would not want our US treasuries to lose value if the Canadian dollar increased.

On the other hand if one bought ZTL.F, and the US dollar went up relative to CAD then our investment would decease.

Perhaps owning 50% ZTL.F and 50% ZTL for the US treasuries portion of the portfolio is the best bet.

Bogle would not approve of this complexity but I like the premise.