Canadian stocks look cheap, and 4 other chart insights for 2019

Plus, will interest rates keep rising?

Advertisement

Plus, will interest rates keep rising?

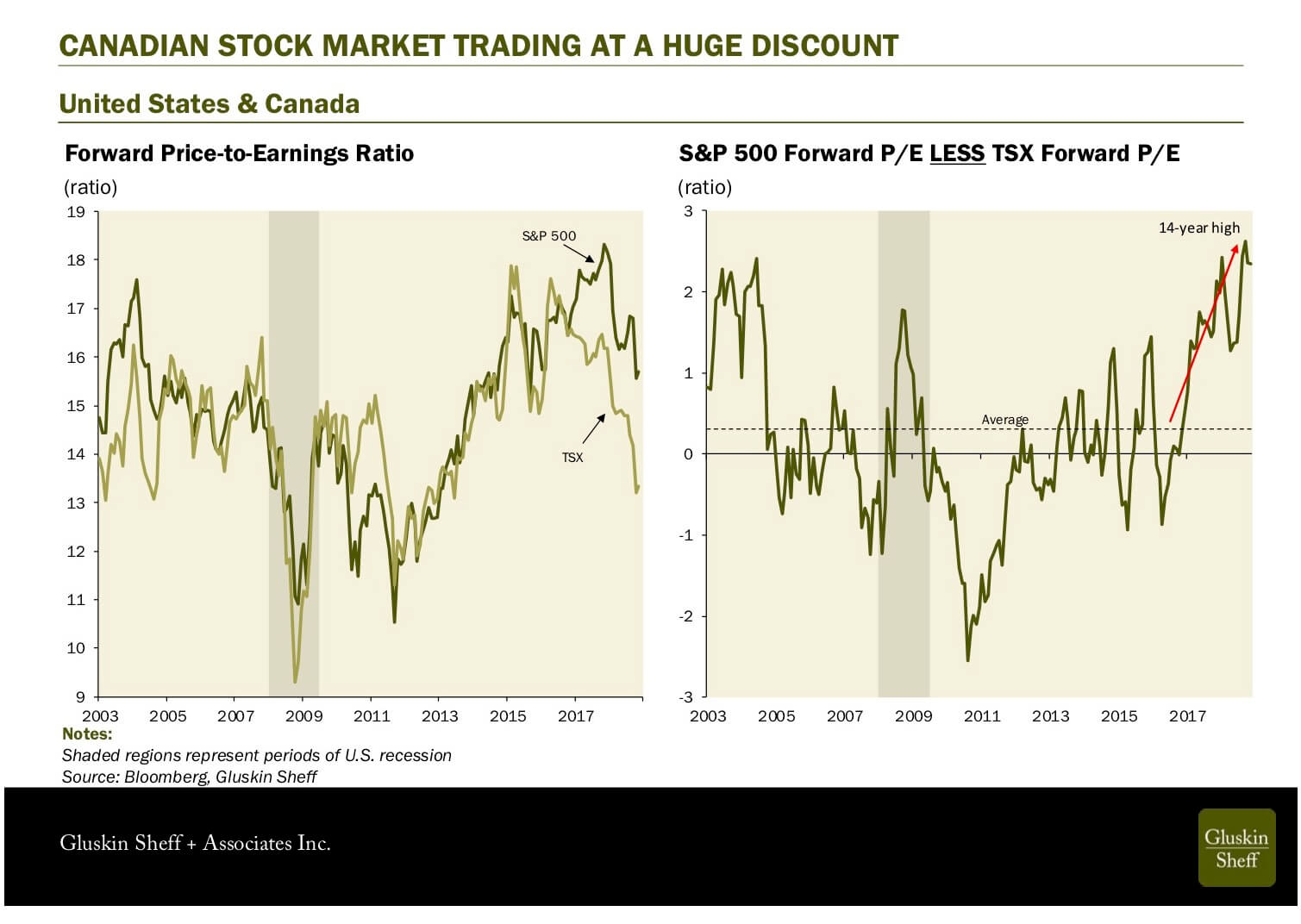

Rosenberg: “The macro news in Canada may indeed be bad, but that bad news is likely already in the price. Consider for a moment that there has been no bull market north of the border this cycle as there was in the United States. The Canadian stock market is no higher now than it was in the summer of 2008—ten years of nothing but a whole lot of volatility and your reinvested dividend in the blue-chip banks.

Yet corporate earnings have risen more than 30 per cent over this time frame, with nothing to show for it from a market price standpoint. In other words, the Canadian stock market is cheap. Dirt cheap. The forward price-earnings multiple (p/e) is beginning to resemble that of an emerging market, and no, despite our challenges, we are not anywhere close to being an emerging market. Not yet, anyway.

Rosenberg: “The macro news in Canada may indeed be bad, but that bad news is likely already in the price. Consider for a moment that there has been no bull market north of the border this cycle as there was in the United States. The Canadian stock market is no higher now than it was in the summer of 2008—ten years of nothing but a whole lot of volatility and your reinvested dividend in the blue-chip banks.

Yet corporate earnings have risen more than 30 per cent over this time frame, with nothing to show for it from a market price standpoint. In other words, the Canadian stock market is cheap. Dirt cheap. The forward price-earnings multiple (p/e) is beginning to resemble that of an emerging market, and no, despite our challenges, we are not anywhere close to being an emerging market. Not yet, anyway.

RELATED: As rates rise, dividend stocks could sufferThat p/e multiple has compressed all the way down to a mere 13.3 times, the lowest it has been in well over five years and the two-and-a-half percentage point discount that the S&P/TSX Composite Index trades at currently vis-à-vis the S&P 500 is the widest the valuation gap has been since June 2004 (normally, both markets trade with the same multiple). Canadian bears may want to dig into the history books because in the year that followed, the TSX rallied 16 per cent versus 4.5 per cent for the S&P 500. That was as tough a sell then as it is today, but either you believe in reversion-to-the-mean, or you don’t.”

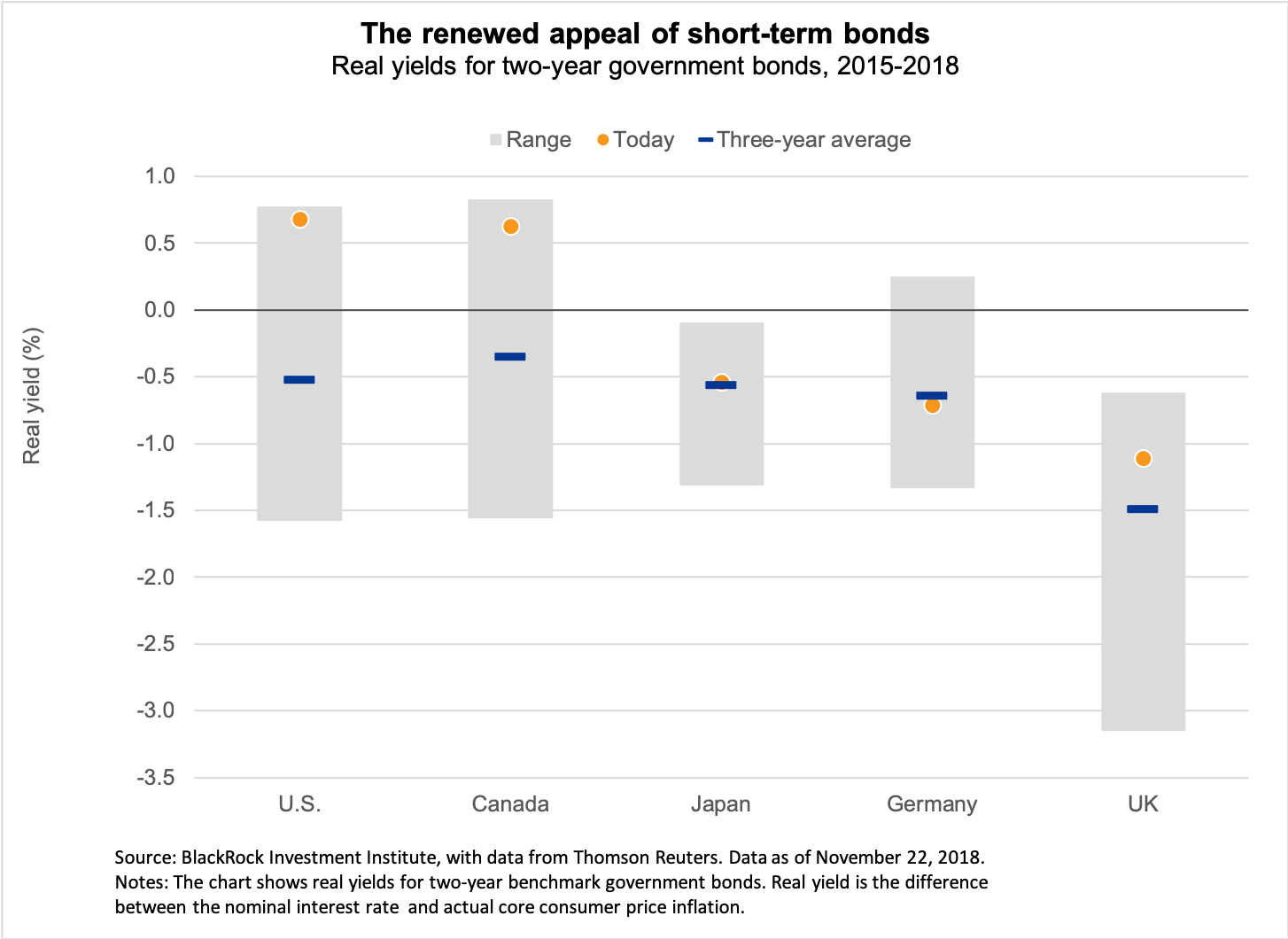

Reiman: “During much of the post-financial-crisis period, yields on shorter-maturity bonds failed to compensate investors for inflation. In other words, real interest rates were negative. After successive rate hikes by the Bank of Canada and the U.S. Federal Reserve, short-term interest rates now offer investors a positive real yield, which creates competition for capital and has likely contributed to recent bouts of stock market volatility. We think allocations to short-term government bonds benefit investors in three important respects: they provide higher yields than cash, they offer lower interest rate risk than longer-maturity bonds, and they provide ballast for the portfolio during periods of elevated uncertainty and financial market volatility.”

Reiman: “During much of the post-financial-crisis period, yields on shorter-maturity bonds failed to compensate investors for inflation. In other words, real interest rates were negative. After successive rate hikes by the Bank of Canada and the U.S. Federal Reserve, short-term interest rates now offer investors a positive real yield, which creates competition for capital and has likely contributed to recent bouts of stock market volatility. We think allocations to short-term government bonds benefit investors in three important respects: they provide higher yields than cash, they offer lower interest rate risk than longer-maturity bonds, and they provide ballast for the portfolio during periods of elevated uncertainty and financial market volatility.”

RELATED: How should your asset allocation change over time?

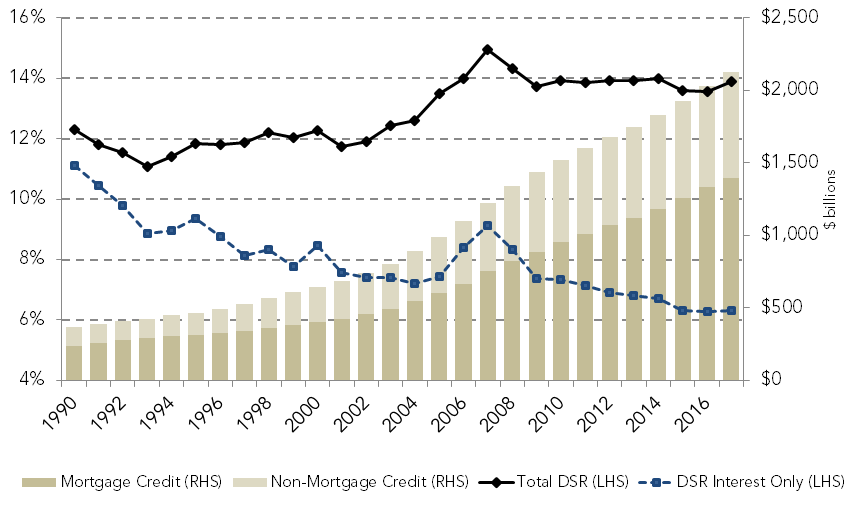

Scilipoti: “Since the financial crisis, Canadians have increased their indebtedness by over 50 per cent. Yet as a proportion of disposable income, the costs to carry said debt has remained constant.

Unfortunately, the regime of low interest rates is about to change. According to the BOC, the weekly effective interest rate for households, which is a weighted-average of mortgage and non-mortgage interest rates, reached 3.9 per cent in October 2018; the highest rate since March 2009. As higher rates flow through to outstanding retail credit, primarily from rate resets on fixed and variable rate mortgages, Canadian households are expected to experience rising DSRs for the first time since the financial crisis.

The BOC’s June 2018 Financial System Review analysis of the impact of higher rates from fixed mortgages renewals implies that the household DSR is expected to rise to around 14.9 per cent, matching the peak DSR reached in 2007. The rising DSR will put pressure on consumer spending, and based on our analysis, is a reliable leading indicator of higher delinquency rates and credit losses for Canadian banks. With the DSR already at 14.5 per cent in Q2-18, we caution investors that higher retail credit risk is around the corner and that investors should closely monitor their exposure to banks dependent on Canadian retail lending.”

Scilipoti: “Since the financial crisis, Canadians have increased their indebtedness by over 50 per cent. Yet as a proportion of disposable income, the costs to carry said debt has remained constant.

Unfortunately, the regime of low interest rates is about to change. According to the BOC, the weekly effective interest rate for households, which is a weighted-average of mortgage and non-mortgage interest rates, reached 3.9 per cent in October 2018; the highest rate since March 2009. As higher rates flow through to outstanding retail credit, primarily from rate resets on fixed and variable rate mortgages, Canadian households are expected to experience rising DSRs for the first time since the financial crisis.

The BOC’s June 2018 Financial System Review analysis of the impact of higher rates from fixed mortgages renewals implies that the household DSR is expected to rise to around 14.9 per cent, matching the peak DSR reached in 2007. The rising DSR will put pressure on consumer spending, and based on our analysis, is a reliable leading indicator of higher delinquency rates and credit losses for Canadian banks. With the DSR already at 14.5 per cent in Q2-18, we caution investors that higher retail credit risk is around the corner and that investors should closely monitor their exposure to banks dependent on Canadian retail lending.”

READ: A nearly $40,000 TFSA all-in on Canadian dividend stocks

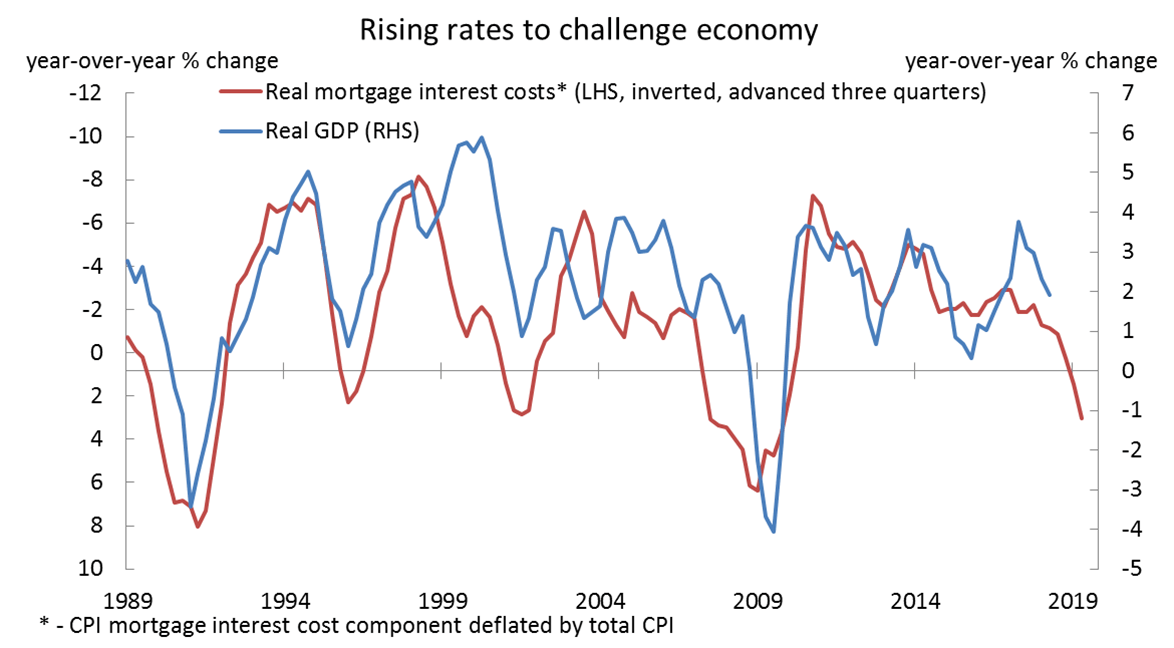

Wolf: “Interest rates have been going up. Canadians are more indebted than ever. Putting the two together, the period ahead is likely to be challenging for the Canadian economy. This chart puts a picture to that, showing that changes in Canadians’ real mortgage interest burden (inverted in the chart) leads growth in GDP by nearly a year—in other words, the higher that burden, the weaker the economy will tend to be. The historical relationship suggests the risk of recession in Canada in 2019, a risk that will intensify if interest rates continue to rise.”

Wolf: “Interest rates have been going up. Canadians are more indebted than ever. Putting the two together, the period ahead is likely to be challenging for the Canadian economy. This chart puts a picture to that, showing that changes in Canadians’ real mortgage interest burden (inverted in the chart) leads growth in GDP by nearly a year—in other words, the higher that burden, the weaker the economy will tend to be. The historical relationship suggests the risk of recession in Canada in 2019, a risk that will intensify if interest rates continue to rise.”

READ: Why Canadians invest too much at home

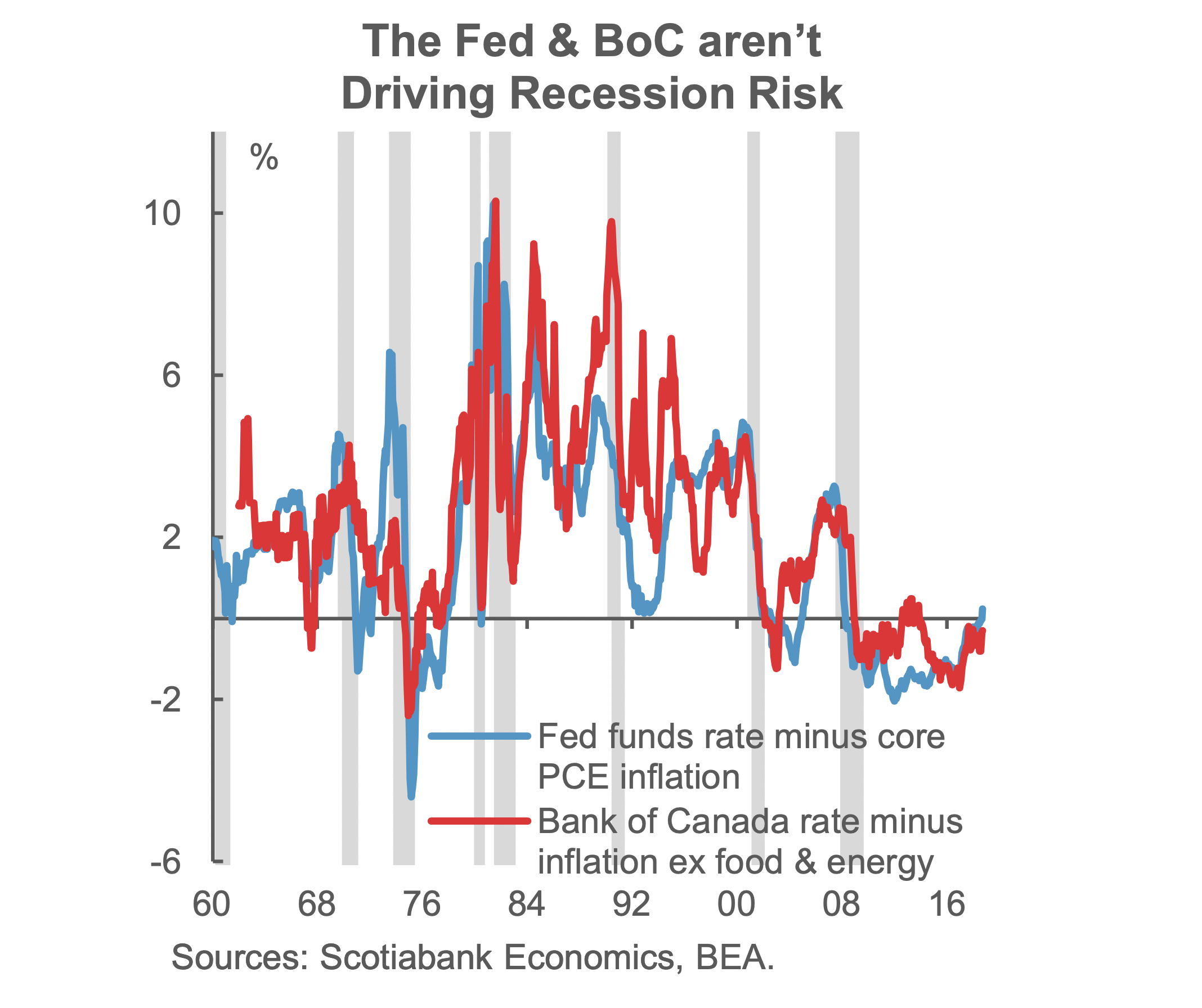

Holt: “Neither the Bank of Canada nor the Federal Reserve is on the verge of driving their respective economies into recession through rate hikes. The chart shows the inflation-adjusted policy interest rate in Canada and the U.S. over time with shaded vertical bars representing recession periods. The so-called ‘real’ rate is either about zero (U.S.) or about -0.5 per cent (Canada). Never before has either country entered recession driven by over-tightening of monetary policy with the real policy rate as low as it is today. As such, monetary policy remains stimulative to growth in both countries. Against guidance that 2019 will lead to interest rate relief for borrowers on such recession fears, it would be prudent and responsible for borrowers to prepare for further rate hikes within economies that have essentially exhausted slack and that are generating firm inflation pressures.”

Holt: “Neither the Bank of Canada nor the Federal Reserve is on the verge of driving their respective economies into recession through rate hikes. The chart shows the inflation-adjusted policy interest rate in Canada and the U.S. over time with shaded vertical bars representing recession periods. The so-called ‘real’ rate is either about zero (U.S.) or about -0.5 per cent (Canada). Never before has either country entered recession driven by over-tightening of monetary policy with the real policy rate as low as it is today. As such, monetary policy remains stimulative to growth in both countries. Against guidance that 2019 will lead to interest rate relief for borrowers on such recession fears, it would be prudent and responsible for borrowers to prepare for further rate hikes within economies that have essentially exhausted slack and that are generating firm inflation pressures.”

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

In the likelihood of a protracted conflict, these experts think people in or close to retirement need to review...

Look under the hood before buying some popular Canadian sector ETFs. There may be alternatives that better represent the...

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

Lululemon profits dip, Couche-Tard surges, and Power Corp declines. Here’s what investors need to know about Q4 results...

U.S.-Iran tensions have shaken markets, but experts urge investors to stay disciplined, avoid emotional moves, and use volatility to...

Canadian companies face a turbulent quarter, with Algoma Steel losing big and Transat posting gains amid major corporate moves.

Canadians moving to the U.S. may be able to unlock a locked-in RRSP after 24 months of non-residency—but tax...

Q4 shows mixed results across sectors: Canadian Natural and Pet Valu post gains, while George Weston and Canada Packers...

Bitcoin extends losses, down 47% since October 2025. When will the crypto bear market reverse, and what does the...