Is VFV a good buy? What about other U.S. ETFs with even lower fees?

Sure, VFV could be a good buy, but there are U.S. ETFs with even lower fees available for Canadian investors. Here’s how they stack up.

Advertisement

Sure, VFV could be a good buy, but there are U.S. ETFs with even lower fees available for Canadian investors. Here’s how they stack up.

With an average management expense ratio (MER) of 0.09% and collective assets under management (AUM) approaching $40 billion, exchange-traded funds like the Vanguard S&P 500 Index ETF (VFV), the BMO S&P 500 Index ETF (ZSP) and the iShares Core S&P 500 Index ETF (XUS) are some of the most cost-effective options for Canadian investors to get exposure to U.S. equities.

Sure, investing in these ETFs means you’ll forfeit 15% of your dividends to withholding tax. Yet, for many, it’s a worthwhile trade-off to gain access the most significant U.S. equity index—a benchmark that, according to the Standard & Poor’s Indices Versus Active (SPIVA) report, has outperformed 88% of all U.S. large-cap funds over the past 15 years.

But hold on, these aren’t your only choices. And here’s something you might not know: they aren’t even the cheapest around. Just like opting for no-name brands at the store can offer the same quality for a lower price, other ETF managers have been quietly rolling out competing U.S. equity index ETFs that come with even lower fees. Here’s what you need to know to make an informed choice.

Exploring cheaper alternatives to the well-known S&P 500 ETFs—like VFV, ZSP and XUS—leads us to a pair of lesser known but highly competitive options: the TD U.S. Equity Index ETF (TPU) and the Desjardins American Equity Index ETF (DMEU). Launched in March 2016 and April 2024, respectively, these ETFs track the Solactive US Large Cap CAD Index (CA NTR) and the Solactive GBS United States 500 CAD Index. The “CA NTR” stands for “net total return,” which means the index accounts for after-withholding tax returns, providing a more accurate measure of what Canadian investors might take home.

Essentially, these indices offer U.S. equity exposure without the licensing costs associated with the brand-name S&P 500 index, which is a significant advantage for keeping expenses low. You can think of Solactive as the RC Cola of the indexing industry, and S&P Global as Coca-Cola, and MSCI as Pepsi.

For TPU, the management fee is set at 0.06%, with a total MER of 0.07%. DMEU charges a management fee of just 0.05%. Since it hasn’t been trading for a full year yet, its MER is still to be determined but is expected to be competitively low.

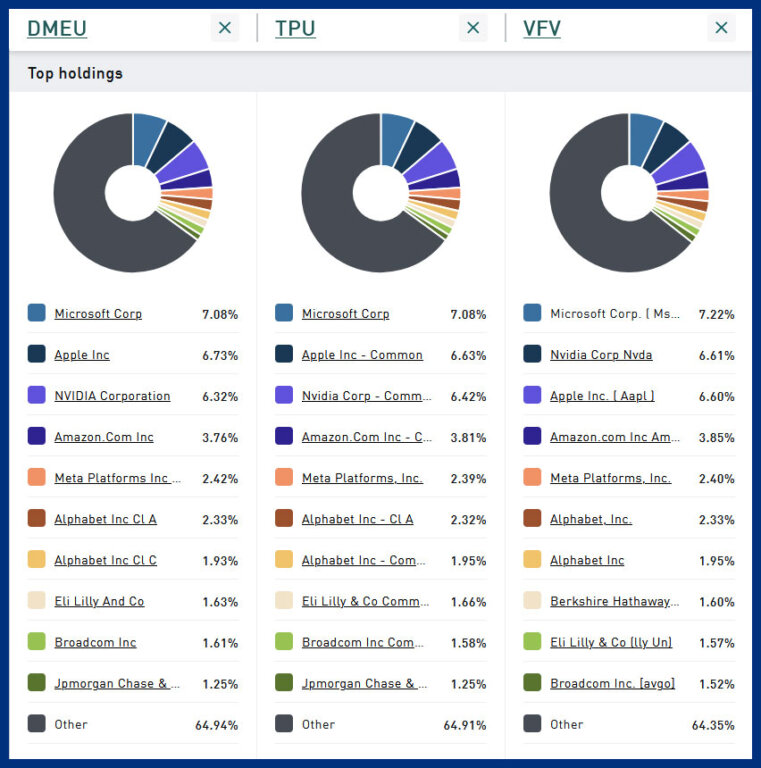

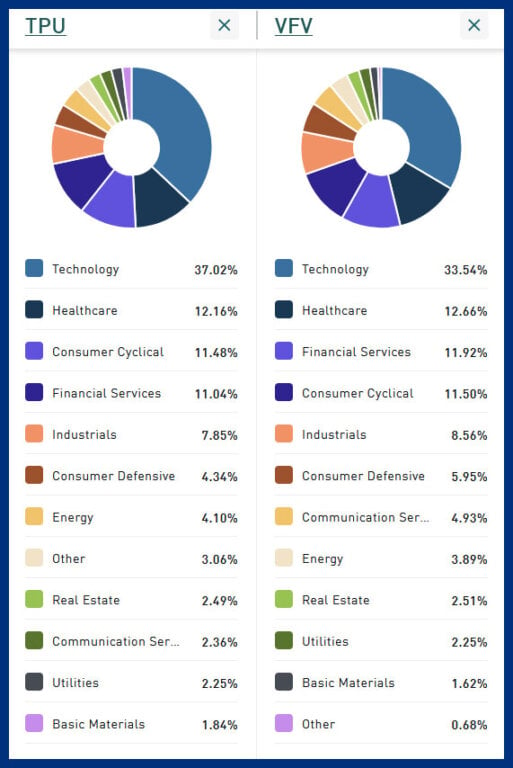

In terms of portfolio composition, there’s scant difference between the these ETFs: VFV, TPU and DMEU. Glance at the top 10 holdings, and you’ll see the weightings of these ETFs reveals very similar exposure, with only minor deviations. Similarly, when comparing sector allocations between TPU and VFV, they align closely, reflecting a consistent approach to capturing the broad U.S. equity market. However, look a bit deeper into the technical aspects, the indices that these ETFs track—the Solactive indices for TPU and DMEU versus the S&P 500 for VFV—exhibit some notable differences.

The S&P 500 is not as straightforward as it might seem, though. It doesn’t just track the 500 largest U.S. stocks. Instead, what is included is at the discretion of a committee, subject to eligibility criteria including market capitalization, liquidity, public float and positive earnings. This makes it more stringent and somewhat more active than you might have thought.

In contrast, the Solactive indices used by TPU and DMEU are more passive. They simply track the largest 500 U.S. stocks by market cap, with minimal additional screening criteria. This straightforward approach lends a more passive characteristic to these indices compared to the S&P 500.

Yes and no. Practically speaking, I expect all three ETFs—TPU, DMEU, and VFV—to perform more or less the same over the long run, barring minor, statistically insignificant deviations. As time progresses, these differences are likely to become even less pronounced in performance.

It’s important to note that both TPU and DMEU, while having lower trading volumes compared to VFV, still offer very good liquidity. This is because ETF liquidity is primarily determined by the liquidity of the underlying assets. In the case of TPU and DMEU, the two ETFs focus on large-cap U.S. stocks, similar to those found in the S&P 500, which are among the most liquid in the market. As a result, Canadian investors can expect low bid-ask spreads—often just one to two cents—on either ETF, ensuring efficient trading conditions.

Another significant advantage of holding TPU, DMEU or VFV pertains to tax-loss harvesting. Although TPU, DMEU, and VFV have similar holdings and sector weights, and are likely to perform similarly, they track different indices. This distinction is crucial under the Canada Revenue Agency’s (CRA) superficial loss rule, which prevents taxpayers from claiming a capital loss for tax purposes if they or someone affiliated buys the same asset within 30 days before or after it is sold.

Since these ETFs are not considered “substantially identical” due to the differences of their underlying indices, you could, for example, sell VFV to lock in a capital loss and immediately reinvest the proceeds into TPU or DMEU. This strategy allows you to stay invested in the market without waiting 30 days.

Tax-loss harvesting, or tax-loss selling, is a strategy for reducing tax in non-registered accounts. Investors sell money-losing investments, triggering capital losses they can use to offset capital gains incurred the same year. Tax losses can also be carried back three years or carried forward indefinitely. When using this strategy to save on taxes, take care to avoid triggering the superficial loss rule.

Read the full definition of tax-loss harvesting in the MoneySense Glossary.

The S&P 500’s strong brand value heavily influences investor choices, often leading many to select ETFs like VFV due to familiarity and historical performance. However, it’s worth considering alternatives, like TPU and DMEU, which offer slightly lower fees that could translate into substantial savings over time without compromising performance or risk.

While the allure of a well-known index is powerful, the financial benefits of these less expensive ETFs should not be overlooked, especially for those aiming to optimize long-term investment returns.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Quarterly results show profit gains at Cogeco, Roots and BlackBerry despite ongoing revenue pressure and uneven forward guidance.

Experts say rising geopolitical tensions and higher defence budgets are reshaping investing strategies, with opportunities spanning weapons, tech and...

ETFs

The MoneySense 2026 Best ETF panellists each pick a fund they’d leave in their portfolios if they were stranded...

A JD Power survey finds fintechs leading on satisfaction and innovation, while more DIY investors plan to seek human...

The first quarter finally broke the pattern of steadily rising markets, but energy stocks soared.

Geopolitics, rising oil prices and ETF inflows are shaping Bitcoin’s outlook. Is now the right time for Canadian investors...

Wealthsimple's direct indexing brings a tax-saving investing strategy to a wider group of investors, but the number likely to...

In the likelihood of a protracted conflict, these experts think people in or close to retirement need to review...