What seasoned investors look for in an ETF prospectus

Sponsored By

National Bank Direct Brokerage

Canadian investors who want to buy ETFs can learn a lot from a fund’s fact sheet and prospectus. Here are the details to focus on.

Advertisement

Sponsored By

National Bank Direct Brokerage

Canadian investors who want to buy ETFs can learn a lot from a fund’s fact sheet and prospectus. Here are the details to focus on.

It’s fair to argue that exchange-traded funds (ETFs) have changed the investing landscape for the better by providing easy access to low fees and broad diversification. With more than 4,300 ETFs to choose from on Canadian and U.S. exchanges, it can be difficult for investors to make their selection. Your online brokerage platform may offer ETF screening tools to help narrow the field.

All ETFs aren’t created alike. Differences can include the management style (for example, active versus passive), investment objective (income versus total return), benchmark index (broad market versus narrow market) and even regulatory structure.

In Canada, ETF providers must prepare and file a four-page “ETF Facts” sheet, as well as a long-form prospectus, for each fund they offer. These documents are filed with Canadian Securities Administrators and made available on SEDAR (the electronic filing system for public securities documents in Canada), as well as the fund providers’ websites.

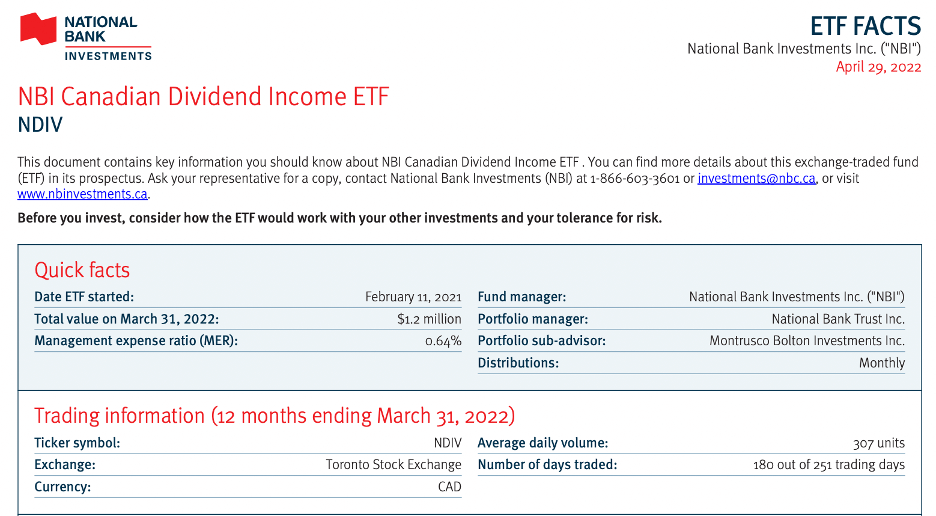

Most investors can get the information they need about an ETF from its fact sheet. It’s a plain-language summary of the fund where investors can find the following key information:

You’ll also find quick facts such as the ETF’s inception date, its current assets under management (AUM), its management expense ratio (MER), the name of the fund manager, how often distributions are paid, the fund’s ticker symbol, the stock exchange on which it trades, and the currency in which it trades.

ETF Facts sheets are required to be filed and posted at least annually and every time there is a material change to the fund. Investment dealers are also required to deliver the ETF Facts sheet to you no later than midnight on the second business day following the purchase of ETF securities.

Here’s an example of an ETF Facts document from National Bank Investments, showing the first of four pages, including the “Quick Facts” summary:

There’s only so much information that can be shared in the four-page fact sheet. A long-form prospectus can give investors a better look underneath the hood, especially for an ETF that uses a complicated investment strategy.

All ETFs are required to provide a long-form prospectus. This document includes information including basic disclosures, fees, expenses, returns, legal structure, investment objectives, investment strategies, an overview of the investment structure, an overview of the sectors the fund invests in, risk factors, distribution policy and income tax considerations (to name a few).

It’s rare that an investor would need to pull up an ETF’s long-form prospectus to learn more about a fund. But a prospectus does offer more in-depth information about fees, risk factors and even the taxation of the ETF that’s worth knowing.

According to the Ontario Securities Commission, an investment fund can distribute securities under its prospectus for up to 12 months before the prospectus lapses. The prospectus can be renewed for an additional 12 months, provided certain conditions are met.

Bobby Argitis, business development manager with National Bank Direct Brokerage, says it would be appropriate for investors to look through an ETF prospectus to glean more information about complicated ETFs.

“A good example is an ETF that uses derivatives and leverage to meet its investment objectives,” he says.

For instance, the fact sheet for National Bank Investments’ Liquid Alternatives ETF (NALT) states that its “objective is to provide a positive return while maintaining low correlation to, and lower volatility than, the return of the global equity markets.” It does this by investing in long and short positions on financial derivatives, and it may introduce leverage of up to 300% of its net asset value (NAV), meaning the total assets minus total liabilities.

A seasoned investor may be interested in knowing more details about the ETF’s investment approach and risk factors. For this, we can turn to the investment firm’s prospectus for its 16 ETFs, including NALT. On page 12, we learn that the fund uses computer models and a rules-based approach to determine its long and short positions. We’d also see that the fund uses futures contracts to provide exposure to bonds, currencies, equities or commodities.

The prospectus also explains that NALT determines its leveraged position at the end of each business day, and if its exposure exceeds 300% of its NAV, it will reduce its exposure to 300% or less, “as quickly as is commercially reasonable.” (Visit NBI full details about its ETFs.)

Investors with a keen eye for detail will notice other ETF documents such as monthly profiles, yearly reports and quarterly disclosures, as well as distribution and tax information.

Benjamin Felix, a portfolio manager at wealth management firm PWL Capital, says at least two of these documents are worth reviewing. “The annual management report of fund performance (MRFP) has good details like portfolio turnover and trading expense ratio. The annual financial statements contain securities lending income and foreign withholding tax. Together, those details are important for understanding the total cost of ownership of a fund,” says Felix. (Learn more about reviewing financial statements.)

For passive index investors, it can also be insightful to review the index methodology from the index provider. “Many indexes with similar names may be materially different, and some proprietary indexes may look more like actively managed funds,” says Felix. “This problem is documented in Robertson (2019).”

Many do-it-yourself investors can get the information they need about a particular ETF from its ETF Facts sheet. But it can be helpful to explore other documents, such as the long-form prospectus, to better understand the investing methodology, risk factors, fees and tax considerations—especially when it comes to more complicated or exotic ETF structures.

Investors can glean further information from documents such as the annual report and annual financial statements to determine the total cost of ownership of a fund, including often-misunderstood items such as securities lending activity and foreign withholding tax.

At the very least, DIY investors should read the ETF fact sheet before investing. A deep dive into the ETF prospectus is never a waste of time—after all, don’t you want to know what you’re buying?

Your investing platform may also have helpful resources. Among other tools, National Bank Direct Brokerage has a dedicated ETF Centre that helps users search for funds based on industry, management style, annual fees and more. Investors can also hone their skills with a wide range of articles, videos, tutorials and seminars. National Bank Direct Brokerage also has a free mobile app for iOS and Android. On your smartphone or tablet, you can trade stocks and ETFs online at $0 commission, create watchlists, set up alerts for specific stocks, transfer funds, and more.

MoneySense ranked National Bank Direct Brokerage as the best online broker for ETF investing in 2021 and 2022. Use the promo code MoneySense when you open an account* and you’ll pay no commissions on transactions.

This is a paid post that is informative but also may feature a client’s product or service. These posts are written, edited and produced by MoneySense with assigned freelancers.

Affiliate (monetized) links can sometimes result in a payment to MoneySense (owned by Ratehub Inc.), which helps our website stay free to our users. If a link has an asterisk (*) or is labelled as “Featured,” it is an affiliate link. If a link is labelled as “Sponsored,” it is a paid placement, which may or may not have an affiliate link. Our editorial content will never be influenced by these links. We are committed to looking at all available products in the market. Where a product ranks in our article, and whether or not it’s included in the first place, is never driven by compensation. For more details, read our MoneySense Monetization policy.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Nvidia plans to manufacture AI chips in the U.S. for the first time.

Canada’s Consumer Price Index fell in March amid the start of a tariff war with the U.S., the end...

There are several personal, trust and corporate income-tax-filing extensions for Canadians this year. Which ones apply to you? ...

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

Want an idea of how much tax you paid—or will be paying—for 2024? Here are the federal and provincial...

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Investing in gold seems like a throwback, yet this precious metal is hitting new highs and attracting new investors....

Here’s how proposals from the NDP, Liberals, Conservatives and Green Party could affect your cash flow—and maybe help decide...

Cineplex, Roots, Corus Entertainment, Cogeco and Delta Air Lines reported earnings this week. Here are the details for Canadian...

Young investors have many ways to build the fixed-income portion of their portfolios. Experts say to keep these two...