Making sense of the markets this week: April 21, 2024

Capital gains tax inclusion rate will increase (for some), Netflix chills, U.S. bank earnings solid, and will the loonie sag on inflation?

Advertisement

Capital gains tax inclusion rate will increase (for some), Netflix chills, U.S. bank earnings solid, and will the loonie sag on inflation?

Kyle Prevost, creator of 4 Steps to a Worry-Free Retirement, Canada’s DIY retirement planning course, shares financial headlines and offers context for Canadian investors.

After talking a lot about how we really—finally—need to get serious about the decades-long issue of Canadian productivity decline, the federal government decided that perhaps it wasn’t such a big priority at all.

Tuesday’s federal budget had a lot of changes in it, and MoneySense’s columnist and Certified Financial Planner Jason Heath has an excellent breakdown of how the 2024 federal budget might affect you and your finances.

But for the purposes of commenting on Canada’s productivity, we’ll focus exclusively on the changes to the taxation of capital gains. Until Tuesday’s announcement (which takes effect in 10 weeks) only 50% of a capital gain was included as taxable income on your annual tax return. That inclusion rate will now be 66.67% for capital gains within corporations and trusts. For individuals, the new inclusion rate will be applied to all capital gains over the $250,000 threshold each year.

A few brief points for consideration on who these new taxes rules might affect:

While reasonable people can disagree on who should shoulder a higher tax burden and what is considered a “fair share” in Canada, there is no doubt that these new taxes will continue to discourage investment within our country. (Read: How will the changes to capital gains in Canada affect tech sector?) It’s also part of a budget that added substantially more complexity to our already-too-complex tax code. The sheer difficulty of calculating your taxes and trying to plan for long-term tax efficiency in Canada is yet another drag on productivity.

Former finance minister Bill Morneau was politely scathing in his commentary on the new changes, saying: “This was very clearly something that, while I was there, we resisted. We resisted it for a very specific reason—we were concerned about the growth of the country… I don’t think there’s any way to sugar coat it. It’s a challenge. It’s probably very troubling for many investors.”

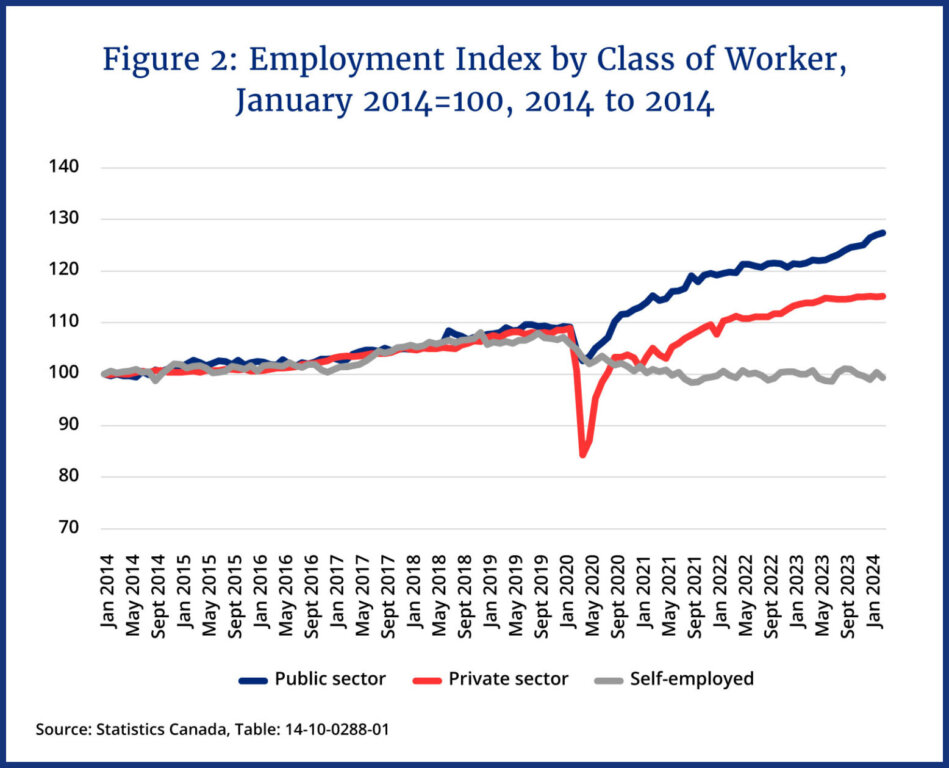

The rush to raise taxes versus finding efficiencies in current government spending is a tough pill to swallow for many, especially in light of the exploding numbers of public employees in Canada.

From the chart above, it doesn’t appear that Canadians were lacking for reasons not to start their own corporations or invest in innovative growth.

Perhaps the silver lining is that accountants and financial planners will likely be quite happy with these changes. The more complicated we make the tax code, the more valuable tax-savvy advice becomes, especially for long-term planning. It will be interesting to see how many Canadians choose to sit on their capital gains, hoping that the next government reverses course before they have to realize any taxable income. That might be a big gamble, as the next elected government might choose to raise capital gains even higher (depending on which party ends up in a minority or majority government).

For more reading, MoneySense investing editor-at-large Jonathan Chevreau summed up the immediate reaction of financial experts and mainstream media in regards to these changes on his website Findependencehub.com, and you can read my take on the new capital gains rules at MillionDollarJourney.com.

Netflix had a massive earnings per share beat on Thursday but presented a cautious forecast for the rest of the year.

All figures are in U.S. currency.

Perhaps the biggest takeaway from the earnings report was that streaming memberships were up 16% (to 269.6 million) in the first quarter of 2024, which were well above the 264.2 million predicted. But with that high note, Netflix also stated it would no longer be reporting membership numbers going forward, as the company is now more focused on profit and free cash flow as its metrics of choice.

Despite the solid first-quarter bottom line, Netflix’s slight downgrade of future projected revenues had shares down 5% in after-hours trading on Thursday. And according to Reuters, shares were down as much as 6.22% to $572.58 in premarket trading Friday.

That said, shareholders are likely still pretty happy with the company, as Netflix shares are up about 80% over the last year.

Netflix co-CEO Ted Sarandos highlighted the company’s first forays into live programming and video games, saying “We’re in the very early days of developing our live programming and I would look at this as an expansion of the types of content we offer, the way we expanded to film and unscripted and animation and most recently games. We believe that these kinds of event cultural moments like the Jake Paul and Mike Tyson fight are just that kind of television, and we want to be part of winning over those moments with our members as well, so that for me is the excitement part of this.”

Get up to 3.00% interest on your savings without any fees.

Lock in your deposit and earn a guaranteed interest rate of 3.40%.

Earn 4.50% for 5 months on eligible deposits up to $500k. Offer ends January 31, 2026

MoneySense is an award-winning magazine, helping Canadians navigate money matters since 1999. Our editorial team of trained journalists works closely with leading personal finance experts in Canada. To help you find the best financial products, we compare the offerings from over 12 major institutions, including banks, credit unions and card issuers. Learn more about our advertising and trusted partners.

U.S. bank earnings herald the beginning of a new season of earnings reports. The first quarter was largely kind to the banking sector, with every company beating earnings predictions.

All figures below are in U.S. dollars.

While all the banks posted strong results, those that rely more heavily on investment banking for their revenues (Goldman Sachs and Morgan Stanley) had the best quarters.

Goldman CEO David Solomon sounded confident on his earnings call, as he stated “I’ve said before that the historically depressed levels of activity wouldn’t last forever. CEOs need to make strategic decisions for their firms, companies of all sizes need to raise capital, and financial sponsors need to transact to generate returns for their investors… It’s clear that we’re in the early stages of a reopening of the capital markets.”

Another through line for the banks was that net interest income (revenue minus interest-bearing assets and interest-bearing liabilities expenses) was down as rates for interest-bearing deposits are finally catching up to the interest rates charged on loans.

All the big banks report reductions of potential credit losses (PCLs), showing unexpected confidence in the American consumer and the broader overall economy. (The more loans that banks feel will default in the near future, the more PCLs they must have on hand to “soak up” the loss.)

JP Morgan CEO Jamie Dimon said that while his company’s first-quarter performance was “strong,” he was less certain about the overall economy. “Many economic indicators continue to be favorable. However, looking ahead, we remain alert to a number of significant uncertain forces including overseas conflict and inflationary pressures.”

Buried under the big budget news on Tuesday was the most recent consumer price index (CPI) report released by Statistics Canada.

March saw a rise of 2.9% in the CPI on a year-over-year basis, which was a slight increase in the rate of inflation from February.

Notable inflationary figures included:

Given that monetary policy has a substantial lag time, it’s unlikely that the Bank of Canada (BoC) will wait until headline CPI or CPI-trim hits 2% before it decides to cut rates. The divergence between Canadian and American inflation is likely to lead to some uncomfortable trade-offs.

Currency markets are clearly anticipating that increased U.S. inflation will lead to “higher for longer” interest rates. If the BoC begins to cut interest rates before the Fed does, look for the Canadian dollar to continue its sharp decline (it’s down 4% vs the USD since December).

With thousands of Canadians avidly awaiting interest-rate drops so that they can deploy their shiny new-ish first home savings account (FHSA) and stretch the Home Buyer’s Plan further, we could soon see housing prices continue their sky-high climb.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

A recent EQ Bank survey found that more Canadians are relying on this year’s tax refunds to pay for...

It’s almost impossible to do, but the mindset around spending all your savings can help you make the best of the...

In the likelihood of a protracted conflict, these experts think people in or close to retirement need to review...

Home exchanges are changing how we travel, making it more affordable, flexible, and personal. Here’s how platforms like HomeExchange...

Filing your 2025 taxes in 2026? Here are the key changes, cancelled credits, and CRA updates Canadians need...

If it feels impossible to get ahead, you’re not imagining it. Here’s how inequality and policy choices are...

Look under the hood before buying some popular Canadian sector ETFs. There may be alternatives that better represent the...

Rising costs, debt, and delayed planning are leaving many Canadians unprepared. Here’s what’s behind the gap and how to...

Whether you want the highest interest rate or no service fees, these savings accounts will meet your needs.

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

Hello, Can someone please explain to me what happens when my registered GIC RRSP matures relating to my taxes in Alberta, Canada? I have two options, to either reinvest my GIC RRSP on the same term (was 5yrs in 2019 so would be another 5yrs in 2024) or have my GIC RRSP paid out into a specified account. If I have the funds paid out so that I can reinvest a registered GIC RRSP on a different term, since 1yr terms are offering the best rate currently, will I be paying personal income tax if I have the full amount paid out and then I immediately reinvest? Also, if I have $15k paid out, how does this affect my current RRSP contribution limit? I’d like to make the most of the higher interest rates before they start dropping if possible but don’t want to pay personal income tax. Thank you in advance!