Making sense of the markets this week: April 23, 2023

What’s Dale’s take on the economy? Big U.S. bank earnings rock. Apple continues with global domination, and the bitcoin showdown.

Advertisement

What’s Dale’s take on the economy? Big U.S. bank earnings rock. Apple continues with global domination, and the bitcoin showdown.

This week, Cut the Crap Investing founder Dale Roberts shares financial headlines and offers context for Canadian investors.

Regular “Making sense” columnist Kyle Prevost is off for the next couple of weeks. I’m more than happy to sit in the captain’s chair once again and make sense of the markets.

Let’s kick things off with a look at the inflation fight and the state of the economy.

I wrote the final column of 2022 for “Making sense of the markets.” That post included a look back at the year, and it offered a look forward (yes, guesses) about what 2023 might bring.

As my December column showed, there were many investable trends that were easy to identify, and they played out as expected. As I had offered, energy stocks and commodities ruled in an inflationary environment. As outlined on my Cut The Crap Investing blog, I moved to an energy dividend approach, and I’m glad I did. I replaced the price risk with dividend health risk. The iShares S&P/TSX Capped Energy Index ETF (XEG/TSX) is representative of the oil and gas sector, and its dividends doubled in 2022. So far, 2023 continues to gush with dividends and a stream of special dividends. Even so, energy stock prices have been in decline.

Value and defensive stocks also outperformed on the equity front.

From my blog:

“While no one knows the future, and this is not advice, I recently wrote about what worked in 2022 and how it might continue in 2023. Although, now I’d throw bonds into the mix of assets that might do ‘OK’ in 2023.”

Perhaps the “OK” framing for bond performance was prudent. Nothing to get too excited about, but as the bond market adjusts to the Bank of Canada rate hike hiatus, bond prices have been edging up.

If I were to sum up my take on the economic environment, I would use the words “moving in slow motion.” Kyle and I have both mentioned there is a lag effect in play with respect to rate hikes. It can take 12 to 18 months before rate hikes move through the economy to suppress growth and in turn (hopefully) bring down inflation. In one of my blog posts, I summed it up with:

“The pending recession might turn out to be the most advertised and expected recession in history. It might be so expected that it doesn’t happen. Or perhaps the economic shifts are now happening in slow motion. We appear to be in a Goldilocks scenario with falling inflation and a consumer that refuses to cooperate with the recession narrative. Is a soft landing possible, or are we just delaying the inevitable?”

Things are especially slow with this rate hike effort, thanks to a very healthy employment situation in Canada and the U.S. Workers are often hard to find. And employers don’t want to fire workers in fear that it will be very difficult to refill those positions.

When Canadians have jobs, they spend. When they spend, they support the economy.

But make no mistake, there are many signs of economic weakness. I have a Google Doc entitled “Recession Signals,” and it is a robust file.

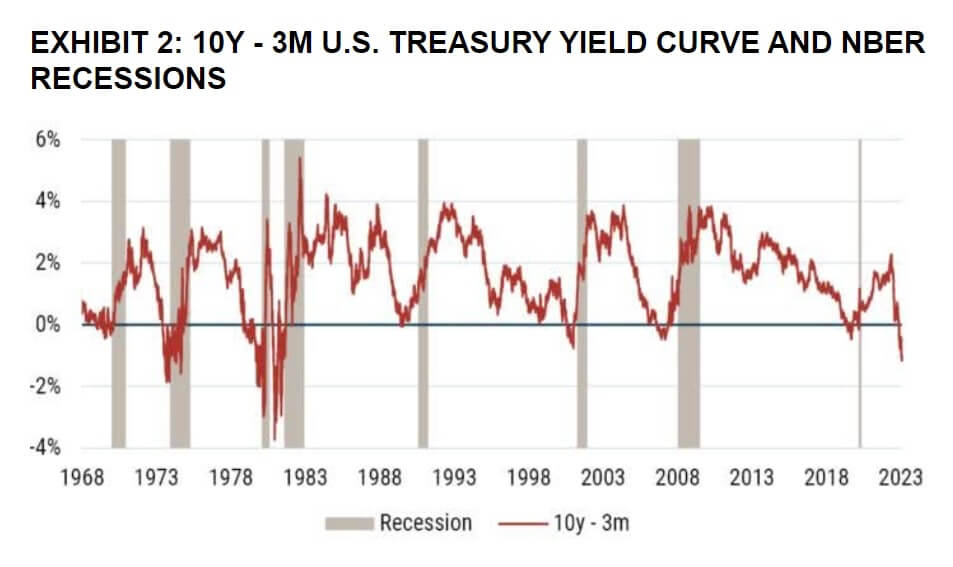

While no one knows the future, the bond market has a very good record in predicting recessions. In fact, the inverted yield curve has predicted seven of the last seven recessions. That’s a lot better than economists, who have predicted 19 of the last seven recessions. 🙂

In the above chart, the yield curve is inverted when the line moves below zero.

Here’s an update on that level of inversion.

On March 8, the spread between the 10-year and 2-year Treasury yields hit -1.07%, the most inverted yield curve since September 1981.

— Charlie Bilello (@charliebilello) March 19, 2023

7 trading days later the spread narrowed to -0.42%, a 65 bps increase. This was the biggest 7-day steepening we’ve seen since the 2001 recession. pic.twitter.com/yd3wATWpGE

If we don’t get some form of recession, it will be an outlier. That said, the expert and economist consensus appears to be that we will experience a soft recession. And that recession might arrive in the second half of 2023, or early 2024.

We will follow the U.S. into recession if they go first. Canada always does.

🇺🇸 Recession

— ISABELNET (@ISABELNET_SA) April 19, 2023

Will the next US recession start in 2H 2023?

👉 https://t.co/m11iBkSWhc

h/t @jpmorgan #markets #recession #recessions#risks #assetallocation #economics #investing pic.twitter.com/zmMUcO32Wk

If we do enter the most advertised recession in history, it’s possible that stocks won’t take too much of a beating. After all, investors should not be caught off guard.

And certainly, an economic soft landing is a possibility.

The good news in Canada is that inflation is coming down, though it will likely be very sticky in many areas, such as food.

Canadians aren’t ready for this, but need to be.

— The Food Professor (@FoodProfessor) April 18, 2023

Pressures within the food industry are real. This is our forecast for food prices, wholesale, before goods are sold to grocers in Canada, until 2025. pic.twitter.com/Xj1Q3t2Yb8

There is the risk of energy resurfacing as an inflationary force. Wages are also increasing, and that can create wage-push inflation.

It’s my guess (one I share with many) that we are not going back to the 2% inflation target. We might enter a period where 3% to 4% inflation is the norm and, well, historically that is closer to the longer-term trend. More good news is that stocks typically perform well with that level of inflation.

Entering 2023, I suggested that defensive stocks might outperform, as they did in 2022. However, growth stocks have led the way so far this year.

If that recession does finally arrive, it’s likely that consumer staples, health care and utilities will be good places to hide. Bonds should also perform well if inflation is under control.

There is much uncertainty, thanks to the unpredictability of inflation. Retirees should be prepared for anything and everything. Those in the accumulation stage might ignore all of my interesting economic observations and continue to invest on a regular schedule.

Embrace those lower prices while knowing and understanding your tolerance for volatility.

We recently had the U.S. regional banking “crisis.” From that MoneySense column:

“The big news of the week was, of course, that the 12th-biggest bank in the U.S.A.—Silicon Valley Bank (SVB)—essentially went bankrupt.”

It was the second-biggest bank failure in U.S. history. It was then followed up by the failure of Signature Bank, the third-biggest bank failure in history. But no worries: The U.S. Fed was there to guarantee all deposits, as the majority of deposits were not covered by deposit insurance. The Fed and government agencies announced that all deposits in the U.S. were safe.

They would do whatever it takes. It is bailout nation, of course. 😉

Crisis averted. Maybe.

Starting last Friday, earnings season kicked off with a few of the big banks reporting. Their numbers were very strong. Here’s a taste of the bank reports, all in U.S. dollars:

These strong earning reports gave the markets a short-term boost, and then the U.S. regional banks began to report earnings. There were signs of weakness in the reports.

The regional banking crisis might turn into a slow burn. There is USD$1.5 trillion in commercial real estate loans to be reset at much higher rates over the next two years. In the commercial real estate space, many will hand in their keys. There will be no loans.

Many experts suggest we face the threat of greater economic contagion. Others suggest the economic stress can be absorbed, but it will contribute to economic weakness. This is one of the big events to keep an eye on.

BofA: Strong start to earnings seasons but credit contraction starting to bite pic.twitter.com/DwWJq5IxuV

— Scott Barlow (@SBarlow_ROB) April 18, 2023

Tesla (TSLA:NASDAQ) has always been a hot topic in this column. The leading EV company reported earnings that showed a sizable margin compression and growing inventory. Tesla has cut prices a few times in the last several months. The company’s gross margin came in at 19% for the quarter, down by a massive 1,000 basis points from 29% one year earlier. Earnings declined.

The stock was down almost 10% on Wednesday, April 20. Tesla added to losses early on Thursday.

Back in 2020, we showed how the value of Tesla could be used to purchase several of the major automakers. You’ll see a stunning chart in that post. The value of Tesla became even more outrageous in the months following that post. The stock price more than doubled into late 2022.

All said, Tesla’s margins are very good for the auto space. We don’t know if the legacy automakers will become profitable producing electric vehicles.

My take is that we are in the first inning of the EV revolution, and that the dance floor is wide open. I’m happy to invest in the EV and battery space by way of the Amplify BATT ETF and the VanEck “green” metals ETF (GMET).

Tesla set a quarterly record by delivering more than 422,000 vehicles in the first quarter of 2023, but it took those price cuts to achieve that sales volume. Tesla delivered revenues of $24.32 billion and non-GAAP earnings per share of $1.19 (all figures for Tesla are in U.S. currency). The weakest part of the report was the cash flow picture. Tesla generated just $441 million of free cash flow, well below the more than $2.6 billion that analysts were expecting. Inventory rose by more than $1.5 billion in the quarter as production again exceeded deliveries.

All said, Tesla is difficult to price, as it trades on hope, not fundamentals.

In Canada, Metro (MRU/TSX) delivered very good results, as has been the trend for Canadian grocers. The following is in Canadian dollars.

Apple (AAPL/NASDAQ) is one of my favourite companies and perhaps my favourite stock holding. It is one of my three U.S. stock picks from 2014. From the time I picked up Apple, it has beaten the S&P 500 by more than 16% annually.

My other picks include BlackRock (BLK/NYSE) and Berkshire Hathaway (BRK.B/NYSE) as a defensive (bring on that recession pick).

Apple recently made another fintech push with a partnership with Goldman Sachs to deliver a high-interest savings account offering in the U.S. From that news article:

“Apple joined the competition for bank deposits on Monday with the launch of a high-yield savings account that pays an annual percentage yield of 4.15%. The high-yield savings accounts, available in conjunction with Apple’s credit card, are one of the tech company’s latest steps into the financial-services space, which also include an option to allow customers to ‘buy now, pay later’ on certain of its hardware products.”

Apple is also moving some production to India. CEO Tim Cook travelled to India to open the first Apple store in a country that many economists feel could be an economic powerhouse in the future. It’s expected that India will pass China some time this summer to become the world’s most populous country.

Apple can move into new offerings where it can deliver great products within the sensible bounds of the brand. But it can stretch the product offering beyond our expectations. Think back to Apple moving into digital music, and then smartphones, essentially creating categories.

It’s a great company, but a very expensive stock IMHO. The stock’s forward price-to-earnings (P/E) ratio—calculated by dividing the stock price by projected earnings per share—is high, at 27.17 (as of April 21). I’m glad that I already own it.

As you may know, I wrote the go-to piece 😉 on bitcoin as an investment, back in January 2021. Gold makes a balanced portfolio better. And for me and many others, bitcoin is modern or digital gold. From that column:

“Arthur Salzer of Northland Wealth Management offers: ‘Monetary value usually arises from objects that are scarce, durable and relatively easy to divide. Since the dawn of civilization, societies have used rare seashells, wampum, glass beads, and stones as money or a form of record keeping. Gold is an ideal example since it can be made into jewelry, coins and bars, but bitcoin is unique in today’s digital world since it is scarce, durable, has strong privacy characteristics.’”

After the FTX scandal, I suggested that the increased scrutiny and regulation in the crypto space would be beneficial. Folks would also learn the difference between bitcoin and “shitcoin.”

Bitcoin is one of the best-performing assets from the time of that post, and in 2023 it’s up over 70%. Just sayin’.

Bitcoin as an investment is not a risk everyone wants to take on. But I’m happy to own some real gold (flirting with all-time highs) and modern gold. Balance sheets in the developed world are a joke, and they continue to deteriorate.

Kyle Prevost is a prolific bitcoin hater. 😉 He will be back in this space in two weeks.

Dale Roberts is a proponent of low-fee investing, and he blogs at cutthecrapinvesting.com. Find him on Twitter @67Dodge for market updates and commentary, every day.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

Tax season can push Canadians deeper into debt as many rely on refunds. Here’s why it’s happening, and how...

The first quarter finally broke the pattern of steadily rising markets, but energy stocks soared.

Robert has been taking RRIF withdrawals beyond the minimum required amount to gift to his kids and to reinvest...

Geopolitics, rising oil prices and ETF inflows are shaping Bitcoin’s outlook. Is now the right time for Canadian investors...

Wealthsimple's direct indexing brings a tax-saving investing strategy to a wider group of investors, but the number likely to...

A University of Calgary study found that over one-third of senior homeowners worry about affording basic home maintenance, suggesting...

Whether you want the highest interest rate or no service fees, these savings accounts will meet your needs.

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...