Making sense of the markets this week: April 5, 2021

BMO sounds the alarm on Canada's housing market, while National Bank begs to differ; how it got so expensive to rent a car; and will bitcoin regulation really happen?

Advertisement

BMO sounds the alarm on Canada's housing market, while National Bank begs to differ; how it got so expensive to rent a car; and will bitcoin regulation really happen?

“One of Canada’s biggest banks is calling on policymakers to act immediately as a ‘fire department’ for blazing housing markets.

“Bank of Montreal (BMO) senior economists laid out a series of recommendations in a new report titled Canadian Housing Fire needs a response and rated how effective a number of those measures would be.”

Some areas across the country are experiencing year-over-year price gains in the area of 30% to 35%. There is a low inventory and a shift in demand thanks to the pandemic. Low borrowing costs are adding fuel to the fire. BMO said the most acute problem is market psychology, even as supply-side issues persist. “The action needed today is one that immediately breaks market psychology and the belief that prices will only rise further. That would dampen the speculation and fear-of-missing-out that those expectations are creating,” BMO’s senior economist Robert Kavcic and economic forecaster Benjamin Reitzes noted. And on the subject of Canada’s real estate bubble, this Yahoo! Finance video is a must-watch. Industry experts John Pasalis, housing analyst and President at Realosophy Realty, and Steve Saretsky, housing analyst and realtor at Oakwyn Realty, say investor psychology is driving the frenzy. It’s FOMO—the fear of missing out. “They need to buy a house now or they’re never going to be able to afford one,” offered Bains, who studies investor psychology as it pertains to real estate. Both experts say there is certainly a housing bubble of epic proportions. And home buyers are being cheered on by our Central Bank and politicians, with the promise that low rates and borrowing costs are here to stay until 2023. In their report, BMO offered.…“Interest rates and the Bank of Canada’s commitment to keep them low for years are arguably the key drivers behind the meteoric surge in home sales and prices across large swathes of the country. A move here would have an immediate, clear and notable impact to cool housing.”

“‘The success of the economic recovery will depend on Canadian consumers in the coming months. There are several reasons to be optimistic,’ the [National Bank] report said. To start, households enjoyed a record increase in both disposable income and the savings rate in 2020.

“‘Excess savings—which we currently peg at 8% of GDP—are currently hibernating in deposit accounts and are ready to be tapped by households once free of COVID-related restrictions,’ the report said.

“‘At the same time, household finances have also been given a boost by rising real estate prices and strong financial asset returns—producing the “strongest positive wealth effect since 2009,’ the report noted.”

However, on the subject of borrowing and interest rates, we might want to take that opinion with a grain of salt. Rising rates might quickly or eventually become a concern for many recent first-time buyers who’ve taken out massive mortgages. That is the elephant in the real estate room. Here’s a tweet that highlights the recent real estate activity in Canada:Selected Canadian Real Estate and Housing Starts for February #canada #realestateagent #cdnpoli #novascotia #ontario #mls #viewpoint pic.twitter.com/GwRLUeXfQm

— Burnsco (@garquake) April 1, 2021

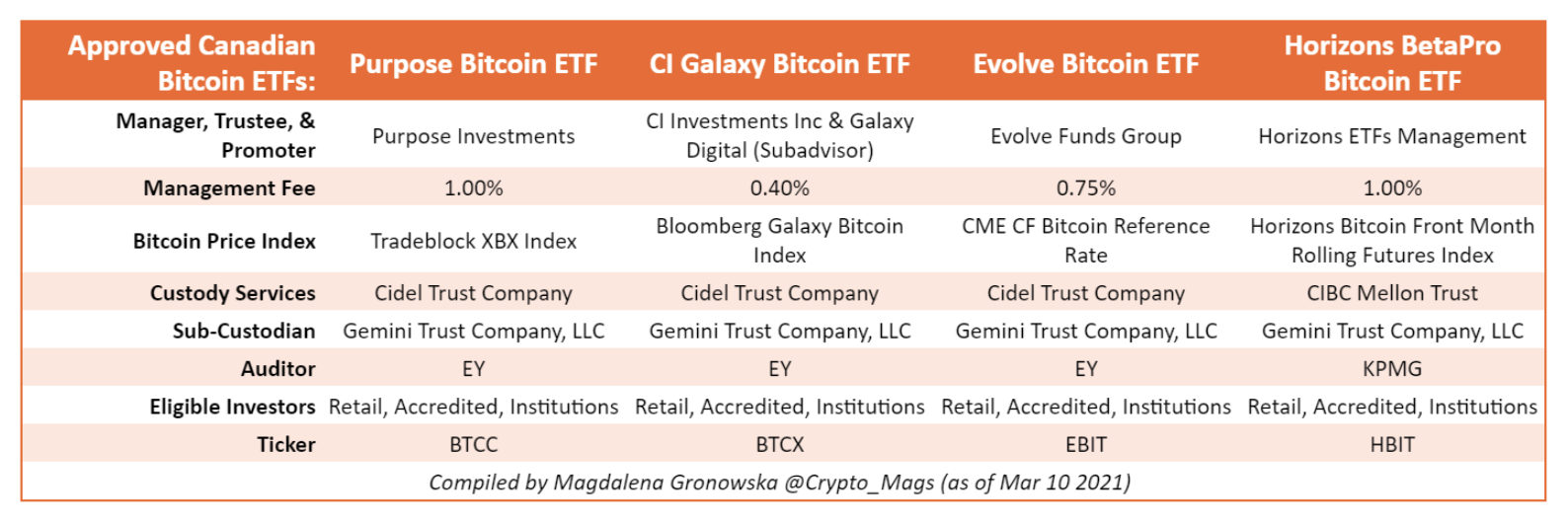

This is the #Bitcoin #ETF & Fund/Trust comparison you were looking for Raising hands

— MAGS 🔑⛏️🚒 (@Crypto_Mags) March 11, 2021

Canadian ETFs (Approved), publicly traded on TSX:

🔸 $BTCC, @PurposeInvest, holds $BTC

🔸 $BTCX, @CIGlobalAsset, BTC

🔸 $EBIT, @EvolveETFs, BTC

🔸 $HBIT, @HorizonsETFs, BTC Futures

1/ pic.twitter.com/0yTNXSLNFw

“The U.S. would hold most of the world’s gold, guaranteeing other nations could convert their gold reserves at a fixed $35 per ounce rate. Essentially, this tied other countries to the U.S. dollar.

“Bretton Woods ‘worked’ for almost 20 years but with side effects, not unlike today’s euro problems.… Starting in the mid-1960s, various European countries began demanding payment for their dollars in gold. They wanted the U.S. to balance its budget, which had gone wildly into deficit because of the Vietnam War.”

These days we are in the midst of a different kind of war (with COVID) and, of course, we have the deficit spending and alarming debt levels to go along for the ride. The first modern day pandemic and war required a historic response by governments and central banks. That Mauldin Economics post will help shape your perspective on gold, debt, and fiat currency. Given that, we might appreciate the use of gold or bitcoin (what I like to call “new gold”) in a portfolio. The unfortunate trend of the separation between haves and have-nots is also on display in that post. These are clear, consistent and ongoing trends that are perhaps even being accelerated. Machines and modernization of the workforce have been the wedge between the rich and the working classes. Look to the post for some shocking charts.“One reason for that is the productivity we talked about earlier. It really shows up as the capital equipment and technology which is bought to reduce the cost of labour (robots, bank ATMs, computers, automated production lines and many others). It all reduces the share of income going to labour while raising income for machine-owning capitalists.”

The ability (or not) to invest in stock markets exacerbates the wealth disparity. We own the companies that own and develop the machines and technologies. Investing is a hedge against the future. Dale Roberts is a proponent of low-fee investing who blogs at cutthecrapinvesting.com. Find him on Twitter @67Dodge.Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Q4 shows mixed results across sectors: Canadian Natural and Pet Valu post gains, while George Weston and Canada Packers...

Bitcoin extends losses, down 47% since October 2025. When will the crypto bear market reverse, and what does the...

Crypto profits aren’t always tax-free. Here’s how the CRA taxes cryptocurrency transactions, mining and staking, and overseas gains.

Low trading volume does not necessarily mean low liquidity. Here’s what actually determines how easy it is to buy...

Vanguard’s VRIF ETF is tilting toward bonds to provide retirees stable income, balancing caution with a 4% annual payout...

Canada’s banking sector sees higher Q1 profits and strong financial performance in the latest earnings reports.

From big profit jumps at Enbridge and Cenovus to strong holiday sales at Canadian Tire, see how major Canadian...

In maintaining your planned allocations in a portfolio of ETFs, consistency matters more than precision.