By Dale Roberts on February 19, 2021 Estimated reading time: 10 minutes

Making sense of the markets this week: February 22, 2021

By Dale Roberts on February 19, 2021 Estimated reading time: 10 minutes

Ways to take advantage of the commodities supercycle; bonds are having a rough year while global markets play catch-up; and Shopify's earnings rouse the markets, but is it as great a stock right now as it is a company?

This article is 3 years old. Some details may be outdated.

Advertisement

Photo by Roberto Cortese on Unsplash

Each week, Cut the Crap Investing founder Dale Roberts shares financial headlines and offers context for Canadian investors.

Boosting the portfolio for the commodities EV supercycle

A commodities supercycle occurs when the demand for base metals and other commodities increases significantly, as those “things” are needed for the production of the goods that we consume. And, right now, the chatter around a potential commodities supercycle is accelerating on financial sites and financial news networks. This Reuters article from early January set the stage. Supercycles can arise in a period of economic rebirth, such as what we might see coming out of the pandemic. From that Reuters piece, citing the opinion of investment bank Goldman Sachs…“A supercycle can be defined as “decades-long, above-trend movements in a wide range of base material prices” deriving from a structural change in demand.” Goldman started making the call for a supercycle in October of 2020. This Yahoo Finance post published Feb. 10 says commodities may have just begun a new supercycle. In that article, you’ll find a chart showing previous supercycles, where we can see the slight price blip (for the commodities index) for the recent price acceleration. From that Yahoo Finance post…

“A long-term boom across the commodities complex appears likely with Wall Street betting on a strong economic recovery from the pandemic and hedging against inflation, JPMorgan analysts led by Marko Kolanovic said in a report on Wednesday. Prices may also jump as an ‘unintended consequence’ of the fight against climate change, which threatens to constrain oil supplies while boosting demand for metals needed to build renewable energy infrastructure, batteries and electric vehicles, the bank said.”

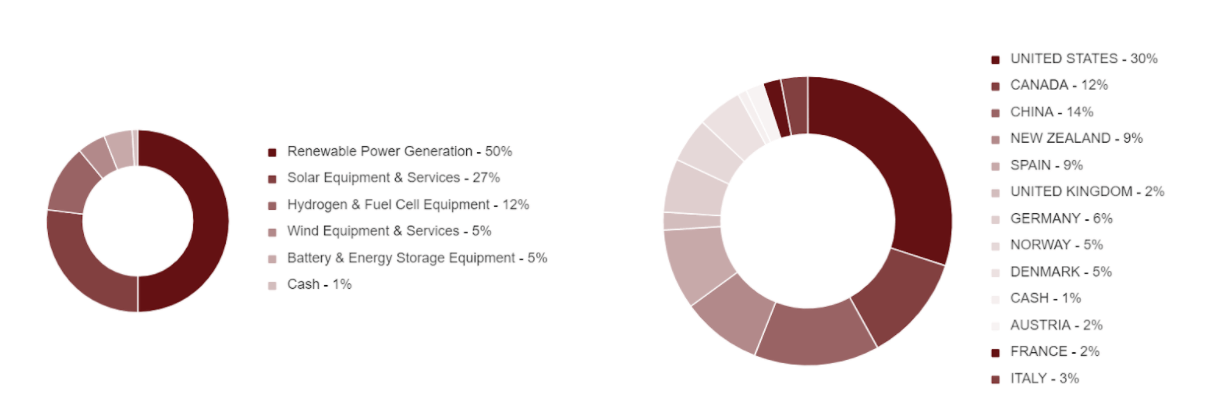

This is not the first time I’ve mentioned commodities in this space. I really like the sub-supercycle theme of investing in the supply chain for the EV (electric vehicles) market. This is an obvious trend. Governments around the world have declared that they are going green as soon as possible—that is, the goal to virtually eliminate human CO2 creation by 2050, in an effort to fight global warming. EVs will play a major role. And the trend is supported by global policy and by subsidies within many countries. You can’t fight city hall and perhaps you can’t fight The Paris Agreement. Many companies are being very aggressive with this green shift. For example, the Ford Motor Company recently announced that their entire European passenger sales will be all electric and hybrid by 2030. How do we go along for the ride? You might put a charge in your portfolio with the BATT ETF. I’ve been researching this theme for a few months. The BATT ETF from Amplify just might plug into your portfolio quite nicely. For me, it will tick a few boxes: the EV trend, inflation and a hedge against our traditional oil and gas holdings such as pipelines. It offers global diversification as well. BATT plays everything from the metals required to EV manufacturer Tesla, and the many companies connected along the entire EV production assembly line. The ETF is essentially flat from its inception in June of 2018. But if you click on that BATT link, you’ll see that, more recently, the ETF has gone on quite the run: The price has more than tripled (up 300%) from mid-February of 2020. Does that mean the EV opportunity left without you? We are still in the early stages. That may not mean the ETF did not quickly get a bit ahead of itself. But as we’ve seen with great investment themes such as EV and Tesla, they can go on a very spirited and continued run. And, similar to the way you might decide to invest in bitcoin, you might initiate a position and dollar-cost-average along the way. We can’t wait around for a correction. If we get lower prices or see a major correction, you will be able to reinvest at lower prices, driving down your average cost. If the price only continues to go up, great. In the name of portfolio irony, I will have my generous Enbridge and TC Energy dividends feeding that BATT ETF. TC Energy just announced a 7.5% dividend increase. More dollars to invest in BATT!Keep in mind that BATT is a U.S.-listed, U.S.-dollar ETF. It can be held in registered accounts, but is best held in a U.S.-dollar account, when possible. When you can hold U.S. ETFs in Canadian registered accounts, you will face currency conversion charges when you buy and sell. I was more than excited to see a truly green (and Canadian-dollar) ETF introduced by Harvest Portfolios Group—you might also investigate the Harvest Clean Energy ETF (HCLN).That could be a wonderful complement to BATT, rounding out the green energy space and trend. Personally, I’d be happy with a 5% portfolio weighting for total BATT, plus HCLN. I like to include some undeniable trends in my wife’s and my portfolios, building around our core. Here’s the breakdown for HCLN. In the EV lane, you might also look to CARS from Evolve ETFs, a Canadian ETF provider. Have a read of this MoneySense post on how to trade ETFs: set a limit price for purchase and pay attention to the bid/ask spreads. Happy portfolio greenification.

Bonds off to their worst start to a year since 2013

It is “risk on” in 2021. That phrase describes the rush (by investors) to more risky assets, such as stocks. “Risk off” would include the assets that manage the stock market risk, such as bonds. For a primer, you might have a read of this post on my site; here, I describe stocks as those overly emotional and unpredictable toddlers, while bonds are the adult in the room. They keep an eye on those stocks for you. Regardless of this wisdom, Lisa Abramowicz, on Twitter, offered that bonds are more than unpopular these days. Source: TwitterBut it’s no time to run away from bonds. Remember why we own them. They are risk managers for stocks. They are a key portfolio asset that should/could perform in a deflationary environment as well. When stocks crater—and they will—I believe quality bonds (especially those with longer maturity) will be there to do their thing. Many portfolio managers will suggest an allotment to U.S. treasuries. From my research, they punch above their weight when it comes to managing stock market risk. And, these days, as some bond yields are rising (bond prices falling), portfolio rebalancing would suggest that we add to our bond positions. Again, that rebalancing would also include moving monies to other risk managers as well, if stock prices continue to increase dramatically. The all-weather portfolio can include some gold, bitcoin and commodities. Just rebalance as you would with your bonds. The all-weather portfolio can provide better returns and better risk-adjusted returns compared to a traditional balanced portfolio that is composed of stocks and bonds. I’ll be back in the future with a post looking at that all-weather portfolio. If you feel your portfolio is overexposed to longer-dated bonds and rising interest rates, you might move to shorter-duration bonds or ETFs; you can look at floating-rate bond ETFs and short- to mid-term bond ladder ETFs. You might even consider a GIC ladder for a segment of your portfolio. All said, if we rebalance to bonds today and along the path of a rising-rate environment, we will be picking up some greater yields and lower prices. We like when our stocks go on sale—so why not embrace our bonds when they go on sale?

Global shares play catch-up

At the beginning of this week, global shares hit a fresh peak with advances that are 11 days running. While many stock markets have lagged the tech-heavy U.S. market, developed markets such as those for Europe and Britain and Japan have been posting very solid and consistent gains. In fact, the Nikkei (Japan’s stock market) is back above 30,000 for the first time in three decades. Wow, talk about lost decades for stocks. From that link…

“Japan’s Nikkei share average rose above the 30,000 level for the first time in more than 30 years on Monday, as it regained the ground lost during decades of economic stagnation.”

The developed markets stock index (developed nations excluding U.S.) has lagged, but it’s playing catch-up, if in modest fashion. The developed markets EAFE (Europe, Australasia, Far East) has outperformed U.S. markets from Nov. 1, 2020, after positive vaccine approvals gave another boost to the stock market rally that is still in progress. The stock market recovery based on global vaccination and global economic recovery hopes is now a global affair. One event to keep an eye on is vaccine nationalism. How will the markets react to countries and regions that lag behind in the struggle to vaccinate their populations? I’ll keep score, in this space.

Canadian tech darling Shopify offers an incredible quarter

Shopify reported earnings this week: Canada’s most valuable publicly traded company almost doubled revenues in the quarter, year-over-year. The company also beat earnings estimates. Here’s the earnings overview, courtesy of Seeking Alpha:

Shopify (NYSE:SHOP): Q4 Non-GAAP EPS of $1.58 beats by $0.37; GAAP EPS of $0.99 beats by $0.35.

Revenue of $977.74M (+93.6% Y/Y) beats by $64.42M.

GMV grew 99% Y/Y to $41.1B; Gross Payments Volume grew to $19.1B, which accounted for 46% of GMV processed in the quarter.

CFO comment: “Shopify was prepared to ship the features that our merchants needed during the pandemic because we had invested for several years in a future that arrived early with the acceleration of online commerce. We’re amplifying our efforts in 2021, as we focus on executing on a portfolio of initiatives that will fuel further growth for our merchants and for Shopify.”

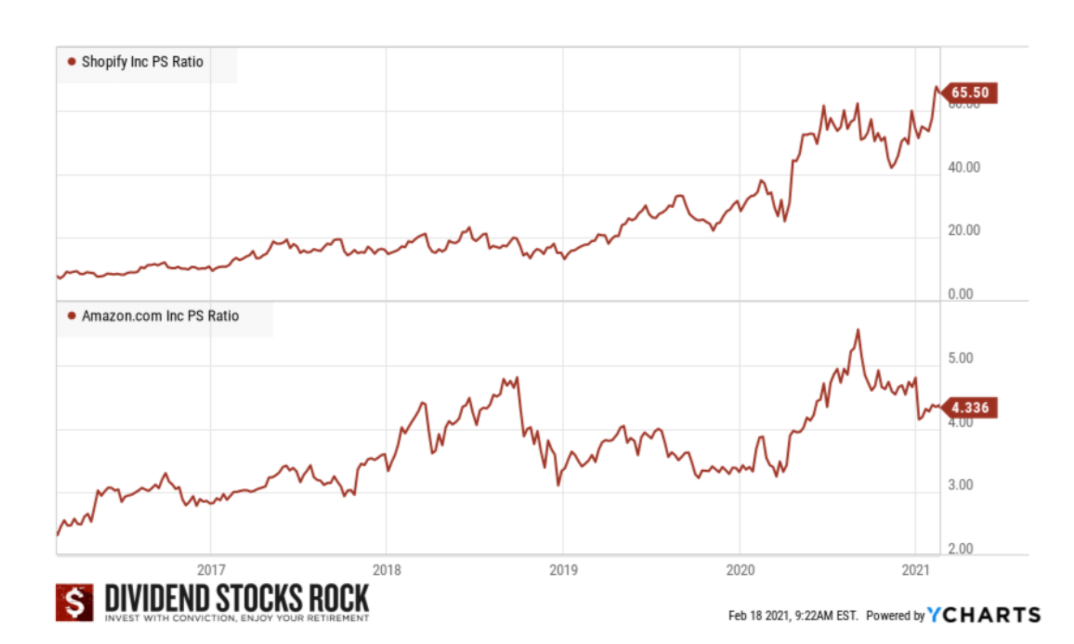

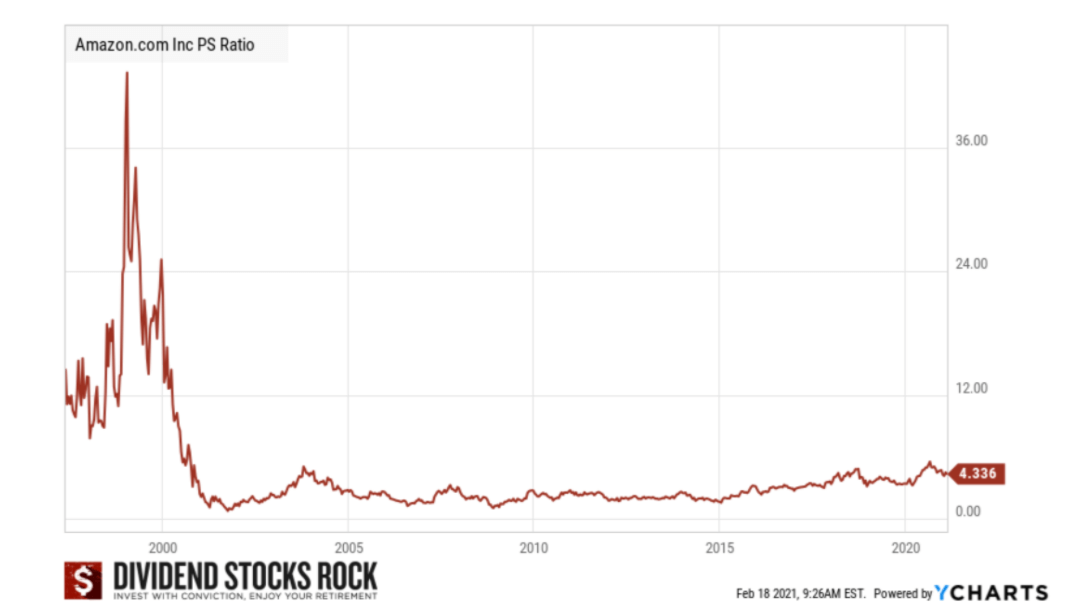

There is no debate that Shopify is a great company, but many wonder if it is a great stock. It is very expensive. The PE ratio (price-to-earnings) is a dizzying 843 according to YCharts. The price-to-sales ratio is above 65. Here’s a great comparison chart courtesy of Mike at Dividend Stocks Rock:Is Shopify another Amazon? Could it one day grow into those big PE and PS ratio boots? Amazon stock was long criticized for being too expensive. Thanks to continued monster growth numbers over several years, Amazon grew into its valuation. And from the chart above we can see that in recent years Shopify has been much more expensive compared to Amazon based on price-to-sales. Even in its more nascent years, Amazon was never as expensive as Shopify. It only briefly punched above 36. That said, Mathieu Litalien, who writes at Stocktrades.ca, reminds me that the market today is assigning or allowing for much more liberal (higher) price-to-sales ratios in 2020 and 2021 compared to 10 and 15 years ago. Stepping back, I’d suggest that expensive is expensive. In the end it comes back to earnings and revenue growth. We have some Shopify exposure (in my wife’s account) by way of the TSX 60 XIU ETF. I am not eager to top this one up at today’s levels. Many will suggest that Shopify is a great company, but perhaps it is not a great stock at today’s levels. Into Thursday, Shopify stock was down over 5% from the time of the earnings release. Shopify CEO Tobias Lutke acknowledged that, moving forward, it would be a challenge to match the growth rate of 2020. Dale Roberts is a proponent of low-fee investing who blogs at cutthecrapinvesting.com. Find him on Twitter @67Dodge.

Dale Roberts is a former investment advisor and proponent of low-fee investing. He created the Cut The Crap Investing blog in 2018. Find him on Twitter for market updates and commentary, every day.