By Dale Roberts on July 23, 2021 Estimated reading time: 10 minutes

Making sense of the markets this week: July 26, 2021

By Dale Roberts on July 23, 2021 Estimated reading time: 10 minutes

Evidence that buying the dip isn't the brag investors might think; more dispatches from earnings season; what you need to know about stagflation; and where you can now buy a fraction of a stock share.

This article is 4 years old. Some details may be outdated.

Advertisement

Photo by Ravi Patel on Unsplash

Each week, Cut the Crap Investing founder Dale Roberts shares financial headlines and offers context for Canadian investors.

Earnings season, part II: both sides of the border

In last week’s column, we kicked off earnings season and the projections for what is setting up to be a robust reporting period. It is likely to be the earnings growth peak in both the U.S. and Canada. A roundup report on Seeking Alpha offered…

“The rally goes on…. A three-day winning streak on Wall Street—that followed a sharp selloff on Monday—is showing no signs of slowing down as futures continued to climb in overnight trading.

“‘The earnings results have continued to be strong and guidance is showing that the Delta variant isn’t impacting the recovery, so far at least,’ said Esty Dwek, head of global market strategy at Natixis Investment Managers. ‘That is giving confidence to the market that the recovery can continue’.”

Canadian stocks are also joining the rally. Here’s a snapshot of selected earnings: CN Rail beat projections on the earnings front, but trailed on revenue. Railways are very economically sensitive bellwether industrials, as they move the goods across the country and across North America. Freight revenues (C$3,452 million), which contributed 95.9% to the top line, increased 14% year over year as economic activities picked up. Canadian National still anticipates earnings per share to grow in double digits during 2021 from adjusted earnings of C$5.31 in 2020. Rogers Communications earnings were just short of expectations, while they beat on revenue, reporting C$3.58B. That’s up 13.3% year over year and beat by C$40M. Rogers management offered… “This quarter, we generated cash flow from operating activities of C$1,016 million, down 29%, and free cash flow of C$302 million, down 35%, as a result of increases in cash income taxes and capital expenditures.”Air Canada continues to face incredible challenges, but reported revenues that surpassed expectations. That said, they are still largely grounded and losing money at a good clip. The airline reported operating revenues of $837 million, an increase of $310 million or 59% from the second quarter of 2020, and an operating loss of $1.133 billion compared to $1.555 billion in the second quarter of 2020. Net cash burn of $745 million, or about $8 million per day, on average, is down from the $15 million per day range of the first quarter. They expect that to fall to $3 to $5 million in the third quarter. Travel restrictions are being removed; will Canadians take to the skies? That is yet to be seen. In a recent post we reported on the potential of close-quarters hesitancy. But the stock has not been grounded. The stock is up over 59% over the last year. That might be rich, for a company that is burning cash and not fuel. We’ll keep an eye on the Canadian traveller and Air Canada.

South of the border…

U.S.-index and portfolio staple Johnson & Johnson had a robust quarter, beating on earnings and revenue: Q2 Non-GAAP EPS of $2.48 beats by $0.19; GAAP EPS of $2.35 beats by $0.31. Revenue of $23.31B (+27.1% year over year) beats by $770M. They also increased guidance moving forward. That can also affect stock prices. JNJ is up in a healthy fashion after their earnings release. Source: Seeking AlphaI’m happy to hold JNJ in our market-beating U.S. stock portfolio. Coca-Cola earnings and revenues bubbled in the second quarter: Q2 Non-GAAP EPS of $0.68 beats by $0.12; GAAP EPS of $0.61 beats by $0.05. Revenue of $10.1B was up an incredible 42% year over year, and beats by $800M. They also adjusted guidance more favourably, and like Pepsi that I own, the stock saw a nice pop after earnings. Source: Seeking AlphaDiversified telco Verizon reported very strong numbers: Q2 Non-GAAP EPS of $1.37 beats by $0.07; GAAP EPS of $1.40 beats by $0.11. Revenue of $33.8B (+11.2% year over year) beats by $1.07B. Wireless Retail postpaid net adds of 528K vs. a consensus of 360K.Chip maker Texas Instruments beat on earnings and revenue, but the market did not like its forward guidance. That took the stock down: Q2 Non-GAAP EPS of $1.99 beats by $0.14; GAAP EPS of $2.05 beats by $0.22. Revenue of $4.58B (+41.4% year over year) beats by $220M.Alaska Air reported its first profit since 2019: Q2 Non-GAAP EPS of -$0.30 beats by $0.15; GAAP EPS of $3.15 beats by $2.90. Revenue of $1.53B (+263.4% year over year) beats by $10M. And American Airlines surprised on a few metrics: Q2 Non-GAAP EPS of -$1.69 beats by $0.03; GAAP EPS of $0.03 beats by $0.92. Revenue of $7.45B (+359.9% year over year) misses by $30M. Load factor of 77% vs. consensus of 72.1%. Q3 capacity to be down approximately 15% to 20% vs. 3Q19, total revenue to be down approximately 20% vs. 3Q19. The earnings watch continues. Things should heat up more next week on Canadian side of the border.

Understanding stagflation: is it the biggest threat?

Stagflation is a period where we have inflation but no economic growth. That is not a good combination. Our cost of living is increasing and many companies will move through difficult times; with the economy stagnant or shrinking, more and more workers join unemployment lines. Stagnation hit with force in the 1970s and into the early ’80s. It ate investors alive. You can head to the Moneychimp calculator to play around with U.S. stock returns from the period from 1966 to 1981. Don’t forget to hit that inflation button. From my own research using Canadian stock market data supplied by BlackRock and using the inflation calculator on the Bank of Canada site, our markets also came up short for most of the period. Canadian stocks roared back toward the end of the stagflation era, after most of the damage was done. Real and lasting inflation is arguably the most-discussed investment topic (and fear) of the day. And stagflation is a greater concern. From Vox, here is a wonderful summary of the stagflation of the 70s and how the conditions might apply to today. Can we look to the conditions that caused stagflation in the 70s and make an educated guess as to the possibility of a repeat in 2021 and beyond? Many of today’s investors have not known inflation or stagflation. From that post…

“For those of us not alive then and who have never lived through a period of debilitating inflation, the fears voiced by baby boomer economists like Larry Summers and Olivier Blanchard that massive price increases could be coming might ring hollow. But their worry, which many economists share, reflects a real history. The Great Inflation, which began in the late 1960s and finally ebbed in the early ’80s, was a genuine calamity that worsened living standards for years.

“Understanding the warning that figures like Summers and Blanchard are issuing is important. But equally important is understanding the key differences between what happened in the 1970s and what’s happening today.”

The thrust of that post and thesis is that central bankers can learn from past policies and bank responses to stagflation, and apply that during the current inflation threat. The post also looks at the underlying economic conditions of the 1970s and 2020s. Inflation can be an accumulation or piling on of various and individual price increases such as the oil price spike of the 70’s. Today, many put forth the transitory inflation argument based on the fact that there are small pockets of inflation caused by shortages (supply shocks) and supply chain issues. Issues that might soon be resolved. We’ve talked about those inflation hot spots in the past. From that Vox post, and on the suggested strategy:

“Instead, the federal government should be intervening in specific areas to keep specific types of prices that are rising rapidly from further accelerating.”

Can central banks and politicians stickhandle their way through any inflation or stagflation threat? That remains to be seen, and there are so many different moving parts. No economic period is the same. No stock or bond market correction or rally is the same. The VOX article, while very good, is a guess. Perhaps even a very well-thought-out and educated guess. That said, predictions about the economy are hard to make. At least we’re talking about inflation and its real risks. When we protect our wealth, we don’t guess; we create a portfolio based on a truth—that we don’t know the future. We don’t know what’s in store. Gold and other commodities have worked to protect portfolios during stagflation (see those supply shocks), while stocks were no match for inflation in the U.S. and Canada. To my knowledge, international stock markets were also not the required hedge, though certain types of stocks such as energy and commodity-related, tech and consumer discretionary, might help the cause. You might shade in some inflation-adjusted bonds to your fixed income component. Invest and perhaps hedge accordingly.

Wealthsimple trade is the first to offer trades of fractional shares

The trading app Wealthsimple Trade became the first to allow clients to buy and sell fractional shares. Investors can trade a select list of Canadian- and U.S.-listed stocks in this manner. (Wealthsimple is also Canada’s leading robo-advisor by assets under management.)Buying fraction shares allows you to buy $100 of a stock, even if the share price is $1,000. At a discount brokerage, an investor would have to wait until they have $1,000 of cash in their account to buy that $1,000 stock. Consider that the price of Shopify is now near $2,000. Want to grab a few hundred bucks worth of Shopify? Now it’s no problem. And remember, there are no fees when buying and selling Canadian stocks. Investors will face the currency conversion charges when buying or selling U.S. stocks. Here is the very fractional list of popular companies available for fractional share buying:

Airbnb, Inc.

Amazon.com, Inc.

Apple Inc.

Canadian National Railway Co.

Coinbase Global Inc.

Google LLC

Microsoft Corp.

Netflix Inc.

Nvidia Corp.

Royal Bank of Canada

Shopify

Tesla Inc.

Toronto-Dominion Bank

Wealthsimple plans to expand this list. We’ll keep an eye on it.

Buy the dip?

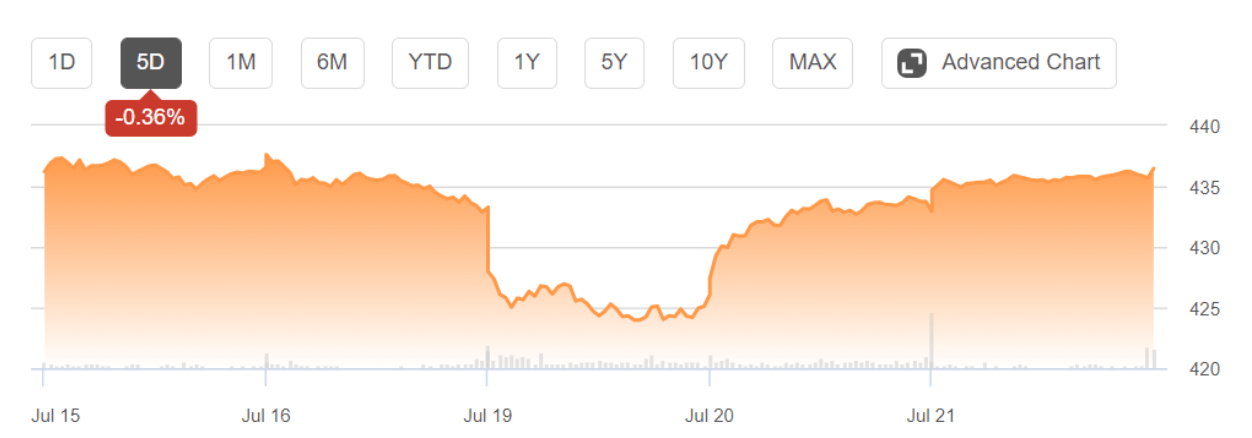

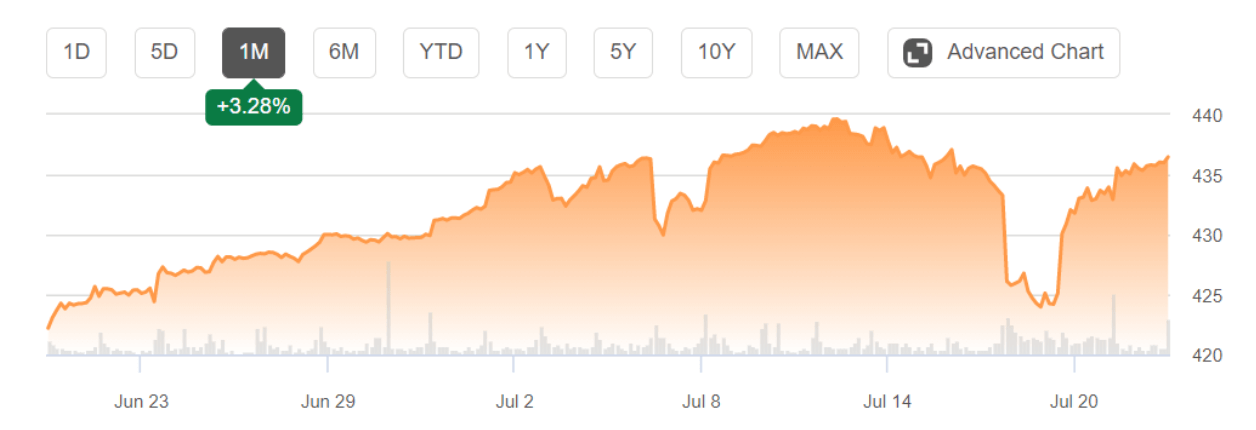

It was the big story of the week. Stocks fell on Monday, July 19, due to concerns over the COVID Delta variant disrupting the grand reopening plans. The S&P 500 fell 1.6% to 4,258.49. Energy, financials and industrials led the way down. It was the Dow’s worst day since October. Source: Seeking Alpha – S&P 500 IVV ETFAnd stocks had been slipping the previous week, and the week before that. Source: Seeking Alpha – S&P 500 IVV ETFFrom July 13, U.S. stocks fell some 4.6%. Canadian stocks also fell, by about 3.5% from the near-term peak. Modest declines, but the big question on Twitter and investment platforms and in the financial press was: Did you buy the dip? What? Mike the Dividend Guy chirped in with…

Yup, you could have had that price two weeks ago. Where was the excitement for buying two weeks ago, or even a month ago when stocks were cheaper?And yet it’s normal to hear so many brag that they “bought the dip.” Money seems to magically appear in investor accounts whenever there is a bad day or two in the markets. Or, that is, for those who post on social media. But if they were hoarding portfolio money waiting for a correction, they sold (or, make that bought) themselves short. There is no reliable way to time the markets. Hoarding cash does not work. If you’re in the accumulation stage, “buy ’em when you got ’em”. Make sure you’re investing within your risk tolerance level. Let rebalancing take care of asset prices that are moving in opposite directions over time. And rebalancing will naturally help you buy some low and then sell high. Dale Roberts is a proponent of low-fee investing who blogs at cutthecrapinvesting.com. Find him on Twitter @67Dodge.

Dale Roberts is a former investment advisor and proponent of low-fee investing. He created the Cut The Crap Investing blog in 2018. Find him on Twitter for market updates and commentary, every day.

Dale Roberts should have his own headline rather than being buried in another headline