Making sense of the markets this week: June 25, 2023

Is it a bear trap, or a new bull market? Stocks often don’t make much from these valuations, and bitcoin soars—thanks to new ETFs.

Advertisement

Is it a bear trap, or a new bull market? Stocks often don’t make much from these valuations, and bitcoin soars—thanks to new ETFs.

This week, Cut the Crap Investing founder Dale Roberts shares financial headlines and offers context for Canadian investors.

The last several months have been all about the rate hikes moving in slow motion. That framing is certainly playing out. It’s quite likely that we are in for a Summer of COVID and #revengespending. We want to buy experiences like travel and entertainment. Is this what’s keeping bankers up at night?

I have a couple of posts on my blog that sum up the stock-market events of the last few months. In early June, I have a headline read that ”The recession can wait.” Consumers and employers certainly did not yet receive the recession memo. So, economists and market experts keep pushing out their recession calls.

Just last week, it became official—we entered a new bull market in the U.S.

The year-to-date (YOY) returns have been very strong, which usually leads to very good one-year returns. I wrote:

“But in the long run, things have been overly positive. After rallying 20% from market lows, the S&P 500 averaged a 10% return over the next six months and 17.7% over the next 12 months.”

The debate that ensued: Are we in a new long-term bull market, or is this a bear market trap? Chief investment strategist for RIA Advisors and lead editor of the Real Investment Report, Lance Roberts (no relation) calls the new bull market, it’s different this time.

Of course, no one knows if this is the beginning of a long-term bull run until we are truly in one. But, there are many conflicting signals.

The Charles Schwab team and its managing director and chief investment strategist released the Schwab Market Perspective: Different Speeds, stating:

“Sometimes it feels like the economy and markets are on different tracks. Although leading economic indicators have been flashing recessionary signals, the S&P 500 index has plowed higher. Manufacturing activity is weak while services are resilient. The [U.S.] Federal Reserve declined to raise short-term rates at its June meeting for the first time in more than a year—but made it clear the door is still open to future rate hikes. Meanwhile, Europe is in a recession and a bull market at the same time. As we enter the second half of the year, clarity remains elusive. We see positive signs ahead, but also potential risks.”

The markets keep teaching us that we don’t know what is going to happen.

Investors sitting on pots of cash (stuck in market timing) might dollar-cost-average and get that money in the market over the next two years.

Take out the guesswork. Take out the emotion. The song remains the same; inflation is in charge. This brief video from Frances Donald, global chief economist and Strategist for Manulife Investment Management, sums up my view on things. Parts of inflation are sticky, and the U.S. Federal Reserve and other central bankers, including the Bank of Canada (BoC), will not create a damaging recession that’s necessary to bring inflation to the 2% target.

I’ll take “Things Central Bankers Don’t Want Me To Say” for $800, Alex. https://t.co/TxqjBX1nb5

— Frances Donald (@francesdonald) June 21, 2023

I think there’s a good chance that inflation settles in the area of 3% to 4%. Wage pressures, de-globalization and the energy green shift all present inflationary pressures.

At the same time, we should recognize that inflation is highly unpredictable, and the stagflation period of the 1970s and early 1980s demonstrated that wild swings are possible.

That is what keeps central bankers up at night.

We cannot time the markets, but we can control what we buy. Value investors typically buy companies that offer reasonable current valuations. And certainly they want and need some solid growth in the mix.

Now, in mid 2023, U.S. stocks are expensive. Let’s not forget the lost decade for U.S. stocks.

The poor returns in the period of the dot-com crash were due to extreme exuberance. The markets simply sold at unreasonable valuations, due to the run in tech stocks.

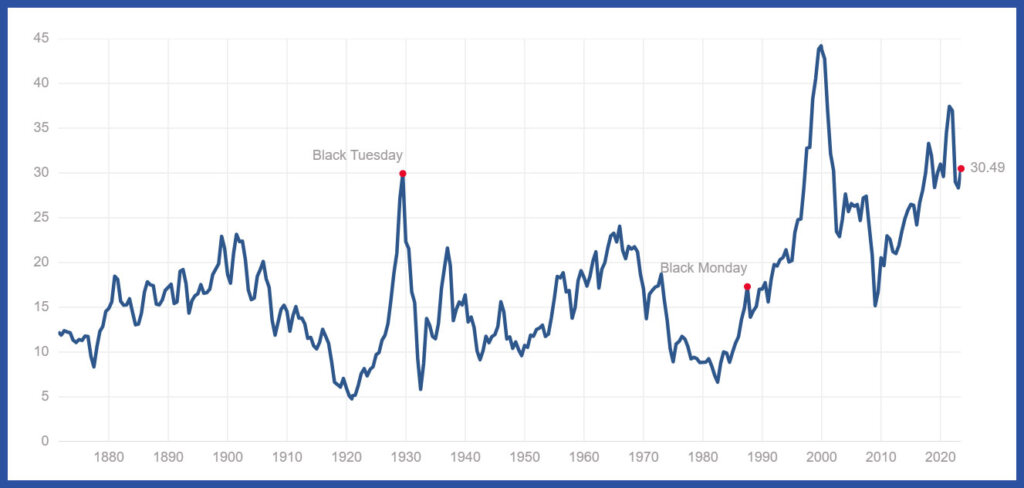

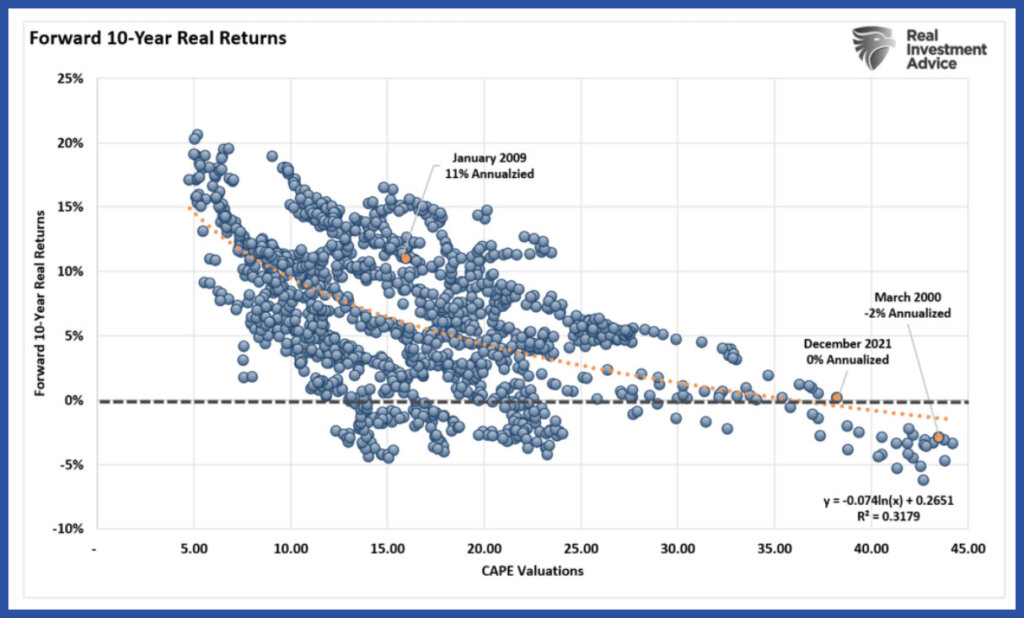

Here’s the historical CAPE ratio for the S&P 500. (CAPE is the cyclically adjusted price to earnings ratio.)

While we’re not in the nosebleeds section of the dot-com crash, the markets are very expensive by historical standards. But that valuation is driven by several stocks that are also mostly responsible for the stock market index gains in 2023.

And while not perfect, the CAPE ratio provides a range of expected real returns over a 10-year period.

And when we look at the forward earnings and earnings that factor in growth prospects (PEG ratio), investors are certainly paying up these days.

What investors are willing to pay for Earnings growth. WOW. https://t.co/mOqET2EQhc

— Martin Pelletier, CFA (@MPelletierCIO) June 19, 2023

And this chart shows the rise in the price-to-sales ratio for “the great eight companies” in 2023.

NVIDIA’s $NVDA price to sales ratio recently eclipsed 40. Is that sustainable? Here’s a look at mega-cap P/S ratios.https://t.co/srbpAWEzWX pic.twitter.com/oRKlFUjEnw

— Bespoke (@bespokeinvest) June 17, 2023

Being in semi-retirement, I’d put my money on the cheap(er) stocks and markets. I try to avoid any stocks I feel are at unreasonable valuations. Last week, I wrote about selling our winners. A (limit) sale price target was filled for Microsoft in my wife’s registered retirement savings plan (RRSP) account this week. I set another limit sale at 10% higher.

For those who don’t like the valuation story for the S&P 500, many look to the equal-weight S&P 500 index, (RSP/NYSE). There are value ETFs, and there are high-dividend ETFs, such as Vanguard’s (VYM:NYSE). Big dividends can find big value at times. We see that continually or almost perpetually in Canada with the Beat The TSX Portfolio. And some look abroad, to international and emerging markets, for greater value.

Case in point: Canadian stocks. They are trading 10% below their historically typical price-to-earnings levels, with enticing dividend yields as well.

Canada’s S&P/TSX Composite Index closed Thursday down 0.24%, its lowest finish since the start of June.

FedEx reported weaker earnings and lowered guidance, volume weakness was offset by cost actions, and non-GAAP earnings per share $4.94 (beat estimates by $0.07). (GAAP stands for generally accepted accounting principles. And non-GAAP does not and it doesn’t include items like non-recurring or non-cash expenses.)

This comes from FedEx’s financial report:

“The quarter’s results were negatively affected by continued demand weakness and cost inflation, partially offset by cost-reduction actions and U.S. domestic package yield improvement.”

For full-year guidance in 2024 guidance FedEx sees flat to low single-digit revenue growth.

There is also a decline in the movement of goods as a general trend.

🇺🇸 Truck Tonnage

— ISABELNET (@ISABELNET_SA) June 21, 2023

The drop in truck tonnage indicates a decrease in demand

👉 https://t.co/blMxcoFA78

h/t @MorganStanley #markets #ATA #truck #trucks#trucking #freight #recession #recessions #investing pic.twitter.com/dhwpZoptUw

There are signs of weakness in North American rail traffic. As how I started off this column, consumers are choosing experiences over buying goods. This may also be an early sign of a weakened consumer, as higher borrowing costs begin to bite.

And here’s more fodder for the (eventual) recession crowd:

May marked 14 consecutive monthly contractions for Leading Economic Index (LEI) from @Conferenceboard … a streak only seen in recessions that started in 1973 and 2007 pic.twitter.com/i8eDnBiwPa

— Liz Ann Sonders (@LizAnnSonders) June 23, 2023

As for Empire Co. (parent of Sobeys), it reported earnings on Thursday morning. This member of the Canadian Wider Moat Portfolio reported some solid earnings, and they raised its dividend by 10.6%.

Remember the wider-moat portfolio will include the grocers and railways, I can find no better Canadian stock portfolio for a market beat and risk-adjusted returns. Empire says its fourth-quarter sales totalled CAD$7.41 billion, down from CAD$7.84 billion in its fourth quarter last year, which included an additional week.

Same-store sales were up 1.6%, while same-store sales, excluding fuel sales, were up 2.6%.

Metro (MRU/TSX) delivered very good results in its recent report, as has been the trend for Canadian grocers. It reported food same-store sales up 5.8%, and pharmacy up 7.3%.

Seems the grocers can provide a much-needed inflation hedge.

Crypto is back on some radars. Namely as BlackRock (BLK: NYSE) shocked the investment world this week, announcing it would create a bitcoin spot price exchange-traded fund (ETF). “Spot price” means that the funds would hold bitcoin.

Many other asset managers are lining up their own bitcoin funds.

Quick inventory of spot bitcoin ETF filings since last Thursday…

— Nate Geraci (@NateGeraci) June 21, 2023

iShares (world’s largest ETF issuer)

Bitwise (knows space inside & out)

WisdomTree (top 10 issuer)

Invesco (4th largest issuer)

What changed recently?

SEC has been on warpath against crypto.

Something’s up.

Keep in mind that the iShares product offering is not a traditional ETF, but a trust as per bitcoin.com. But it will hold bitcoin, which is favourable for the bitcoin price, as it will increase demand for bitcoin.

As you may know, I wrote the go-to popular feature 🙂 on bitcoin as an investment, back in January 2021. From my research and observations, gold makes a balanced portfolio better. And for me and many others, bitcoin is seen as a modern or digital gold.

The bitcoin price hit USD$30,000 for the first time in a long while.

“The business models behind the vast majority of crypto tokens […] are ‘fraudcoins’ built solely on the ability to pump and dump them to the retail public.”

You might remember that Canada was out in front, first to offer bitcoin ETFs.

Whenever discussing bitcoin, we always stress that it is an extremely volatile asset. And there are many politicians and central bankers who would love to see the demise of bitcoin. But even the BoC is looking at going digital.

For those who like the idea of bitcoin as an investment, many use it sparingly in the area of a 2% to 3% portfolio weighting, as even 5% might be considered too aggressive.

I have a modest bitcoin position in my RRSP and continue to chip away at bitcoin and ethereum in my tax-free savings account TFSA.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

How Tesla and other companies are dealing with the uncertainty of the trade war.

Some Canadian seniors enter retirement without savings or run out of money over time. Here’s how they can stay...

If you carry a credit card balance in Canada, use our calculator to see how much you owe and...

Here’s how proposals from the NDP, Liberals, Conservatives and Green Party could affect your cash flow—and maybe help decide...

Yes, your estate will pay a high rate of tax on your RRIF when you die. But it usually...

Earth Day is on April 22. Here’s how to invest sustainably, and other ways to help the planet.

Canadian depository receipts are one of the fastest-growing investment products in Canada. Here’s what to consider before investing in...

Here’s why you might see an RRSP deduction limit on your notice of assessment, even when you’ve already converted...

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...