By Dale Roberts on June 4, 2021 Estimated reading time: 9 minutes

Making sense of the markets this week: June 7, 2021

By Dale Roberts on June 4, 2021 Estimated reading time: 9 minutes

Full-time office spaces are over—but what does that mean for REIT investors? Canadians are divided on the promise of a new retirement income product; the TSX Composite tops 20,000 for the first time; and we look at how rising yields might affect your portfolio.

This article is 3 years old. Some details may be outdated.

Advertisement

Photo by Cherrydeck on Unsplash

Each week, Cut the Crap Investing founder Dale Roberts shares financial headlines and offers context for Canadian investors.

Canadians are not ready to return to the office

It may be no surprise that Canadian employees aren’t eager to get back to their offices—at least not in a full time capacity. This recent poll suggests only 20% of Canadians are missing their business attire, commutes, expensive takeout coffees and packed lunches. From that CTV News post:

“A recent poll by Leger and the Association for Canadian Studies has found that 82% of Canadian respondents who have worked from home during the pandemic have found the experience to be very or somewhat positive, while just 20 per cent want to return to the office every day.

“Only 17% described working from home as somewhat or very negative.”

And, as has been suspected for many months, we might be looking towards hybrid workplaces in the future.

“Almost 60% of those surveyed said they would prefer to return to the office part-time or occasionally, while 19% said they never want to go back.

“The top three reasons for preferring to continue to work from home were convenience, saving money and increased productivity.”

Employers might have to give into these employee “demands” because…

“Some 35% of those surveyed in Canada agreed with the statement ‘If my superiors ordered me to go back to the office, I would start to look for another job where I can work from home’.”

Canadians are looking for flexibility. We might very well work from home one day, and then work from our offices the next. What does that mean for investors? Many REITs are concentrated on office space. And a hybrid-work future means we won’t be seeing the death of the office. However, office REITs might have to update their resume and approach. And they will face competition. With white-collar workers heading up those tower elevators for important meetings, perhaps many companies will no longer need the conventional desk-per-headcount setup. Could that mean the offices of the future will consist only of meeting rooms?WeWork, the company that offers flexible and satellite office space, has struggled during the pandemic, as their offering is not exactly work-from-home friendly. But they believe a hybrid work space is the future—where “employees have the ability to work in different spaces, including corporate offices, coworking spaces (such as WeWork), public spaces and from home.” What about picking up that coffee and other retail? In a hybrid future, those lineups at Tim Hortons and Starbucks could continue to be on the short side. The continued loss of food-court traffic and other local businesses (including restaurants) might be an ongoing theme. And that loss of business might have more of an effect on employment recovery prospects. In the early days of pandemic, we reported in this space on how retail workers faced the full (and perhaps unfair) brunt of economic hardship. That theme continued throughout the pandemic. They did not, and do not, have the luxury of working from home. As a freelance writer and blogger, I’m more than happy to be staying home, with homemade coffee, while dressed in shorts or sweatpants. Maybe Walmart will be a main benefactor of the hybrid workplace? I just love that stock. I’m guessing that it is also ready for the hybrid workforce. We’ll keep an eye on this very interesting recovery story.

The TSX tops 20,000 for the first time

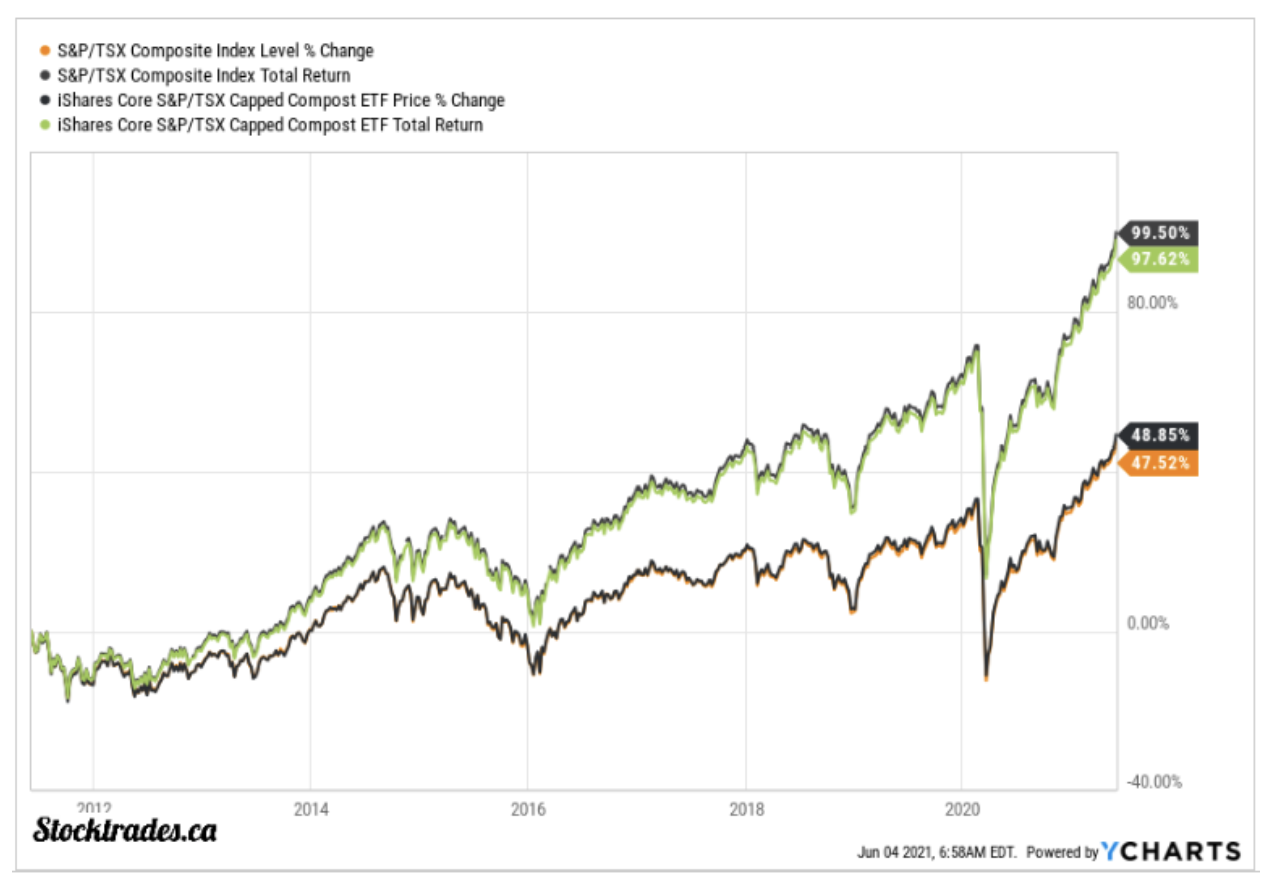

The Canadian stock market as measured by the TSX Composite hit a major milestone this week: On Wednesday, June 2, it broke 20,000 for the first time ever. To appreciate what a big deal this is, here’s a quick history lesson.The index broke 5,000 in the Spring of 1996. It quickly doubled to reach 10,000 in mid-2000, according to Trading Economics, but the dot-com crash that took down stock markets around the world, including in Canada. The Canadian market fell below 10,000 in that crash. The TSX then broke through 10,000 again five years later in 2005. The financial crisis of 2008-2009 took down the markets again, sending the TSX composite below 10,000 once again. It was not until the late Spring of 2009 when the market enjoyed a sustained rally above that 10,000 level. Then it took another 12 years for the TSX composite index to double from that 10,000 level in 2009 to 20,000 this month. Here’s the double double scorecard:

TSX Composite

5,000 to 10,000 – 13 years

10,000 to 20,000 – 12 years

Keep in mind that TSX Composite benchmark returns are not total returns, and do not include the reinvestment of any dividends. The index is price-only. Courtesy of friends at Stocktrades.ca, here’s a chart that reflects the (massive) difference between price-only indices, and indices that include the reinvestment of all dividends. The total returns for iShares Capped Composite Index ETF (XIC) is also thrown into the mix along with the underlying S&P TSX capped composite price-only index. Source: Stocktrades.caAlso, we do not know if this is a sustainable breach of the 20,000 mark. In fact, the index did not hold that level on Wednesday. On Thursday, the market closed at 19,941. And by Friday it was flirting once again with the territory above 20,000 points.In the 14 months since the depths of the COVID market crash, the Canadian benchmark has risen by about 78%. This is one of the strongest bull runs ever. The recent rally and new milestone are courtesy of the rise in inflation-friendly sectors, such as financials, energy and industrials. And, as has been mentioned many times in this space, the Canadian market rally owes a good deal of credit to Shopify, a stock that has quadrupled in price from the pandemic bottom.

Purpose Investments rocks the retirement world

On Tuesday, June 1, Purpose Investments introduced what may turn out to be a game-changer for Canadian retirees and for Canadian investors. The Longevity Pension Fund is designed to pay out at a rate of 6.15% annually. Did Purpose just redefine retirement income for life?As I wrote on my blog, Cut The Crap Investing, compared to the popular VRIF retirement income ETF and other options, this product just gave Canadian retirees a massive raise. (You’ll find VRIF among Best all-in-one ETFs for 2021.) The Longevity Pension Fund’s announcement set off a flurry of responses, with a mix of excitement, curiosity, confusion, and outright contempt and dismissal. The fund uses an interesting and innovative structure. For a backgrounder on the offering, you might start with this wonderful 2018 post on MoneySense from Jonathan Chevreau: Why Ottawa needs to push for tontine-like annuities. From that post, referencing a study conducted by retirement expert and academic, Moshe Milevsky says…

“While a tontine revival could make sense around the world—the pension and longevity trends are almost universal—they make particular sense in Canada. The authors state they “believe that Canada has a dearth of products for hedging personal risk, compared to the U.S. market.’ They know of no Canadian insurance company that offers a true deferred income annuity (DIA or ALDA), nor do they offer a variable income annuity or equity-indexed annuities with living benefits: all available in the U.S. The closest we have are segregated funds, and they really aren’t that great as far as guaranteeing lifetime income.”

All said, the Longevity Pension Fund is not a tontine (call it a modern tontine if that makes you happy); it is more like a pension model that is a mutual fund. While there are underlying investment assets, the secret sauce is the mortality credits. From the post on my site, and an explanation offered by Purpose CEO Som Seif…

“It is based on what they call Longevity Risk Pooling. The difference between the required return on the fund (net 3.5%) and the income paid to investors (6.15%+) is because when people buy, they get their income, but as some people redeem/pass away earlier, they leave behind in the pool their returns on their invested capital (they get their unpaid capital paid out upon death or redemption). These returns left behind reduce the total return required to provide the income stream for all investors.”

Stay tuned. Jonathan Chevreau will be back next week with a dedicated post on this new retirement offering. While there is more research to do, I am in the camp that this pension/mutual fund has the potential to be a game-changer for Canadian retirees.

How rising yields might affect your portfolio

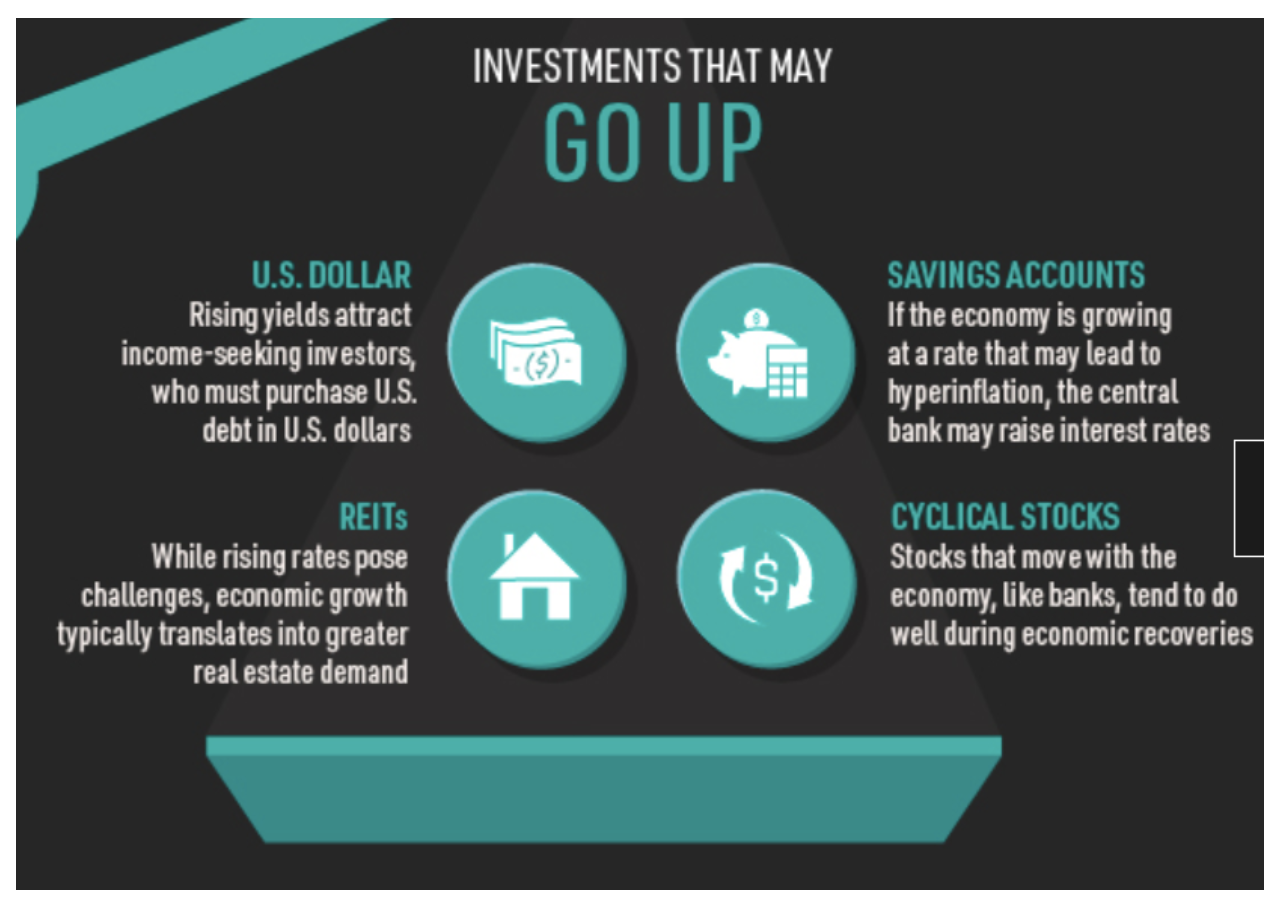

Here is a more than useful and interesting visual presentation from Visual Capitalist and New York Life Investments. More on the investment topic du jour, here is how rising treasury yields impact your portfolio. Of course, one of the main threats for the stock markets is that inflation will be robust and lasting, and that can lead to a rising-rate environment. Those conditions are known to be a stock market rally-killer at times. What does that mean for your portfolio? From that Visual Capitalist infographic, when treasuries are on the rise… Source: Visual CapitalistAnd on the flipside, er, make that upside… Source: Visual CapitalistWithin the document, be sure to check out the dedicated graphic on REIT performance during the various levels or rising yields. REITs can be a wonderful portfolio building block. Visual Capitalist’s infographics and commentary reinforce that an investor can create an all-weather portfolio that is ready for all conditions, including a rising-rate environment. Investors might also consider a bond barbell strategy. Shorter bonds or a short bond ladder will have the ability to increase their payments as the rates rise. The longer-dated bonds, such as Treasuries, can keep an eye on the stock markets. They offer the potential for “convexity”—to go up when stock markets go down. Of note within the document is a warning for dividend investors—a.k.a. many Canadian investors. That said, those banks might end up being your best friend in a rising-rate environment. And keep in mind, as we discussed earlier, rising rates don’t always follow inflation. Dale Roberts is a proponent of low-fee investing who blogs at cutthecrapinvesting.com. Find him on Twitter @67Dodge.

Dale Roberts is a former investment advisor and proponent of low-fee investing. He created the Cut The Crap Investing blog in 2018. Find him on Twitter for market updates and commentary, every day.