Making sense of the markets this week: March 22, 2021

Is investing in bonds now a "stupid" move? Plus: Unpacking the U.S. Federal Reserve's comments on growth and inflation; Rogers comes a-courting Shaw; and more.

Advertisement

Is investing in bonds now a "stupid" move? Plus: Unpacking the U.S. Federal Reserve's comments on growth and inflation; Rogers comes a-courting Shaw; and more.

“The world is a) substantially overweight in bonds (and other financial assets, especially U.S. bonds) at the same time that b) governments (especially the U.S.) are producing enormous amounts more debt and bonds and other debt assets.… Their overweight position in U.S. bonds is largely because of the ‘exorbitant privilege’ the U.S. has had being the world’s leading reserve currency, which has allowed the U.S. to overborrow for decades. The cycle of becoming a reserve currency, overborrowing, and being over indebted threatening the reserve currency status is classic.”

The investment world has been in a bond bull market from the early 1980’s. It’s all we’ve known. Again, from Dalio’s LinkedIn post …“If bond prices fall significantly that will produce significant losses for holders of them, which could encourage more selling. Bonds have been in a 40-year bull market that has rewarded those who were long and penalized those who were short, so the bull market has produced a large number of comfortable longs who haven’t gotten seriously stung by a price decline. That is one of the markers of a bubble.”

We are not used to getting hurt (or, at least seriously hurt) by our bond holdings. We suffer from that recency bias. We should keep in mind that bonds change in price and can carry risk. Even a traditional balanced portfolio could deliver no real (inflation-adjusted) returns for several years. Low yields bonds offer very little moving forward in the way of returns, even if rates stay somewhat stable. On their own, bonds are obviously not a great risk/reward proposition. That said, when we manage a well-balanced portfolio, we do not look at an asset in isolation. It is about the sum of the parts and the rebalancing among the parts. We should also step back and remember that we do not know, with any certainty, where any asset will go within the next year, or 10 years, or 20 years. Mike Philbrick of ReSolve Asset Management offers…“No one seems to ask themselves the simple question—if I could admit to myself that I don’t know the future—what portfolio would I hold?”

Short-term moves and fear should not throw us off our portfolio models that build and protect wealth over time. More from Philbrick…“Thoughtful portfolio diversification is about preparation, not prediction. There are many disinflationary dynamics like debt and technology at play so the current reflation trade could absolutely be transient—if so, then bonds will rule the day again and the reflation trade will have a serious correction.”

A key word in there is “could.” Referring back to that first quote, Philbrick will admit he does not know the future. I also checked in with Yves Rebetez of Credo, who acknowledges bonds might still play a stabilizing role in the portfolio. But are they worth it? He adds…“How do you grow wealth compounding at paltry 1.5% yields when inflation is 2% or more? Taxes on income might also seriously bite into it.… I don’t like to invest to lose…[and] bonds don’t look like much of a decent value proposition”.

On their own, bonds don’t make much sense. But, to my mind, their place in our portfolios is to keep an eye on those stocks. Here’s where I net out: We don’t know the future, so we should not guess. We should stick to our portfolio knitting but also check to ensure that we have the economic bases covered. I think, as a guess, that we will have head-fake inflation and a fleeting economic burst. The greater forces are still disinflationary, and those disinflationary forces increase thanks to debts, tax increases, technology and poor demographics in many parts of the developed world. That said, I will also protect against robust inflation, as I have discussed many times in this column. For real inflation: gold, investing in bitcoin and commodities, resource stocks. And on the bond front, we can create a bond portfolio that potentially protects against stock-market corrections while a component also reacts positively to inflation and rising rates. We might consider a bond barbell approach. Rebetez echoed the benefits of that barbell option. Rather than selling my bond ETFs, I am looking to add to those positions in modest fashion. I don’t know the future.Could we all be wrong? The markets will let us know, in good time.MS believes current market cycle will be intense, but short pic.twitter.com/2GjjqxWFe3

— Scott Barlow (@SBarlow_ROB) March 16, 2021

“We got substance to the Fed’s new, strategic brainwork and reaction function, which was implemented last year. But this was the first time for the Fed to put some real meat on the bones with numbers.”

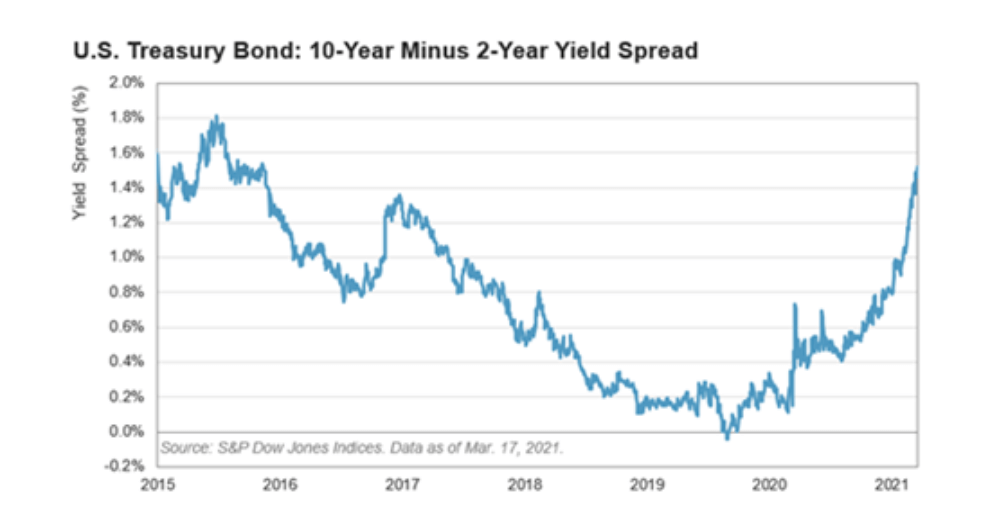

S&P Global offered a very good summary (sent to my email inbox):“With no rise in U.S. rates expected before 2023, but expectations of 6.5% GDP growth for 2021, it’s no surprise to see the U.S. yield curve steepening.

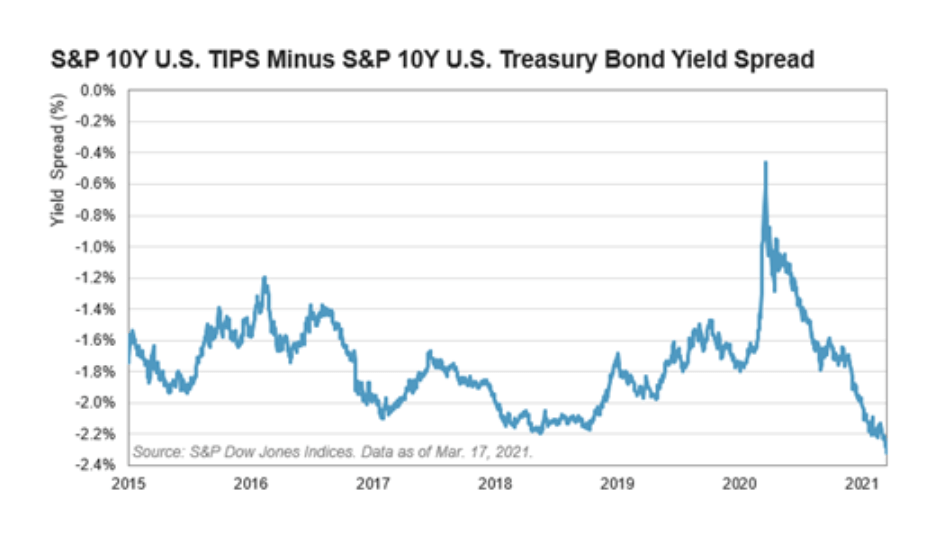

“Meanwhile, the spread between 10-year inflation-protected and nominal U.S. Treasury yields also closed at multi-year extremes yesterday, suggesting that the bond market wasn’t convinced by the Fed’s view that inflation would be transitory and is adjusting expectations for how hot the central bank will allow inflation to run.”

“The S&P 500 gapped up during yesterday’s Fed press conference to finish the day in positive territory. Futures reversed to give up the gains overnight, as a sell-off in the Treasury markets saw the benchmark 10-year yield visit 1.74% in early trading this morning.”

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

If your landlord defaults and the home is sold, your tenancy may still be protected—but rules vary by province....

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Robinhood’s WonderFi acquisition closes as Shopify adds US$3 billion to its buyback plan and Apotex targets a $1-billion IPO.

Leaving a TFSA to a U.S. spouse can trigger complex IRS reporting and costly tax issues. Here’s why some...

Wealth building starts with small, consistent habits. Here’s how young Canadians can save, invest and grow their net worth...

Canadian bank earnings season delivered higher profits, lower credit-loss provisions and dividend increases across much of the sector.

Gig workers and freelancers face uneven cash flow, but experts say consistent investing is still possible with the right...

Canadian depository receipts may offer convenience and accessibility, but they come with numerous trade-offs investors should be mindful of.

I have had various answers to this question before. Should an investor with guaranteed pensions (company and CPP/Old Age) plus annuities count them as the “bond” portion(s) of a balanced portfolio?