Making sense of the markets this week: March 3, 2024

Banks do well despite loan issues, why we’re not waiting for a stock market bubble to burst, navigating Nvidia’s historic gains, and, yes, RRSPs can be a great tool—not a scam.

Advertisement

Banks do well despite loan issues, why we’re not waiting for a stock market bubble to burst, navigating Nvidia’s historic gains, and, yes, RRSPs can be a great tool—not a scam.

Kyle Prevost, creator of 4 Steps to a Worry-Free Retirement, Canada’s DIY retirement planning course, shares financial headlines and offers context for Canadian investors. And Stephanie Griffiths was an award-winning investor for almost 20 years before returning to her roots in journalism. She is a consulting editor and journalist for MoneySense.

This week, Canada’s Big Five banks (six with National Bank) reported earnings for the three months ending January 31, 2023. All six reported significant increases in provisions for credit losses (PCLs), as homeowners and other borrowers struggled with inflation and the impact of higher interest rates. (Provisions for credit losses represent a bank’s estimate of loans at risk of defaulting. PCLs reduce the bank’s earnings.)

Here’s how Canadian banks performed in the three months ending January 31, 2024.

BMO commented that its customers who renewed their mortgages in 2023, saw an average increase in payments of 22% for variable rate mortgages and 21% for fixed rate mortgages. (Check out MoneySense’s Mortgage Renewal Calculator and best mortgage rates in Canada table.)

Of the six banks, only BMO failed to beat analysts’ estimates, with a miss of about 15% that drove the stock down more than 3% on Tuesday. The shortfall was attributed to weak capital markets revenue and increased provisions for credit losses.

BMO CEO Darryl White said he was confident results will improve. “We expect North American economic growth to remain subdued in the first half of this year before recovering towards the end of the year on the back of lower interest rates.”

CIBC and National Bank of Canada beat consensus estimates by 9% and 10%, respectively, while RBC and Scotiabank outperformed expectations by more modest margins. All four offset hefty increases in loan loss provisions with strength in other parts of their businesses.

In the U.S., though, Berkshire Hathaway (BRK.A, BRK.B) released its results last week, reporting that operating earnings for the conglomerate’s underlying businesses rose 21% in 2023.

In his annual letter to shareholders, a must-read for many investors (including Canadian investors), CEO Warren Buffett emphasized Berkshire’s financial strength and ability to weather panics and “market seizures,” which historically have yielded attractive investment opportunities. Some readers viewed these comments as bearish, raising the question of if the U.S. market is poised for a fall?

“The S&P 500 keeps notching fresh records and tech stocks, particularly those exposed to artificial intelligence, are on a tear,” writes Callum Keown in Barron’s. “But the Sage of Omaha appears to be far more cautious.” —S.G.

Get up to 3.50% interest on your savings without any fees.

Lock in your deposit and earn a guaranteed interest rate of 3.65%.

Earn 3.7% for 7 months on eligible deposits up to $500k. Offer ends June 30, 2025.

MoneySense is an award-winning magazine, helping Canadians navigate money matters since 1999. Our editorial team of trained journalists works closely with leading personal finance experts in Canada. To help you find the best financial products, we compare the offerings from over 12 major institutions, including banks, credit unions and card issuers. Learn more about our advertising and trusted partners.

Ever since the 2008 market crash, it’s become popular for talking heads on TV to use the phrase “bubble.”

According to The MoneySense Glossary for personal finance and investing terms—for Canadians:

“A market bubble occurs when prices (of anything from housing to stocks) rapidly rise to unprecedented levels and then collapse. Bubbles expand as frenzied buyers push prices higher and higher, fuelled by hype and fear of missing out. Bubbles eventually burst when sentiment shifts, sellers vastly outnumber buyers and prices implode. Examples include the Dutch tulip bulb mania of the 1630s, the dotcom stock market bubble of the 1990s and the U.S. housing bubble that burst in 2008.”

Read more about market bubbles in the glossary.

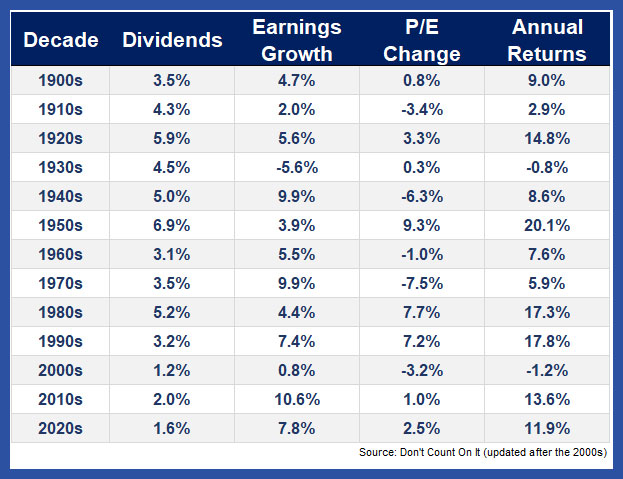

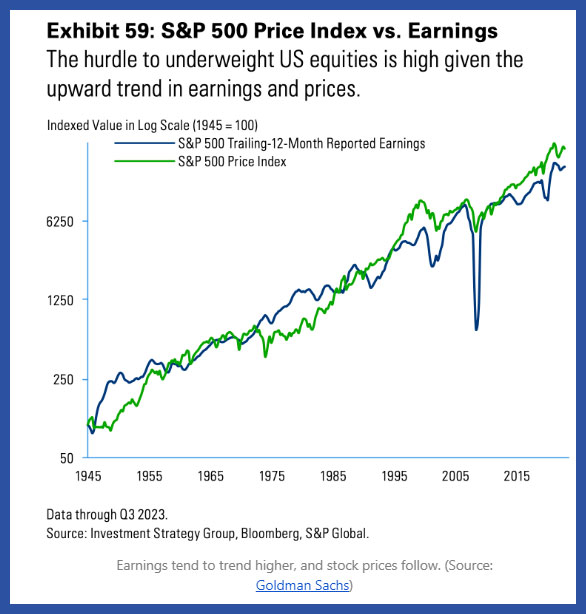

So, to figure out if an asset—in this case, the U.S. stock market—is in a bubble, we should look at how much of the current value is driven by the fundamentals (like earnings) and how much of it is due to exuberant traders getting caught up in the latest fad.

Ben Carlson had an interesting take on the latest data including the two charts below.

The main takeaway from this data: By and large, the value of the 500 largest U.S. companies that make up the S&P 500 closely track the actual amount of profit those companies are making. This is a good thing. It means there’s something tangible (namely, a group of increasingly profitable companies) to back up the rise in value (unlike assets such as gold or cryptocurrency, for example).

Three takeaways from Carlson’s report:

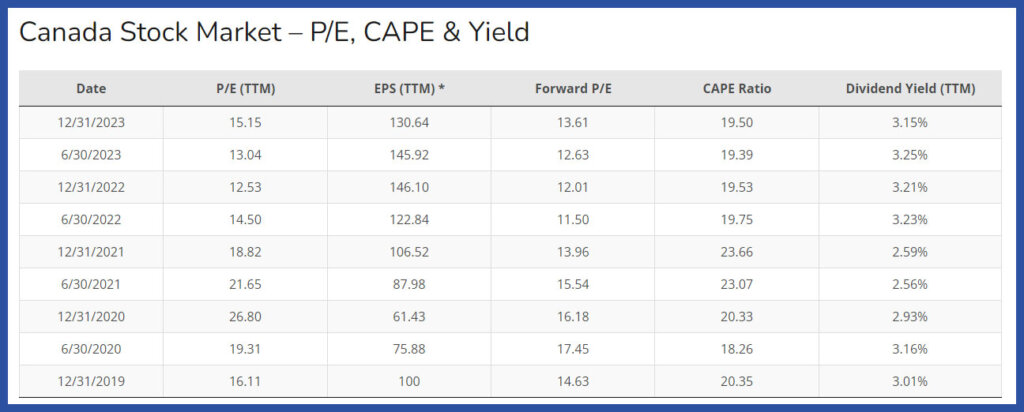

My takeaway: While Canadian companies aren’t as profitable as the American ones, a similar valuation versus earnings model does seem to fit.

Note: CAPE ratio refers to Cyclically Adjusted P/E, a metric designed and trademarked by economists Robert Shiller and John Y. Campbell. CAPE uses 10 years of inflation-adjusted earnings in its calculation instead of a single year.

Now, all of this isn’t to say that the stock market is currently recession-proof. Obviously investors could get pessimistic about owning stocks, and a bear market can happen at any time. What I’m simply saying is that we are very unlikely to see a large bubble burst because companies are simply making more and more money. As they earn more money, investors are willing to pay more to own a share of them. —K.P.

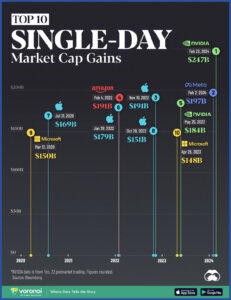

Last week I wrote about just how quickly Nvidia’s value has exploded over the last couple of years. And, I may have undersold just how incredible this company’s rise has been over the last few years and, to some degree, the rise of several of the U.S. tech giants, including the Magnificent Seven. These tech stocks are the big reason the U.S. stock market has so substantially outperformed Canada’s market and the rest of the world’s markets, too.

Here’s a look at the biggest one-day stock market gains in history.

You might notice pretty quickly that all these gains happened over the last four years, and that they are all part of the mighty U.S. tech story.

For perspective, Nvidia’s big day resulted in a market cap gain of USD$247 billion last week. That’s roughly the size of Canada’s two largest companies—TD and RBC—put together. So, Nvidia added a value of TD-plus-RBC-worth in one day. And earlier this month, Meta announced its earnings and gained nearly USD$200 billion in a day. From a total value perspective, it’s as if the company created both major Canadian railways from scratch, and added Suncor as well—all in one day. The sheer scale of the wealth generated by these companies is incredible.

It might be easy to dismiss this recent share price run up as a bubble, but the data referenced above would indicate that these companies have the earnings to back up their valuations to at least some degree. This isn’t the tech crazy of the early 2000s where non-profitable companies could just add “.com” behind their brand and turn founders into multi-millionaires.

I’m not sure I want to bet against a company with the recent track record that Nvidia has, but current expectations and valuations couldn’t be higher for this company right now. That’s a lot to live up to.

Now, that said, is the stampede of investors running out to buy Nvidia something to follow? It’s not exactly a slam dunk. The market appears to have done a pretty good job pricing this stock given all available information.

Nvidia doesn’t have much room left for multiple expansion when it comes to an increased share price for the stock. After accounting for its incredible earnings day, Nvidia is still trading at a P/E ratio of 66x. Even fellow tech heavyweights Microsoft and Apple are only at 36x and 28x respectively. Consequently, if Nvidia continues its incredible bull run, one would have to believe that the demand for chips will continue to skyrocket and that Nvidia will be able to hold off competitors like AMD and Intel. —K.P.

With the deadline to contribute to registered retirement savings plan (RRSP) officially passed as of February 29, we wanted to quickly address the becoming prominent idea that RRSPs are some sort of scam.

We’ve noticed an increasing number of inquiries from friends and family over the last few years that go something along the lines of, “RRSPs are just a rip-off because you have to pay tax on them anyway.”

Since you’re reading a column called “Making sense of the markets,” you’re probably aware that RRSPs are not in fact an asset. The fact that some Canadians don’t understand is shocking. It’s important to understand precisely what RRSPs are.

RRSPs are a type of investment account—one that’s registered. It’s a place where you can hold investments, and it has powers that protect investments from taxation. If you think you’re purchasing RRSPs as an asset, then you might have gone to a bad wealth management company. A good financial advisor helps you understand what asset you were investing in. A bad financial advisor will be vague by using phrases such as “invest in RRSPs.” Investment information is often murky so money can be put into whatever high-fee investments (such as mutual funds) they wanted to sell that day. (Need an advisor? Check out MoneySense’s Find A Qualified Advisor tool.)

Of course, an RRSP doesn’t avoid taxes entirely. It defers tax on the contributed amount from when you relatively earn a lot of money (while working) to when you earn less money (when retired). If you get a tax refund when you contribute or owe less taxes when you contributed to a RRSP, that’s essentially the government saying, “Since you contributed to your RRSP, your taxable income this year is not as high as it would’ve been. So you don’t owe us that money now. Oh, and if you have children, we’ll likely increase your Child Care Benefit cheque, as well.”

If you get a refund, then invest it and let all of that money compound in low-fee investments for the next several decades, you’re very likely to be happy with the results. But those people who say “RRSPs are scams” are usually salespeople pedalling life insurance for higher commissions.

Yes, for some Canadians investing within a tax-free savings account (TFSA), it means they could come out ahead of investing within an RRSP. Yet, for the vast majority of Canadians, they could end up in a pretty similar place. Don’t forget, if you invest inside a TFSA, you don’t get that tax refund to stuff right back into your investment account—you’re contributing after-tax income. When deciding on a TFSA or an RRSP, you would need to know exactly how much income you and your spouse will have when you retire.

To keep things simple, if you make more than $100,000 a year from your salary, the RRSP investment account filled with low-fee investments (not mutual funds with MERs above 0.60%) is probably a great idea. Or, if you make less than $40,000, then the TFSA may be the better choice—as you’re not in a high enough tax bracket to be sure of any tax deductions.

If you’re between those two income levels, then your retirement income won’t likely be different from that of your working years. So, your tax rate may be similar, and it may not really matter if you choose a TFSA or an RRSP. With an RRSP, don’t forget about how awesome it was to get money back from the government and remember it’s worth considering investing any tax refunds. If you’re experiencing analysis paralysis, just choose one—and quit clicking “RRSPs are a scam” headlines. —K.P.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

What Canadians need to know about stablecoins, possible coins from Amazon and Walmart, and Canada launches three XRP ETFs.

RBC Direct Investing has introduced commission-free trades on 50 exchange-traded funds (ETFs) from partner iShares.

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

The latest earnings reports for Canadian investors from the cybersecurity and convenience-store giants.

Canada was ranked the fifth-most investment-curious country in a recent study, with higher-risk investments like stocks and crypto leading...

A MoneySense reader asks about survivor benefits for spouses. Here’s how defined benefit and CPP survivor payments work in...

The tax-free savings account is a great wealth-building tool, but it’s sadly misunderstood. Here are seven TFSA features Canadians...

Here’s why mutual funds don’t travel well across international borders—and what Canadian investors can do instead.

Created By

Ratehub

Most registered retirement savings plans are eventually converted to registered retirement income funds. Here’s what to know about RRIF...