Making sense of the markets this week: May 3, 2021

There's money to be made in energy, but fund managers are hesitant to go there; why Warren Buffett is sitting on $140 billion in cash; and is there growth outside of FAANGM?

Advertisement

There's money to be made in energy, but fund managers are hesitant to go there; why Warren Buffett is sitting on $140 billion in cash; and is there growth outside of FAANGM?

“Eric Nuttall: Should I be grappling with my own ‘existential threat’ as an energy fund manager with a focus on oil?”

The article frames the current energy reality for Canada and on a global scale. Including …“The world prior to COVID-19 consumed 102 million barrels of oil every single day and is projected to be back to that level by the end of this year.

“Roughly 60% of oil is used for transportation, while the remaining 40% is used for things such as petrochemicals, lubricants, and agriculture for which there is no real alternative.”

The use of oil and the need for oil will continue to increase for many years. Like you, I wish that we could “get off oil,” but that is not about to happen any time soon. I encourage you to read Nuttall’s post to obtain a topline view of that energy reality. I shared that Financial Post article on Twitter to put the energy idea on the table for Twitter #investorfriends and bloggers. And in a recent MoneySense column, I looked at the hesitancy of most Canadian equity fund managers. They are not enticed by the amount of free cash flow, nor the profits that Canadian oil producers are likely about to deliver. Let’s call that “energy hesitancy.” They are not increasing their weightings in the sector. Do retail investors also feel that energy hesitancy? The topic of global warming and the environmental impact of harvesting the massive amounts of energy in the Canadian oil sands leaves very few investors “in the middle ground.” We all appear to have strong opinions.Follow that thread on Twitter—you’ll see most of the comments put environmental concerns over any investment consideration. And that makes sense, of course; there are few things more important than the planet. But the reality is that our investment decisions won’t be what drives the shift to a greener economy. On final count, it is obvious that the retail investor is not enticed as well. I get the same energy hesitancy when I chat with advisors. Many yield-hungry Canadian investors will stick to their pipelines. (If you’ve been reading this column for a while, you’ll know I am still with the gang with respect to those big-paying pipelines.) This is not advice (I simply put investment ideas on the table), but I think energy is an obvious and missed investment opportunity. And it’s very likely oil use will peak and start to fall over time. This is perhaps not a forever buy-and-hold. But, near-term, I put it in the no-brainer camp; I hold iShares in the energy index ETF XEG in a couple of accounts. And I will invest in the future as well. We can prosper from that transition. Portfolio shift follows that green shift. Perhaps any traditional energy profits can feed green technology and clean energy investments. For me, this is some modest portfolio shading, part of the explore in the “core and explore” portfolio approach. I like those undeniable trends. Canadians can look to Evolve ETFs for groundbreaking themes such as automotive innovation. You can check out the Harvest Green Energy ETF. Google will help you with many more ways to green up the portfolio. You can keep an eye on the burgeoning green bond industry as well. These are vehicles that offer more of a direct investment in the solution."We produce one of the most ethical units of energy in the world and increasingly one of the cleanest."

— TheDividendGuy (@TheDividendGuy) April 28, 2021

Really?

So oilsands is clean energy now?

Thanks to Lance Roberts (no relation) and the Daily Shot for the chart. Roberts suggests the (collective) rest of the S&P 500 has offered no growth. It’s quite the choice.Why do we own a bunch of the #FAANGM? Precisely because of this. @RealInvAdvice @SoberLook pic.twitter.com/wcvA3KfeDo

— Lance Roberts (@LanceRoberts) April 28, 2021

That chart fits into a theme that I covered on my site—that growth will be even more scarce in the future. At least, according to economist David Rosenberg. That post looks at a few themes and ideas for growth. Of course, the U.S. market and those U.S. growth hotspots are very expensive. And they are expensive for good reasons, as they keep on delivering the goods. This week is a big one for U.S. earnings, and big tech is delivering big time. We can check in on some tech earnings here and here. Keep in mind, there are pockets of growth within the S&P 500 outside of big tech. And, collectively, they can deliver positive growth over time for the total index. I hold a U.S. portfolio of individual stocks and I see growth in the healthcare sector, financials and even among consumer discretionary stocks such as Lowe’s and Nike. Other sectors have the potential to pick up some slack as well. But, make no mistake, that chart is nothing short of fascinating; it shows us a great deal about the recent past and perhaps the future of growth and profitability.It is the choice of owning #growth or owning "#nongrowth"

— Lance Roberts (@LanceRoberts) April 28, 2021

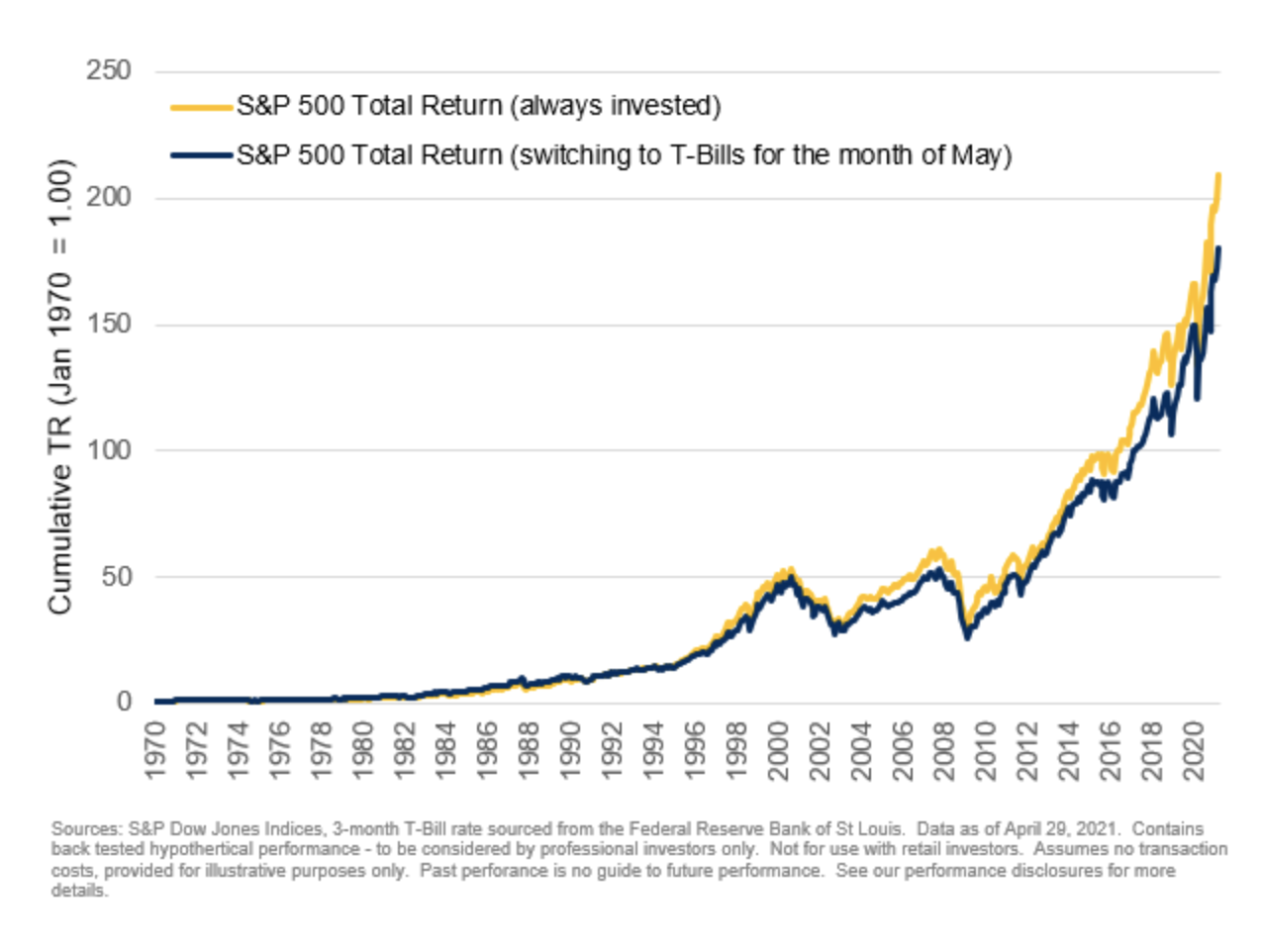

As the chart says: Don’t miss out on May.

Dale Roberts is a proponent of low-fee investing who blogs at cutthecrapinvesting.com. Find him on Twitter @67Dodge.

As the chart says: Don’t miss out on May.

Dale Roberts is a proponent of low-fee investing who blogs at cutthecrapinvesting.com. Find him on Twitter @67Dodge.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Yes, your estate will pay a high rate of tax on your RRIF when you die. But it usually...

Here’s why you might see an RRSP deduction limit on your notice of assessment, even when you’ve already converted...

Created By

Ratehub.ca

Once you start RRIFing, how do you make sure you have enough cash, and should you dial down risk?

There are several personal, trust and corporate income-tax-filing extensions for Canadians this year. Which ones apply to you? ...

Whether you have renters in your home or another property, know that the money you make can affect your...

What to consider when deciding to incorporate a company with friends to buy real estate and more.

Sorry not sorry: Restaurants revamp decor, menus to showcase Canadian ties.