Canada’s Best Mutual Funds for 2014

Prior picks have out performed their peers for over a decade.

Advertisement

Prior picks have out performed their peers for over a decade.

Note: BMO Entreprise Fund Classic is no longer available to new investors.

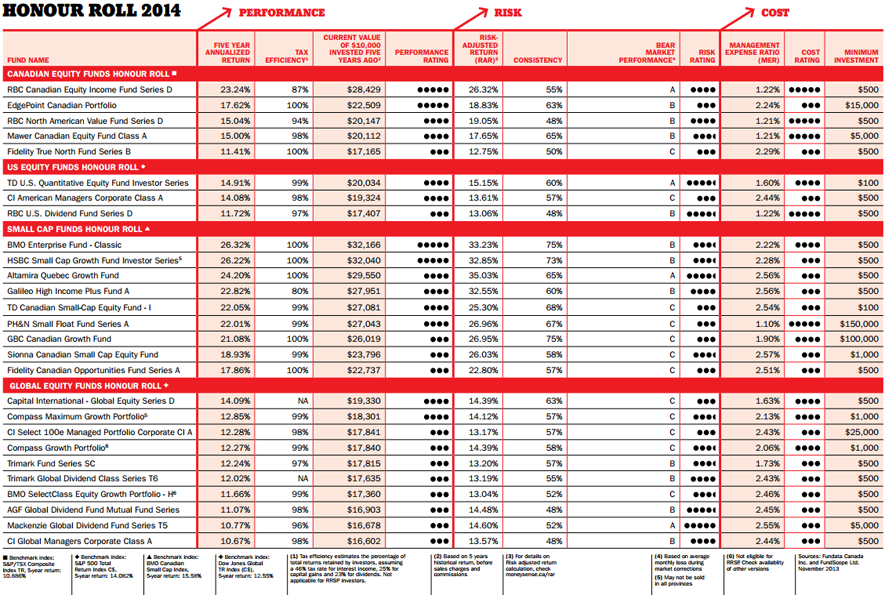

Overall ratings in each category go from one circle (poor) to five circles (excellent). Any Honour Roll fund is a good buy, but some may be better than others. For instance if investing outside an RRSP, pay particular attention to “Tax Efficiency.” This measures how much of a fund’s return has been lost to taxes on distributions. (Funds that don’t distribute cash don’t lose anything, so are rated at 100%.) In general, the higher this number, the better for funds held in taxable accounts. All investors should also consider risk. “Risk-Adjusted Return” shows how much return each fund has achieved in proportion to its risk—again, the higher, the better. To play it safe, look for funds with a high “Consistency” rating (which shows the percentage of months in which a fund has performed better than its peers) and strong “Bear Market Performance” (the best funds get ‘A’s and so on down to ‘E’s).

Note: BMO Entreprise Fund Classic is no longer available to new investors.

Overall ratings in each category go from one circle (poor) to five circles (excellent). Any Honour Roll fund is a good buy, but some may be better than others. For instance if investing outside an RRSP, pay particular attention to “Tax Efficiency.” This measures how much of a fund’s return has been lost to taxes on distributions. (Funds that don’t distribute cash don’t lose anything, so are rated at 100%.) In general, the higher this number, the better for funds held in taxable accounts. All investors should also consider risk. “Risk-Adjusted Return” shows how much return each fund has achieved in proportion to its risk—again, the higher, the better. To play it safe, look for funds with a high “Consistency” rating (which shows the percentage of months in which a fund has performed better than its peers) and strong “Bear Market Performance” (the best funds get ‘A’s and so on down to ‘E’s).

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Find out which Canadian robo-advisors offer the lowest fees, best support, top returns, and more, with MoneySense’s 2025 guide.

There are several personal, trust and corporate income-tax-filing extensions for Canadians this year. Which ones apply to you? ...

Young investors have many ways to build the fixed-income portion of their portfolios. Experts say to keep these two...

Ottawa defers effective date of capital gains changes to 2026 and promises exemptions for the tax inclusion increase.

What does 2025 have in store for Canadian investors? Who knows. But there are some trends to keep an...

Learn the tax implications of moving investments from Canada to the U.S. There’s lots to consider.

Looking back at 2024, we go through the Canadian and U.S. stock exchange predictions, as well as crypto, Tesla...

This advisor isn’t losing any sleep over the markets. In fact, looking back at 2024 and forward into 2025,...

Bank of Canada makes a big cut, U.S. inflation is up, Oracle ends a great year on a low...

Canada bank earnings remain on target, Dollarama’s expectations catch up to it, “insider selling” sets a new record, and...