Investors see value, but why won’t they act on it?

Investors continue to favour higher-fee active investments when lower-fee passive strategies are clearly better for them

Advertisement

Investors continue to favour higher-fee active investments when lower-fee passive strategies are clearly better for them

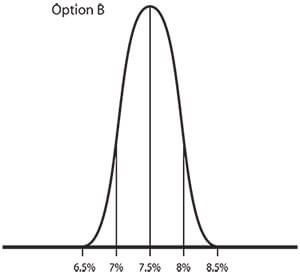

Option B (Beta-replicating) is predicated on mimicking a market.

Option B (Beta-replicating) is predicated on mimicking a market.

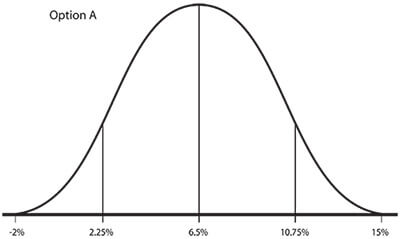

In my examples I’ll use a market return of 8% and then deduct the average cost of the products to determine the expected market return. Let’s assume that traditional active products (for example, F Class mutual funds) cost 1.5% and traditional passive products (for example, market-tracking ETFs) cost 0.5%. Those costs are likely a bit high, but the important thing to note here is that the difference in cost is about 1 percentage point.

In my examples I’ll use a market return of 8% and then deduct the average cost of the products to determine the expected market return. Let’s assume that traditional active products (for example, F Class mutual funds) cost 1.5% and traditional passive products (for example, market-tracking ETFs) cost 0.5%. Those costs are likely a bit high, but the important thing to note here is that the difference in cost is about 1 percentage point.

![]()

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Canadian depository receipts are one of the fastest-growing investment products in Canada. Here’s what to consider before investing in...

Here’s how proposals from the NDP, Liberals, Conservatives and Green Party could affect your cash flow—and maybe help decide...

Here’s why you might see an RRSP deduction limit on your notice of assessment, even when you’ve already converted...

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

As the grocer reports sales growth of Canadian products, the clothing retailer plans to increase its U.S. footprint. Here...

Created By

Ratehub.ca

Find out which Canadian robo-advisors offer the lowest fees, best support, top returns, and more, with MoneySense’s 2025 guide.

Nvidia plans to manufacture AI chips in the U.S. for the first time.

Canada’s Consumer Price Index fell in March amid the start of a tariff war with the U.S., the end...