Stock market news for Canadian investors: Eli Lilly, BCE and more

Eli Lilly, BCE, Suncor, Canada Goose, Bombardier, Thomson Reuters and Lightspeed reported earnings this week. Here are the details for Canadian investors.

Advertisement

Eli Lilly, BCE, Suncor, Canada Goose, Bombardier, Thomson Reuters and Lightspeed reported earnings this week. Here are the details for Canadian investors.

Canada Goose Holdings Inc.’s third-quarter profit ticked higher as the company worked to make its operations “more flexible and nimbler,” but warned of headwinds materializing in China.

The luxury parka maker revealed Thursday that its profit attributable to shareholders amounted to $139.7 million or $1.42 per diluted share for the quarter ended Dec. 29.

The result compared with a profit of $130.6 million or $1.29 per diluted share a year earlier.

The company has spent months “ruthlessly focused on prudently managing” headcount and costs, said Beth Clymer, Canada Goose’s president of finance, strategy and administration.

“This required new ways of working across our organization,” she said.

One of the ways was moving to manufacturing small quantities of main line product during the season in response to consumer demand signals.

For example, a run of the company’s popular fleece Chilliwack bomber was begun in Winnipeg, when interest piqued in the sweater recently.

The company also sped up timelines when it launched its capsule Snow Goose collection from creative director Haider Ackermann.

“These products included new fabrics, trims, and design features, yet we brought them from design conception to consumers in record time,” Clymer said.

She pointed out the job was also done with a smaller workforce because Canada Goose laid off 17% of its global corporate staff last March.

At the time, CEO Dani Reiss promised the cuts would put the company in a better position for scaling and help it focus on efficiency and key brand, design and operational initiatives.

“This is about being simpler and more effective,” Clymer reiterated Thursday.

Her remarks came as the company said it now expects low single-digit percentage to no growth for its adjusted profit per share for the year. Earlier expectations had been for a mid-single-digit percentage increase.

Its share price on the TSX fell almost 6% to $14.41 in late-morning trading as the market responded to the lower guidance and news that the company’s third-quarter revenue totalled $607.9 million, down from $609.9 million.

About a third of the revenue came from Greater China, which Carrie Baker, president of brand and commercial, said is “one of the company’s healthiest markets” because of its strong brand awareness.

The company has poured resources into Asia over the last several years, opening a rash of new stores in the market and recently launching live shopping on Douyin, a short video app from TikTok owner ByteDance.

The moves paid off, delivering strong sales during the recent Lunar New Year and Golden Week, the period of Asian holidays earlier in the year.

Yet Baker said Hong Kong, Macau and Taiwan are facing macroeconomic pressures and some stores in parts of Asia are seeing lower traffic levels.

Its third-quarter Greater China revenues fell 4.7%, when compared with a year earlier.

“It’s still a tough market, but we’re seeing the momentum in the places that we are investing in,” Baker said.

Retailers in China are facing headwinds because the U.S. recently decided to implement a 10% tariff on goods from the country. Canada Goose may also be impacted by 25% tariffs the U.S. has threatened to impose on Canadian goods in a month.

While Canada Goose did not face questions from analysts about the tariffs on Thursday, the company told The Canadian Press over the weekend that “tariffs will not change our path.”

It noted 70% of its products are manufactured within seven facilities in Ontario, Manitoba, and Quebec and said the company employs about 20% of the country’s “cut and sew industry.”

“We remain steadfast in our commitment to producing world-class products right here,” the company said Sunday.

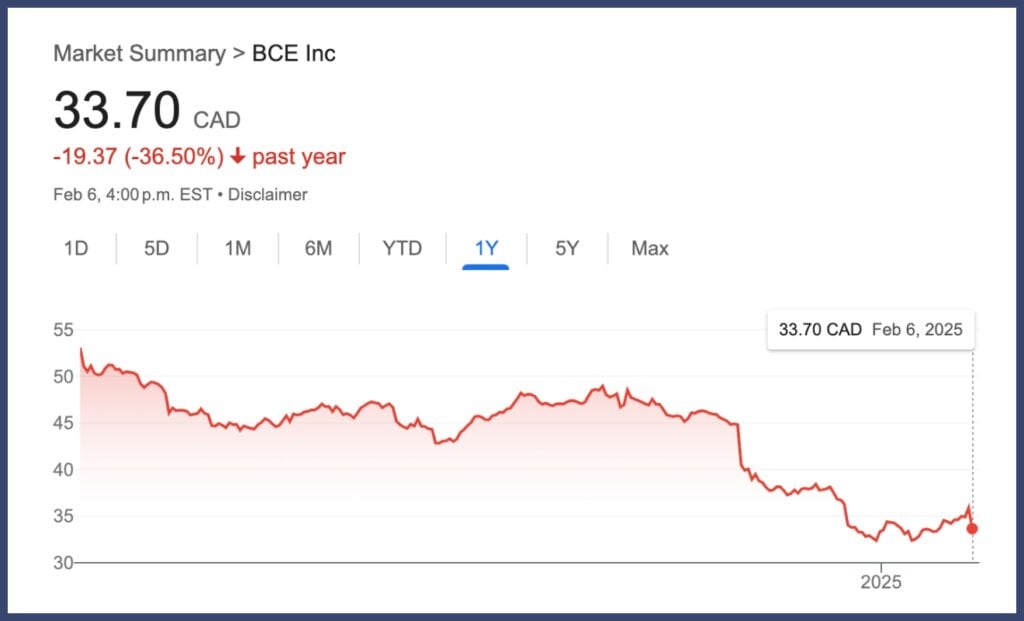

The chief executive of BCE Inc. blasted the national telecom regulator as he announced the company would further scale back the build of its fibre internet network.

The parent company of Bell Canada no longer plans to meet its previous target of reaching 8.3 million homes through its fibre footprint by the end of 2025, CEO Mirko Bibic said on Thursday, adding the company would make further capital spending cuts this year.

Bibic said the move is in direct response to a decision earlier in the week by the CRTC surrounding wholesale fibre services. Bell has been at loggerheads with rival Telus Corp. over whether Canada’s largest telecoms should be allowed to sell internet service in regions where they don’t own fibre networks, by paying the local incumbent to use their infrastructure.

The CRTC has so far sided with Telus in allowing them to do so—although it deferred a final decision on the matter until the summer—while Bell says that direction discourages the big players from investing in their own network expansions.

“To put it bluntly, we’re not in the business of building fibre for Telus’s benefit, and that’s what the CRTC policy that’s in place right now forces us to do,” Bibic told analysts on the company’s fourth-quarter earnings call.

He said it “makes no sense” that the CRTC would allow incumbents to resell internet service from each other at a time “when Canadian productivity is already lagging.”

“I don’t understand why a regulator would put in place policies that create disincentives to investment, puts jobs at risk, and puts at risk the building out of critical infrastructure,” he said.

“It seems like the wrong policy at exactly the wrong time.”

The CRTC has said its wholesale fibre rules are meant to level the playing field for smaller internet providers, many of which have struggled to compete with the big players.

After a limited version of the rules were set in late 2023, Bell responded by announcing it would cut network investment plans by more than $1 billion in 2024-25. On Thursday, Bibic said Bell had achieved more than 70% of those reductions by the end of last year and would cut “by more than we anticipated” this year in response to the regulator’s latest decision.

“We will revisit our build out plan if the CRTC reverses its decision,” he said.

The move raised questions from analysts over Bell’s investment strategy, especially given its pending $5-billion acquisition of U.S. fibre internet provider Ziply Fiber, which operates in the Pacific Northwest. Bibic noted that deal, which is expected to close this year, comes as Bell seeks to transform into a “fibre-first company.”

An analyst asked Bibic what he feared happening if Telus did come in to resell Bell’s fibre service and what opportunities the company has to perhaps resell fibre services in other markets in the future.

Bibic said the best form of competition comes from companies building their own infrastructure.

“We would always rather compete on the basis of networks we own,” he said.

“We want to build. We want to compete against other well-capitalized companies that build their own, and we’re prepared to do that here, obviously, in Canada, and we’re prepared to seize on the growth opportunities in the U.S.”

The Ziply Fiber deal is being financed largely though proceeds of BCE’s $4.7-billion sale of its stake in Maple Leaf Sports & Entertainment to rival Rogers Communications Inc.

It’s one of a few ways the company is seeking to monetize non-core assets, said Bibic, who also highlighted BCE’s $1-billion sale of Northwestel Inc. He said a broader review is underway to find up to $7 billion in non-core asset divestitures, a figure which includes the MLSE and Northwestel deals.

The company reported its net earnings attributable to common shareholders amounted to $461 million or 51 cents per share for the quarter ended Dec. 31, compared with a profit of $382 million or 42 cents per share in the last three months of 2023.

Operating revenue for what was its fourth quarter totalled $6.42 billion, down from $6.47 billion a year earlier.

On an adjusted basis, BCE says it earned 79 cents per share, up from an adjusted profit of 76 cents per share a year earlier. Analysts on average had expected an adjusted profit of 72 cents per share, according to estimates compiled by LSEG Data & Analytics.

In its outlook for 2025, the company provided revenue guidance that ranged from a decline of 3% for the year to an increase of 1%. Adjusted earnings per share for 2025 are expected to decline between 8% and 13% compared with 2024.

BCE expects to maintain its dividend at its current level after pausing any future hikes in November.

Desjardins analyst Jerome Dubreuil said the guidance is roughly in line with expectations, but “likely insufficient to turn investors’ perspective around on the stock.”

“BCE announced a significant capex cut, which could be the right thing to do in this environment,” he wrote.

“However, we believe it is fair to say that we should not count on capex (in Canada) to improve the top line going forward.”

He said he would not rule out a dividend cut later in 2025 “given the uncomfortable payout situation and accelerated spending in the U.S.”

BCE shares were trading at $34.28 midway through Thursday on the TSX, down $1.62 or around 4.5%.

During the latest quarter, BCE added 56,550 net postpaid mobile phone subscribers, down 56.1% from the same period a year earlier, which it attributed in part to Canada’s slowing population growth.

It also cited higher customer churn—a measure of subscribers who cancelled their service—which increased to 1.66%. Bell’s wireless mobile phone average revenue per user was $57.15, down 2.7% from the prior year.

“We need to get churn down,” Bibic said in a phone interview.

“I’m still not happy with churn, but we’ve got programs in place and we know we’ve got to tackle it. I think in the kind of environment where you have slowing growth and lower prices, you need to manage your cost structure and you need to retain your customers.”

Get up to 4.00% interest on your savings without any fees.

Lock in your deposit and earn a guaranteed interest rate of 3.55%.

Earn 3.7% for 7 months on eligible deposits up to $500k. Offer ends June 30, 2025.

MoneySense is an award-winning magazine, helping Canadians navigate money matters since 1999. Our editorial team of trained journalists works closely with leading personal finance experts in Canada. To help you find the best financial products, we compare the offerings from over 12 major institutions, including banks, credit unions and card issuers. Learn more about our advertising and trusted partners.

(All figures in U.S. currency.)

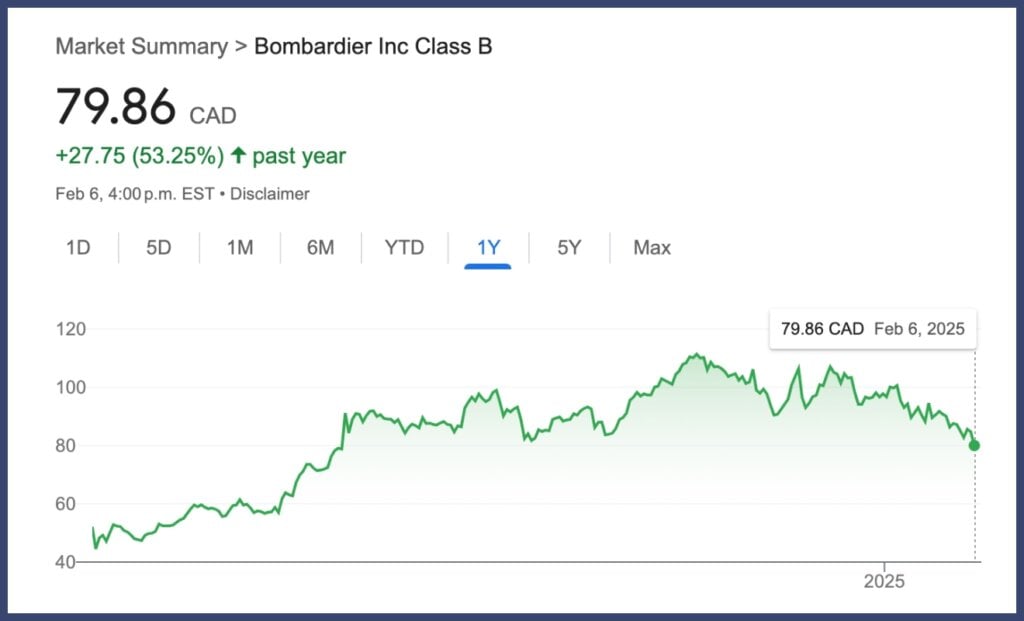

Bombardier Inc. held off on giving investors a financial forecast for the year, citing the uncertainty posed by the Trump administration’s tariff threats that risk knocking the company off course.

Chief executive Éric Martel said he was “very disappointed” the business jet maker could not provide targets.

“We need to exercise caution until we see how this all unfolds,” he told analysts on a conference call Thursday.

“We are still geared up to meet the 2025 objectives,” he added. “But this being said, we still have to be responsible and not provide guidance.”

The move speaks to the massive question mark hovering over aerospace, manufacturing and myriad other industries after U.S. President Donald Trump pledged sweeping 25% duties on Canadian and Mexican imports, then agreed last-minute on Monday to defer them for a month. Prior to the pause, Canada also proposed retaliatory tariffs on $155 billion worth of American goods. (All figures in U.S. currency.)

What happens after the pause is anyone’s guess.

“It’s a lower risk, but it’s still a risk,” Martel said.

The tariffs would pose big problems for Bombardier, which counts more than 2,800 suppliers across 47 states in the U.S.—still its core customer base. American buyers accounted for 63% of its revenue in 2023, analysts said.

Bombardier builds the wings for its ultra-long-range Global 7500 jet just south of Dallas. It transforms Global 6500 jets into military patrol planes in Wichita, Kan.

“The vast majority of our platforms are made up of more U.S. parts and systems than any other country,” Martel said.

“Given the global nature of the aviation manufacturing industry, these proposed tariffs as well as potential reciprocating tariffs could have an enormous impact with many unintended consequences.”

Martel, who took the helm of the company in 2020 when it was struggling under billions of dollars in debt, proceeded to steer the rail and commercial aviation giant through the COVID-19 pandemic and streamline it into a pure-play business jet outfit.

Its adjusted earnings went from $200 million in 2020 to $1.36 billion in 2024. Adjusted profit margins jumped to nearly 16% from 3%.

Faced with a new threat, Martel said the company is “well-equipped” to deal with potential tariffs but declined to detail the contingency plans he said lay at the ready.

“The big question is how long it’s going to last,” he said. “It’s not going to be a crisis overnight.”

Orders for new aircraft continue to roll in at a smart clip. “This includes the U.S. Also worth noting, we have not seen cancellations.”

Bombardier’s book-to-bill—the ratio of orders received to deliveries billed, a key indicator of near-term demand for a company’s products—remained steady at 1.0 last quarter.

Globally, business jet flight volumes in the first five weeks of the year floated 3% above the figure from the same period in 2024, according to industry data firm Wingx Advance.

Bombardier also managed to pay off $400 million in debt last year and boost revenue from services—maintenance and repairs—by 16% over the course of 2024. The services segment now accounts for nearly one-quarter of total revenue, as luxury jet use continues to soar above pre-pandemic levels.

Nonetheless, the lack of a forecast for Bombardier’s fiscal year worried some analysts.

“This could imply that (first-quarter) bookings have been impacted by the tariff threat overhang,” said Desjardins analyst Benoit Poirier in a note to investors Thursday morning.

Bombardier shares have fallen 15% since Trump’s inauguration, including a 5% drop by midday Thursday.

Taking stock of the Canadian aerospace sector, James McGarragle of RBC Dominion Securities cautioned: “We see Bombardier as the most impacted by tariffs, given final completion of its aircraft occurs in Canada.”

The company churned out 57 business jets in its latest quarter, beating last year’s figure by one but falling four planes short of the low end of its full-year forecast range.

On Thursday, Bombardier reported a fourth-quarter profit of $124 million, down 42% from $215 million a year earlier even as revenues crept higher.

The Montreal-based private jet maker, which keeps its books in U.S. dollars, said revenue for the three months ended Dec. 31 rose to $3.11 billion from $3.06 billion in the same period in 2023.

On an adjusted basis, Bombardier increased earnings by 120% to $3.01 per share versus $1.37 per share a year earlier. The result far exceeded analysts’ expectations of $2.01 per share.

Suncor chief executive Rich Kruger says that while all Canadian businesses will feel a hit from tariffs, his company is fairly well-positioned to limit the impact.

He says the company’s large Canadian refining footprint and higher capacity than peers to export crude from the coast makes it less exposed to tariffs compared with some companies more reliant on shipping unrefined heavy crude south of the border.

Kruger says that while he thinks the U.S. needs Suncor just as it needs the U.S. market, the company’s integrated asset base gives it a natural hedge to tariff impacts.

His comments on an earnings call came as Suncor reported a profit of $818 million in the fourth quarter of 2024, down from $2.82 billion a year earlier.

Adjusted operating earnings were $1.57 billion, down from $1.64 billion a year earlier.

Desjardins analyst Chris MacCulloch said in a note that earnings beat expectations even though the company had pre-released most key operational metrics in January.

He says Suncor looks to be a safe harbour in the event of a North American energy trade war given it refines nearly half of corporate production within Canada.

(All figures in U.S. currency)

Thomson Reuters raised its dividend 10% as it reported a fourth-quarter profit of $587 million. (All figures in U.S. currency.)

The company, which keeps its books in U.S. dollars, says it will now pay a quarterly dividend of 59.5 cents per share, up from 54 cents.

The increased payment to shareholders came as Thomson Reuters says its profit for the quarter ended Dec. 31 amounted to $1.30 per diluted per share compared with a profit of $678 million or $1.49 per diluted share a year earlier.

Revenue for the quarter totalled $1.91 billion, up from $1.82 billion in the last three months of 2023.

On an adjusted basis, Thomson Reuters says it earned $1.01 per share in its latest quarter, up from an adjusted profit of 98 cents per share a year ago.

Analysts on average had expected an adjusted profit of 96 cents per share, according to estimates compiled by LSEG Data & Analytics.

Eli Lilly’s profit doubled in the fourth quarter, propelled by its hot-selling diabetes and obesity treatments, and the drugmaker came out with a mostly better-than-expected 2025 forecast.

Sales of Lilly’s top-selling product, the diabetes treatment Mounjaro, jumped 60% to $3.53 billion in the final quarter of 2024 while its obesity treatment counterpart Zepbound brought in $1.9 billion. Both figures fell short of expectations on Wall Street but reflect a forecast Lilly made last month.

Revenue from the breast cancer treatment Verzenio also helped in the fourth quarter, climbing 36% to $1.55 billion.

Overall, Lilly’s quarterly profit swelled to $4.41 billion. Revenue advanced 45% to $13.53 billion, in line with expectations. Per-share earnings adjusted for one-time items totalled $5.32, easily topping the $5.01 that Wall Street was looking for, according to a poll of industry analysts by FactSet.

Mounjaro and Zepbound are part of a wave of diabetes and obesity medications known as GLP-1 receptor agonists that are soaring in popularity globally due to the amount of weight people lose while taking the injections. They compete with Ozempic and Wegovy from the Danish drugmaker Novo Nordisk, which also reported strong sales growth on Wednesday.

For 2024, Mounjaro sales more than doubled to $11.54 billion, while Zepbound notched sales of $4.9 billion in its first full year on the market.

Analysts expect more than $18 billion in sales from Mounjaro this year and over $10 billion from Zepbound, which was recently approved in the United States as a treatment for some forms of sleep apnea.

Additional approvals like that and Lilly’s push to increase manufacturing should lead to ongoing, solid growth for the drugs, Edward Jones analyst John Boylan said in a research note.

For 2025, the Indianapolis drugmaker expects adjusted earnings to range between $22.50 and $24 with revenue falling between $58 billion and $61 billion.

Analysts expect earnings of $22.77 per share on $58.8 billion in revenue.

Eli Lilly and Co. shares climbed about 2% Thursday morning to $857.40 while broader trading indexes started the day mixed.

Lilly’s stock has already climbed 9% so far this year, as of Wednesday.

(All figures in U.S. currency)

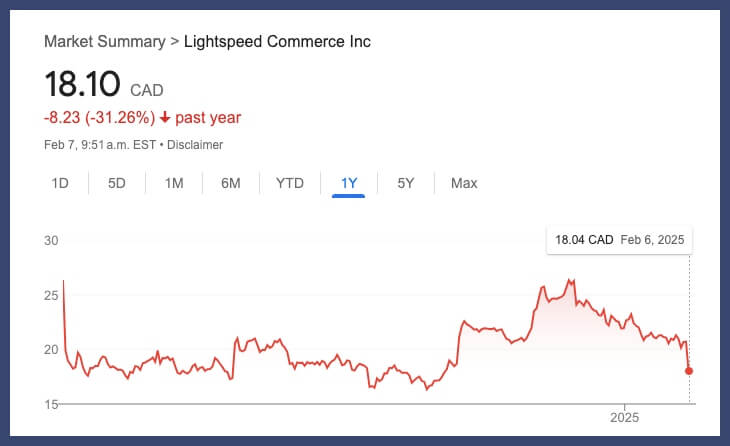

Lightspeed Commerce Inc.’s share price fell almost 18% after the company concluded a strategic review that did not result in a go-private deal.

Instead, the company revealed it would remain public after it said the review revealed a “high level of interest” in the tech firm.

The outcome and a decision from the Montreal-based payments software company to stick with its focus on growing its North American retail and European hospitality businesses left its share price sitting at $17.10 by mid-afternoon Thursday.

Announcing the choices earlier in the day, board chair Patrick Pichette said staying public was a “unanimous” decision that offers “the best available path to maximize value for the company and its shareholders.”

Lightspeed launched the review last year, prompting speculation of a possible sale of the firm, after founder Dax Dasilva returned to lead the company with a promise to return it to profitability.

Dasilva wouldn’t say much Thursday about any offers Lightspeed may have garnered.

“We’re not going into the details of the process, unfortunately, but yes, we had strong engagement and we did have extensive discussions with several participants in the process,” he told analysts.

“Ultimately we determined and concluded that the best way to drive maximum shareholder value is to continue as a public company and execute our transformation plan in that context.”

The end of the review came as Dasilva nears the one-year anniversary of his return to the company. The Lightspeed founder handed off the top job to JP Chauvet in February 2022 but returned to the CEO role on an interim basis in February 2024.

Dasilva was reappointed on a permanent basis in May.

Much of his work since then has been focused on finding cost efficiencies and appeasing shareholders.

He announced Thursday that the company would use a buyback program to return up to $400 million in cash to shareholders.

The move comes after Lightspeed cut about 200 jobs in December and about 280 jobs in April, when it shifted its sales summit from an in-person format to a virtual event and decreased the number of days staff work from the office to reduce bills associated with feeding employees.

However, the company, which keeps its books in U.S. dollars, said Thursday that it experienced a loss of $26.6 million or 17 cents per share for the quarter ended Dec. 31. The result compared with a loss of $40.2 million or 26 cents per share a year earlier. (All figures in U.S. currency.)

Revenue for what was the company’s third quarter totalled $280.1 million, up from $239.7 million a year ago.

On an adjusted basis, Lightspeed says it earned 12 cents per share in its latest quarter compared with an adjusted profit of eight cents per share a year earlier.

The quarter covers a period when the company was deep into its five-month strategic review.

The process looked at the company’s portfolio but also its market attractiveness and competitive dynamics, Dasilva said.

He added the review had no “presupposed outcome.”

“We wanted to know what were the options available (and) what were the different alternatives, but the object is how can we best execute the transformation plan and drive the most value?” he told analysts.

“After assessing multiple options, we concluded with our board that continuing as a public company offers the best path to maximizing value.”

National Bank of Canada analyst Richard Tse said the conclusion of the review was “by far the most notable” part of Lightspeed’s announcements Thursday.

“No doubt, the outcome of the strategic review likely raises questions as to why it did not conclude in a sale—most notable and obvious are a price (valuation) and product disconnect from the vantage point of prospects,” he wrote in a note to investors.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Here’s how proposals from the NDP, Liberals, Conservatives and Green Party could affect your cash flow—and maybe help decide...

Cineplex records fewer moviegoers, Roots skates by tariffs, and Delta Air Lines scratches guidance for the year. Here are...

Young investors have many ways to build the fixed-income portion of their portfolios. Experts say to keep these two...

Shaken by recent stock-market losses? Investing experts weigh in on how Canadians can stick with their retirement plans when...

What to consider when deciding to incorporate a company with friends to buy real estate and more.

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Tariffs tough but “manageable” for Dollarama, automaker Stellantis shuts Canadian plant (for now), and more. Here are the details...

Many industries in Canada will struggle to adapt to the trade war, experts say.

From severing ties and becoming a non-resident to learning about departure and withholding taxes, here’s what expats can expect...