Are you ready for the Hot Potato?

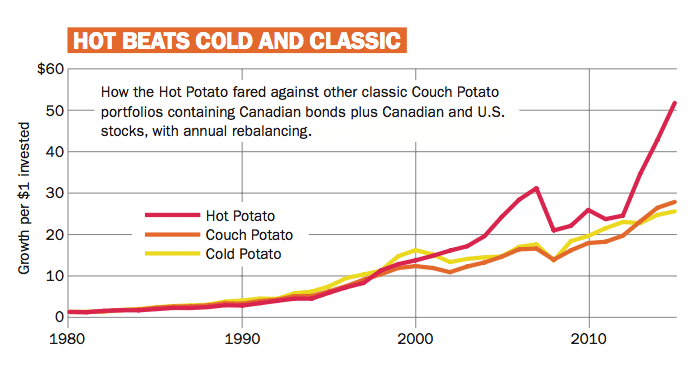

Love the steady returns of the classic Couch Potato strategy? This spicier version beat it by 6.7 percentage points annually. It’s hot stuff

Advertisement

Love the steady returns of the classic Couch Potato strategy? This spicier version beat it by 6.7 percentage points annually. It’s hot stuff

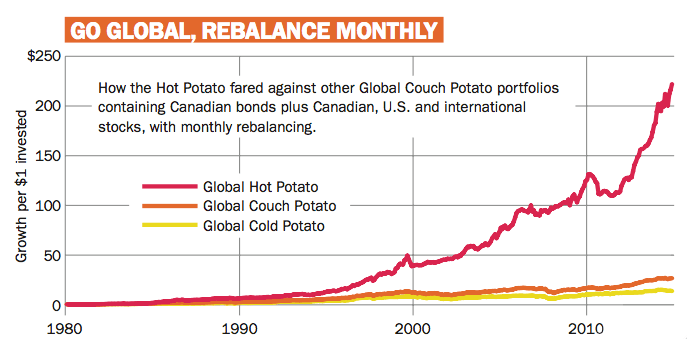

The Global Hot Potato portfolio, rebalanced monthly, gained an average of 16.7% per year from the start of 1981 to the end of 2015. It beat the classic Couch Potato by a whopping 6.7 percentage points annually.

While the global version of the Hot Potato was certainly more volatile than the Couch Potato, it came mostly from the sort of upside volatility that few investors complain about. In addition, it nimbly sidestepped several market crashes along the way. In fact, the largest drawdown for the monthly-balanced Global Hot Potato came after the Internet bubble popped in 2000, when it declined 21.4%. But it bounced back almost two years before the Global Couch Potato did, having fallen 29.2% during the same downturn.

The Global Couch Potato drew its biggest loss during the 2008 collapse (31.1%) and didn’t recover until 2011. Its spicier sibling fared better because it was invested in bonds for a good part of that period: It fell only 10% from its 2007 high to its 2008 low, and had recovered fully by the summer of 2009.

Once again contrarians fared poorly. The Global Cold Potato Portfolio is moved monthly into the worst performing asset class of the prior year. By doing so, it gained an average of 7.9% annually and trailed the Global Couch Potato by 2.1 percentage points per year. The monthly return history of all three global potato variants is shown in the charts on the opposite page.

The Global Hot Potato portfolio, rebalanced monthly, gained an average of 16.7% per year from the start of 1981 to the end of 2015. It beat the classic Couch Potato by a whopping 6.7 percentage points annually.

While the global version of the Hot Potato was certainly more volatile than the Couch Potato, it came mostly from the sort of upside volatility that few investors complain about. In addition, it nimbly sidestepped several market crashes along the way. In fact, the largest drawdown for the monthly-balanced Global Hot Potato came after the Internet bubble popped in 2000, when it declined 21.4%. But it bounced back almost two years before the Global Couch Potato did, having fallen 29.2% during the same downturn.

The Global Couch Potato drew its biggest loss during the 2008 collapse (31.1%) and didn’t recover until 2011. Its spicier sibling fared better because it was invested in bonds for a good part of that period: It fell only 10% from its 2007 high to its 2008 low, and had recovered fully by the summer of 2009.

Once again contrarians fared poorly. The Global Cold Potato Portfolio is moved monthly into the worst performing asset class of the prior year. By doing so, it gained an average of 7.9% annually and trailed the Global Couch Potato by 2.1 percentage points per year. The monthly return history of all three global potato variants is shown in the charts on the opposite page.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Gildan Activewear also reported earnings this week. Here are the details for Canadian investors.

Energy, resource and innovation companies topped the TSX Venture 50 list in 2024, the latest edition of the ranking...

Concerned about the heavy tech weighting in U.S. stock indexes? Explore ETF alternatives for balanced exposure to U.S. equities.

Find out which Canadian robo-advisors offer the lowest fees, best support, top returns, and more, with MoneySense’s 2025 guide.

Restaurant Brands International, McDonald’s and Canadian Tire Corp. also reported earnings this week. Here are the details for Canadian...

Canadians now have three zero-commission brokerage options, including Questrade, to trade stocks and ETFs.

Eli Lilly, BCE, Suncor, Canada Goose, Bombardier, Thomson Reuters and Lightspeed reported earnings this week. Here are the details...

Ottawa defers effective date of capital gains changes to 2026 and promises exemptions for the tax inclusion increase.

Tech industry watchers believe the startup’s success could signal greater competition for the U.S. companies at the forefront of...

This is our list of the top dividend stocks for 2025. Use our ranking as a tool to help...