TFSAs for retirees

TFSAs let you hang on to more of your hard-earned savings in your golden years

Advertisement

TFSAs let you hang on to more of your hard-earned savings in your golden years

Heidi Shearman and Michael Slark are within shouting distance of retirement. Although they’re both just 56, they believe they can leave the workforce in about four years. Shearman is looking forward to getting her hands dirty in the garden of their home in Prince George, B.C. Slark, who survived a life-threatening illness in 2008, will have more time to devote to his hobby: collecting comic books, graphic novels and science fiction. And their TFSAs are taking centre stage in their retirement plan.

Having spent many years in the financial industry, Heidi always knew the importance of saving for retirement. “While I was working full-time I contributed to my RRSP, though we weren’t able to max out,” she says. But Heidi left the workforce in 2007 to care for her mother, who was in the final stages of cancer, and since then she’s worked a series of part-time jobs, including her current role at the electricity and gas utility FortisBC. With her lower income, the RRSP has now lost much of its appeal. “The TFSA is definitely a better option for my situation,” she says.

STOP CLAWBACKS

Michael, a grade 5 teacher, still contributes to a spousal RRSP in Heidi’s name. But these days his TFSA is just as important. The couple is working with a financial planner who advised them that the combination of government benefits, RRSP withdrawals and pension income could push him into a higher tax bracket during retirement. So Michael no longer makes contributions to his own RRSP and has maxed out his TFSA instead. With more of his savings now going to TFSAs, the higher contribution limit has made the account even more important to the couple’s retirement plan.

Right now the couple is using their TFSAs for different purposes. Heidi’s holds a ladder of cashable GICs they’ve earmarked for emergencies, while Michael’s holds a portfolio of stock and bond ETFs that form part of their retirement nest egg. Once they’re retired, Heidi says she plans to cash in the GICs and use her TFSA for long-term savings as well, since she knows that higher-growth investments such as equity ETFs will let her take full advantage of the tax shelter.

SHELTER SURPLUS INCOME

For younger people, the TFSA’s value comes from the large amount of contribution room they can accumulate over decades of saving. But for those who are nearing retirement or already there, the TFSA’s role is usually different. If you’ve already built a large portfolio after decades of saving in RRSPs and non-registered accounts, your TFSA will likely not be a large portion of your net worth. But it can still be a useful tool: as you draw down those RRSPs during retirement, you can use your TFSAs to shelter surplus income and grow your wealth tax-free.

Consider too that once you reach your early 70s, the TFSA is your only opportunity to tax-shelter any new savings, since you can no longer contribute to an RRSP after the end of the year you turn 71. If you’re planning to work part-time after stepping away from your career, that’s an important benefit. Gordon Pape, author of Tax-Free Savings Accounts: How TFSAs Can Make You Rich, says the higher limit makes TFSAs particularly attractive to teachers, police officers and public servants who plan to keep earning income while collecting their pensions.

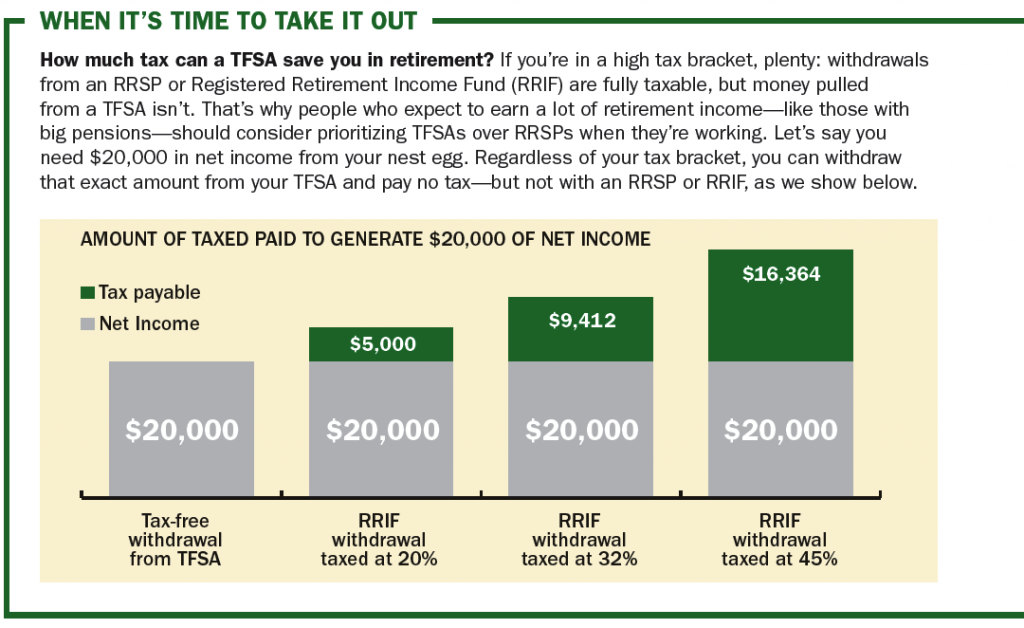

Even if they’re not earning any employment income, many Canadians over this age have a surplus after collecting Canada Pension Plan (CPP) benefits, Old Age Security (OAS) and employer pensions. Moreover, some are forced to withdraw more than they need from their Registered Retirement Income Fund (RRIF): the minimum withdrawal rate now starts at 5.28% and increases every year. For example, a 75-year-old with a $300,000 RRIF would need to withdraw $17,460 and report it as income. “It’s frustrating for people who have RRIFs to be taking money out and paying tax on it when they don’t need it all,” said Rona Birenbaum, a financial planner with Caring for Clients in Toronto. The silver lining is that retirees can use those excess withdrawals to top up their TFSAs.

PROTECT YOUR LEGACY

Birenbaum also says the TFSA can be a useful estate-planning tool. Many older Canadians are concerned about the tax consequences of passing away with large retirement accounts, since the full balance of RRSPs and RRIFs must be reported as income on your final tax return (unless you have a spouse who is the beneficiary). If the account is large, you could end up giving close to 50% to the taxman.

One potential solution is to make additional RRIF withdrawals during retirement, paying tax at a lower rate, and use the net amount to make your TFSA contribution for the year. For example, if your tax rate in retirement is 30%, you could withdraw an additional $14,286 from your RRIF, which would leave you with $10,000 after taxes—enough to max out your TFSA for the year. That money would grow tax-free for the rest of your life, and it wouldn’t be taxable to your estate, so more of your wealth will go to your children or your favourite charity.

If you have a spouse, make sure you name each other the “successor holders” of your TFSAs. That way when you pass away your spouse effectively becomes the new account holder, and the TFSA will retain its tax-free status. Note that only a spouse can be your successor holder: if you want a child or other heir to receive your assets, they must be named as the beneficiary. They’ll receive TFSA assets tax-free from your estate, but any future investment gains will be taxable.

As always, consult with a financial or estate planner when making important decisions like these. Smart planning will help you use the TFSA to preserve the wealth you’ve worked so hard to build and ensure it ends up in the hands of the people you care about.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Find out which Canadian robo-advisors offer the lowest fees, best support, top returns, and more, with MoneySense’s 2025 guide.

What to consider when deciding to incorporate a company with friends to buy real estate and more.

From severing ties and becoming a non-resident to learning about departure and withholding taxes, here’s what expats can expect...

In this excerpt from her new book, Making Bank, Shannon Lee Simmons guides young Canadians (and their parents) through...

There’s more than one way to optimize your income after retiring. Some strategies can boost wealth, and others may...

Are unpredictable markets stressing you out? Two investing experts weigh in on how young Canadians can deal with the...

RRSP contributions can reduce capital gains tax. How does that work, and when might a different tax strategy be...

Broad bond index ETFs haven’t always been there for investors in the past. Here’s a safer alternative if you’re...

The tour company, grocer and steel maker are feeling the effects of U.S. tariffs. Here are the details for...

I WOULD like some info on where to invest TFSA

The initial paragraph is wrong, so this draws the authors’ credibility into repute.

“Michael and Heidi are using a mix of TFSAs and RRSPs to shelter their savings.” This is completely false, as the TFSA operates differently than an RRSP. An RRSP is an investment instrument that lets you defer taxes from income earned, as well as from any monies that is generated, e.g. interest, capital gains, etc. This money will be taxed as income when a withdrawal is made.

What makes a TFSA NOT a “tax shelter” is that the money put into it will already have been taxed. Plus, whatever monies that are withdrawn later will not be taxed.

@Doreen Savoie:

You can invest at any financial institute, either through an advisor or by yourself. If you want to know what to invest in, you can seek the advice from an advisor or accountant.