Retirement portfolio: A Goldilocks strategy

A fixed income and equities mix that’s just right for your retirement portfolio

Advertisement

A fixed income and equities mix that’s just right for your retirement portfolio

![Portfolio_Builder_banner_1256X300[2][2][2]](https://www.moneysense.ca/wp-content/uploads/2016/05/Portfolio_Builder_banner_1256X300222.jpeg)

It’s a tough time to be an income investor. Bond yields are dismal. The dividend yield on stocks is better, but it’s come down as stock prices have climbed in the last few years. (The yield on the S&P 500 is now under 2%.) And the prospect of rising interest rates threatens to give your portfolio a painful kick on the way up. That’s because it would cause bonds—and maybe even high-yield stocks—to fall in value.

So what’s an income investor to do? You’re probably tempted to look for higher yields wherever you can find them, but the risks from doing so are high. “Income investors are starved for yield,” says Christopher Davis, director of fund analysis at Morningstar Canada. “Some are chasing yield, but that scenario can end very badly.”

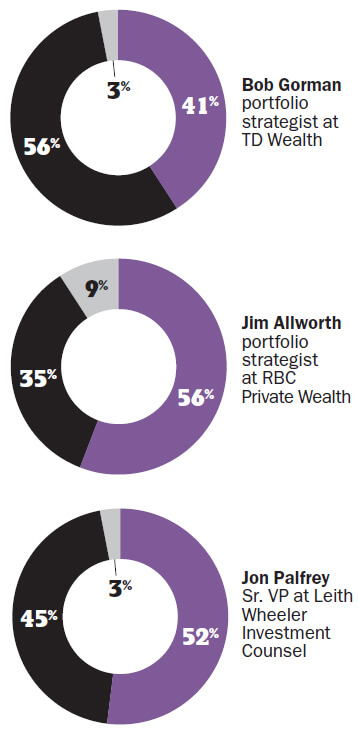

If you’re moderately conservative, you may be better off going for less yield and a little more safety, as hard as that may be to stomach. In bonds, that means going for shorter terms and higher quality, while paring back on those with high yield but high risk. In equities, it means tilting your portfolio in favour of dividend growth stocks instead of high dividend payers, which are more sensitive to rising rates. Call it “the Goldilocks approach,” in the words of RBC Wealth Management portfolio strategist Jim Allworth. Here’s how to find the right balance in your income portfolio.

You’re no doubt aware that central banks have been suppressing interest rates during the last several years in order to foster economic recovery. But with an improving economy, these policies are starting to reverse. In particular, the U.S. Federal Reserve has already started to “taper” its massive purchases of mortgages and bonds and is expected to end them outright later this year. That should result in long-term bond rates returning to more normal levels. The Fed is also expected to raise short-term rates gradually in 2015. It’s unclear how far rates will rise, and how fast—that depends in part on whether inflation stays dormant or picks up. But it’s likely you’ll see at least modest increases, starting with longer terms this year, followed by shorter-term rates as well.

This “normalization” should be good for investors in the long run, because any new money added to fixed-income portfolios should earn higher yields going forward. But there could be a painful adjustment process for investors. Interest rates and bond prices are like two ends of a teeter-totter: as rates rise, the price of existing bonds in your portfolio will fall. So you need to limit this damage while looking forward to benefitting eventually from better yields.

There are two ways bond investors can receive higher yields: one is going with longer terms; the other is taking more credit risk. Right now, however, those are precisely the strategies you should avoid, says Hank Cunningham, fixed-income strategist at Odlum Brown Ltd. and author of In Your Best Interest. “Two pieces of advice are paramount to any investor in fixed income these days: avoid long-term securities and avoid low-quality securities.”

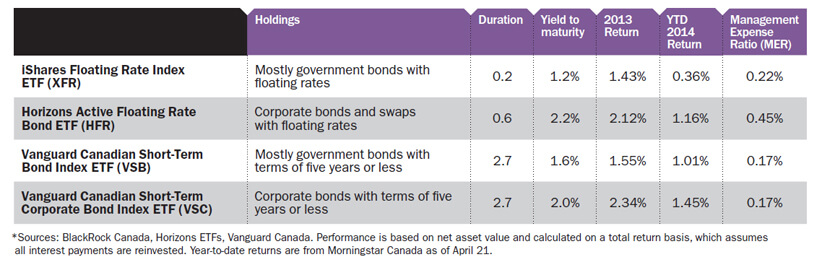

Let’s look at the reasons for this advice. A bond’s sensitivity to interest rates is measured by what’s called “duration.” The iShares Canadian Universe Bond Index ETF (XBB), which tracks the overall Canadian investment-grade bond market, has a duration of 6.9. That means if interest rates rise across the board one percentage point, the ETF’s value should fall by roughly 6.9%.

Duration increases with a bond’s term to maturity, so long-term bonds will fall in price more sharply when interest rates rise. Clearly, you should avoid them if you think rates will climb. Many investment managers have lowered the average duration of their fixed-income investments well below that of the overall bond market. For example, Leith Wheeler Investment Counsel targets a duration around four, says senior vice-president Jon Palfrey.

The advice on avoiding high-yield debt needs more explanation, because bonds with high payouts are not especially sensitive to interest rate movements. However, many experts feel yields on “junk bonds” don’t justify the risk at this time. High-yield bonds need to pay more than safer alternatives to compensate for the greater likelihood of default. But the boom in equity markets has driven down their “spread” over government bonds to the lowest level since before the 2008–09 financial crisis. Some bond issuers have watered down covenants designed to protect investors if these investments get into trouble. “The high-yield market is pricing in pretty high expectations for credit quality,” says Bob Gorman, portfolio strategist at TD Wealth. “We think the return versus the risk is not great, so we don’t have high-yield bonds at this point.”

A second reason to be cautious about high-yield bonds is that they don’t provide much stability in a portfolio when you’re likely to need it most. Investment-grade bonds may have paltry yields, but generally hold their value when stocks get hammered—indeed, they may rise in value as investors flee to safety and drive interest rates down. Meanwhile, high-yield bonds tend to suffer along with stocks. “Our biggest problem with high-yield debt is it’s much more highly correlated to the stock market than it is to fixed income,” says Allworth. “Yet for many people, the fixed-income part is intended to be the non-volatile, certain part of their portfolio.”

How do you put these ideas into practice? Do-it-yourself investors might consider switching some of their fixed-income money into short-term or floating-rate bond ETFs, while ensuring they stick with investment-grade securities. One of several such funds is the Horizons Active Floating Rate Bond ETF (HFR), Morningstar’s Best Fixed Income ETF of 2013. (See “Shortening Up on Bonds” on the next page for others.) As their name suggests, floating-rate bonds have variable coupons, and actually benefit from rising rates. HFR managed to eke out a 2013 return of 2.12%, while many longer-term bond funds had small losses last year. It has a duration of just 0.6 and holds investment-grade corporate securities. (By contrast, some floating-rate mutual funds are choked to the gills with high-yield debt, and they may downplay the risks in their marketing materials. Make sure you understand the credit quality of what you’re buying.)

Another popular strategy for controlling both interest-rate and credit risk is to maintain a ladder of high-quality bonds or GIC rates. You could allocate equal portions to terms of one to five years and hold each component to maturity. That ensures you’ll get your principal back regardless of interest rate movements, plus a steady stream of predictable income. If rates rise, income gradually rises as bonds or GICs mature and new ones are added at higher rates.

When it comes to the equity side of a portfolio, you’ve probably long appreciated the value of stocks that throw off reliable dividends. But these days there’s an adjustment to consider. “It’s important to emphasize dividend growth as opposed to dividend yield,” says Gorman. He recommends shifting into dividend growth stocks—with moderate but rising dividends—and out of stocks with less growth that pay higher dividends. Stocks in general aren’t too sensitive to modest increases in interest rates when investors are confident the economy will do well. But high-dividend stocks with modest growth in sectors like utilities, telecoms and REITs tend to be more strongly impacted. That happened in 2013, when long-term interest rates rose and many such stocks were hit hard. “Investing based on yield will likely give you more risk in a rising interest rate environment,” says Palfrey.

By contrast, dividend growth stocks come from many sectors and are likely to be less affected by rising rates. This group includes stocks with good growth prospects but dividend yields as low as 2% or 3%. At the higher end of the spectrum, many experts include Canadian bank stocks yielding around 4%. No ETF or mutual fund focuses entirely on this strategy using Canadian stocks, but the Vanguard Dividend Appreciation ETF does this with U.S. stocks (ticker is VIG on the New York Stock Exchange, VGG in Canada, or VGH for the version hedged to Canadian dollars).

Companies with capacity to grow dividends in the future are not always those that have done it in the past. Start by looking for a healthy earnings yield (earnings per share divided by stock price), says Allworth of RBC. An average blue-chip company (represented by the S&P 500) has an earnings yield around 6%, he notes. It pays out only one third in dividends, resulting in a 2% yield, with the rest re-invested in the business. There it typically earns 8% to 14% per year. That return is higher than you can expect to earn investing on your own, and sets the stage for healthy future dividend increases. Says Allworth: “I’d rather take a little less now with the promise of a lot more later.”

Yield-hungry investors may be inclined to turn their noses up at companies paying only 2% or 3%. But if you’re patient, a dividend growing at 8% a year doubles in nine years. A rising dividend that eventually becomes quite large in relation to your original investment may be most relevant if you’re a buy-and-hold investor patiently focused on income. But you can also expect reasonably steady capital gains and a rising share price, which is most relevant if you sell the stock or are more focused on the overall value of your portfolio. “You can get a higher stream of income that grows, capital appreciation, good total returns, with muted volatility,” Gorman says.

Dividend-paying companies in Canada have performed well in recent decades, but dividend growth companies have done even better. Dividend-paying stocks in the TSX composite index achieved an annual compounded return of 10.4% since 1986, outperforming the overall composite by 3.7 percentage points, according to a study by RBC Capital Markets Quantitative Research. But dividend growth stocks beat the more general dividend category by 1.8 percentage points, the research found.

Dividends from Canadian companies are taxed at a lower rate than dividends paid by foreign firms, and they carry no currency risk. On the other hand, the Canadian stock market is a tiny portion of global markets and skewed to financials and resources. There is an enormous diversification benefit from investing in U.S. and international markets, especially in sectors poorly represented in Canada. Many wealth managers suggest investors keep 40% to 70% of their equity portfolios in foreign stocks. Others, like Allworth, downplay geography, preferring to focus on finding “good companies at good prices” that provide a balance of sectors.

You still have to find the right balance between fixed income and equities. Lately, experts are tilting portfolios more towards cash or equities and away from bonds.

But there’s a role for both equity and fixed income. A healthy dollop of investment-grade fixed income that isn’t overly sensitive to interest rates helps produce reliable income and keeps portfolio values stable. Adding dividend growth stocks should boost your income and provide more potential for growth. In the end, a “Goldilocks” strategy may not give you as much income as you’d like, but you’ll probably feel much more comfortable should conditions turn bearish.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Some Canadian seniors enter retirement without savings or run out of money over time. Here’s how they can stay...

Here’s how proposals from the NDP, Liberals, Conservatives and Green Party could affect your cash flow—and maybe help decide...

Yes, your estate will pay a high rate of tax on your RRIF when you die. But it usually...

Here’s why you might see an RRSP deduction limit on your notice of assessment, even when you’ve already converted...

Find out which Canadian robo-advisors offer the lowest fees, best support, top returns, and more, with MoneySense’s 2025 guide.

Once you start RRIFing, how do you make sure you have enough cash, and should you dial down risk?

Here’s how Canada’s Old Age Security pension works, who’s eligible for OAS, when you can start receiving OAS, and...

Here’s how Canada’s retirement pension plan works, who’s eligible for CPP, when you can start receiving CPP, and CPP...

There’s more than one way to optimize your income after retiring. Some strategies can boost wealth, and others may...