Downsizing: Go small, think big

Downsizing in retirement can add a sizeable chunk of income to your nest egg, paving the way for more security and enjoyment in your golden years

Advertisement

Downsizing in retirement can add a sizeable chunk of income to your nest egg, paving the way for more security and enjoyment in your golden years

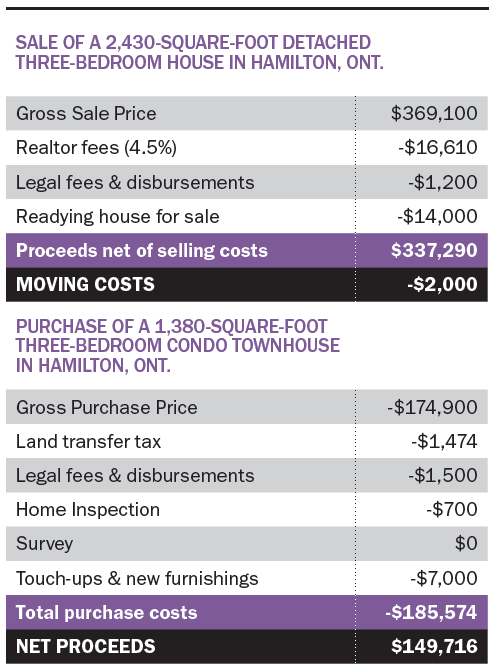

Notes: Prepared with the assistance of Melanie Reuter, Elizabeth Campbell and Don Campbell of the Real Estate Investment Network. Gross sale price, gross purchase price and land transfer tax are taken from actual recent real estate transactions in Hamilton, Ont. (In this case, the seller of the house and buyer of the townhouse are not the same.) The other figures are estimates. Realtor fees can vary from 2.5% to 6%. Money spent on readying house for sale as well as touch-ups and new furnishings will vary widely. Buyer is often required to commission a survey by the mortgage lender if the seller can’t produce one done fairly recently. In this case we’ve assumed no new survey is required. Land transfer taxes vary widely across Canada but most provinces have them. Purchase of a newly constructed home would be subject to additional costs, particularly GST. In this case, both properties are resales and not subject to GST.

Notes: Prepared with the assistance of Melanie Reuter, Elizabeth Campbell and Don Campbell of the Real Estate Investment Network. Gross sale price, gross purchase price and land transfer tax are taken from actual recent real estate transactions in Hamilton, Ont. (In this case, the seller of the house and buyer of the townhouse are not the same.) The other figures are estimates. Realtor fees can vary from 2.5% to 6%. Money spent on readying house for sale as well as touch-ups and new furnishings will vary widely. Buyer is often required to commission a survey by the mortgage lender if the seller can’t produce one done fairly recently. In this case we’ve assumed no new survey is required. Land transfer taxes vary widely across Canada but most provinces have them. Purchase of a newly constructed home would be subject to additional costs, particularly GST. In this case, both properties are resales and not subject to GST.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Canadians must begin taking RRIF withdrawals the year after converting an RRSP. What happens if you convert only part...

A Certified Financial Planner looks at the different strategies to ask your own advisor: Is life insurance the answer?

Here’s how Canada’s retirement pension plan works, who’s eligible for CPP, when you can start receiving CPP, and CPP...

Here’s how Canada’s Old Age Security pension works, who’s eligible for OAS, when you can start receiving OAS, and...

Find out which Canadian robo-advisors offer the lowest fees, best support, top returns, and more, with MoneySense’s 2025 guide.

Canadians now have three zero-commission brokerage options, including Questrade, to trade stocks and ETFs.

Inflation prices jumped to 0.5% from January to December, which was the largest increase since August 2023.

In this excerpt from Wealthier, authors Daniel R. Solin and Mark McGrath offer practical tips on estate and financial...

To minimize taxes and maximize benefits, learn the difference between deductions, credits and other forms of tax relief by...

Ottawa defers effective date of capital gains changes to 2026 and promises exemptions for the tax inclusion increase.