Perfect advisor for your financial planning needs

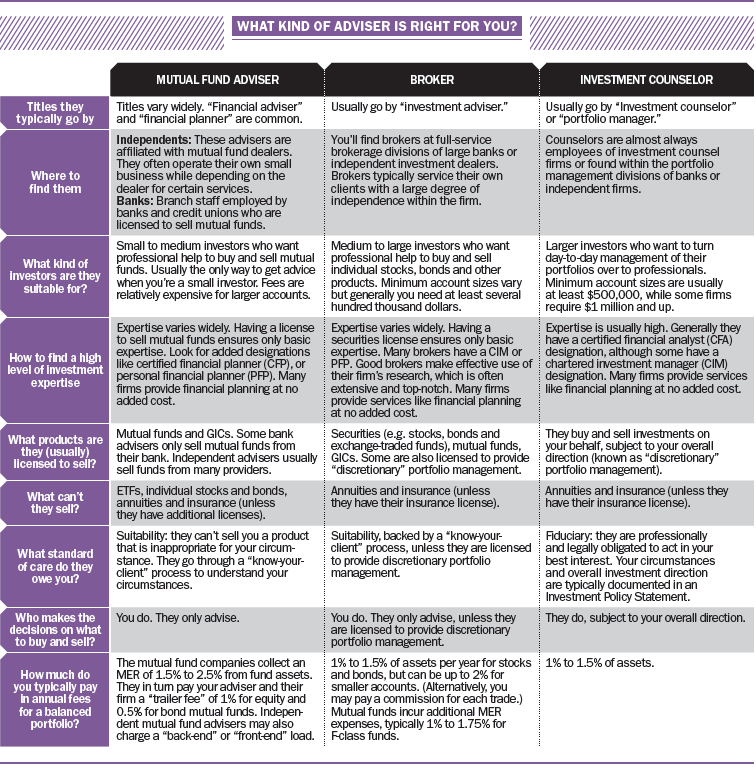

There are three main types of advisors—here's what you need to know to pick the right one

Advertisement

There are three main types of advisors—here's what you need to know to pick the right one

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Maxing out employer contributions is an easy way to boost your retirement savings. Here’s how to do it without...

Some Canadian seniors enter retirement without savings or run out of money over time. Here’s how they can stay...

Here’s how proposals from the NDP, Liberals, Conservatives and Green Party could affect your cash flow—and maybe help decide...

Yes, your estate will pay a high rate of tax on your RRIF when you die. But it usually...

Here’s why you might see an RRSP deduction limit on your notice of assessment, even when you’ve already converted...

Find out which Canadian robo-advisors offer the lowest fees, best support, top returns, and more, with MoneySense’s 2025 guide.

Once you start RRIFing, how do you make sure you have enough cash, and should you dial down risk?

Here’s how Canada’s Old Age Security pension works, who’s eligible for OAS, when you can start receiving OAS, and...

Here’s how Canada’s retirement pension plan works, who’s eligible for CPP, when you can start receiving CPP, and CPP...

There’s more than one way to optimize your income after retiring. Some strategies can boost wealth, and others may...