What are the tax rules for LIRAs?

You can convert it into a LIF or an annuity

Advertisement

You can convert it into a LIF or an annuity

Q: My LIRA is currently valued at $48,000. I am 49 years of age. I am employed part time, with low annual income of about $10,000, but we don’t anticipate needing the money until age 65 to 70. I have always assumed that any investments that can be held in an RRSP can also be held in a LIRA. I am now concerned that this may not be the case. I am also unclear as to how I will access this money in the future. What are the taxation rules and can I switch to an annuity at any time without being taxed?

—Claudia

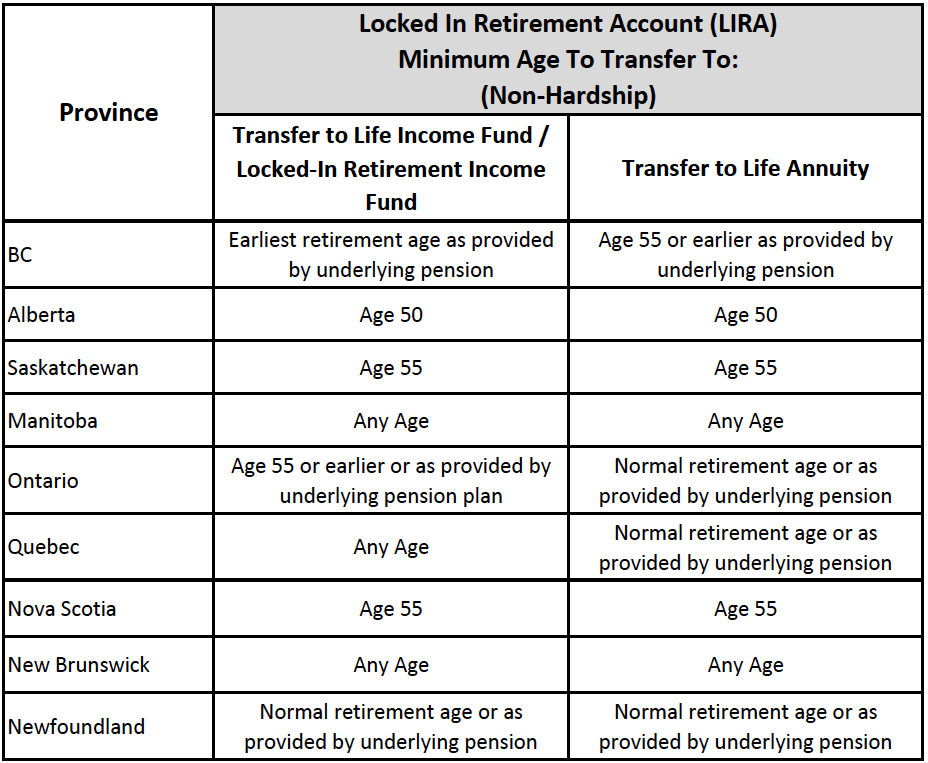

A: Let’s start with what a LIRA is. A LIRA or Locked-In Retirement Account is an RRSP with restrictions on the use of the funds to ensure it is used for lifetime retirement income. It falls under pension legislation which varies from province to province. Typically the earliest you can withdraw funds from a LIRA is age 55 and it must be rolled into a Life Income Fund (LIF) or used to purchase a life annuity.

Claudia can invest within the LIRA as if it is an RRSP. Choose a mix of investments that are moderate to aggressive given the 15+ years ahead. The funds grow until Claudia decides to convert to either a LIF or Annuity (after age 55) to begin her retirement income.

The age at which to start taking the funds as income needs to be assessed in the context of Claudia’s overall financial resources, her retirement income expectations, and health/longevity. It seems reasonable to wait until age 65 to 70.

Income sourced from LIRA funds is taxable whether it is moved to a LIF or used to purchase a Life Annuity. Tax payable is minimized by drawing the income slowly over many years. A prescribed life annuity further spreads the associated tax payable evenly until end of life.

Funds in a LIF can be used to purchase a Life Annuity. I generally suggest converting a LIRA to a LIF initially and then later purchasing a life annuity. The older you are the more mortality credits you have (less years left to live) so the insurance company will offer a higher monthly annuity income.

Q: My LIRA is currently valued at $48,000. I am 49 years of age. I am employed part time, with low annual income of about $10,000, but we don’t anticipate needing the money until age 65 to 70. I have always assumed that any investments that can be held in an RRSP can also be held in a LIRA. I am now concerned that this may not be the case. I am also unclear as to how I will access this money in the future. What are the taxation rules and can I switch to an annuity at any time without being taxed?

—Claudia

A: Let’s start with what a LIRA is. A LIRA or Locked-In Retirement Account is an RRSP with restrictions on the use of the funds to ensure it is used for lifetime retirement income. It falls under pension legislation which varies from province to province. Typically the earliest you can withdraw funds from a LIRA is age 55 and it must be rolled into a Life Income Fund (LIF) or used to purchase a life annuity.

Claudia can invest within the LIRA as if it is an RRSP. Choose a mix of investments that are moderate to aggressive given the 15+ years ahead. The funds grow until Claudia decides to convert to either a LIF or Annuity (after age 55) to begin her retirement income.

The age at which to start taking the funds as income needs to be assessed in the context of Claudia’s overall financial resources, her retirement income expectations, and health/longevity. It seems reasonable to wait until age 65 to 70.

Income sourced from LIRA funds is taxable whether it is moved to a LIF or used to purchase a Life Annuity. Tax payable is minimized by drawing the income slowly over many years. A prescribed life annuity further spreads the associated tax payable evenly until end of life.

Funds in a LIF can be used to purchase a Life Annuity. I generally suggest converting a LIRA to a LIF initially and then later purchasing a life annuity. The older you are the more mortality credits you have (less years left to live) so the insurance company will offer a higher monthly annuity income.

Ask a Retirement Expert: Leave your question for Tom Feigs »

Tom Feigs is a fee-for-service financial planner, money coach and retirement planning expert based in Calgary, Alberta.

Ask a Retirement Expert: Leave your question for Tom Feigs »

Tom Feigs is a fee-for-service financial planner, money coach and retirement planning expert based in Calgary, Alberta.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

A University of Calgary study found that over one-third of senior homeowners worry about affording basic home maintenance, suggesting...

It’s almost impossible to do, but the mindset around spending all your savings can help you make the best of the...

In the likelihood of a protracted conflict, these experts think people in or close to retirement need to review...

Rising costs, debt, and delayed planning are leaving many Canadians unprepared. Here’s what’s behind the gap and how to...

Canadians moving to the U.S. may be able to unlock a locked-in RRSP after 24 months of non-residency—but tax...

Vanguard’s VRIF ETF is tilting toward bonds to provide retirees stable income, balancing caution with a 4% annual payout...

Explore retirement living options—from aging in place to assisted care—and learn how to start supportive, practical conversations with aging...

Retirement planning for couples with a significant age difference calls for realistic projections but also flexibility.

Many adult children know the basics of their parents’ money, but not the details. Discover why full financial visibility...

Learn how inheriting a US IRA or 401(k) works for spouses and non-spouses, including taxes, withdrawal rules, and opportunities...

Hi. I am 56 years of age and in good health. I was employed by Canada Post Corporation for approximately 13 years and transferred the present future value of my pension to a locked in RSP valued at approximately $100 000 presently. I am a resident of Alberta. The fund is, I assume, a LIRA. I am under financial distress. My income is approximately $3500 / month. Can you recommend if I could use some or any of my locked in funds to become more financially secure. I am considering money mentors at this time. Thank you.

I am in Ontario. Retiring with an RPP at age 56 after 26 years of service. I have. I am in a bad situation financially and want to know how I can het access to these funds. I’ve been told LIRA TO LIF conversion and then can access 50 percent of the balance in cash if necessary. I need some direction.

Thank you for your comment. Due to the large volume of comments we receive, we regret that we are unable to respond directly to each one. We invite you to email your question to [email protected], where it will be considered for a future response by one of our expert columnists. For personal advice, we suggest consulting with your financial institution or a qualified advisor.

I don’t think this article answered the questions about tax rules and LIRA’s

Are LIRA with USD dividends subject to the 15% non-resident tax (NRT)?

Thanks