Why the 4% withdrawal rule may not be safe

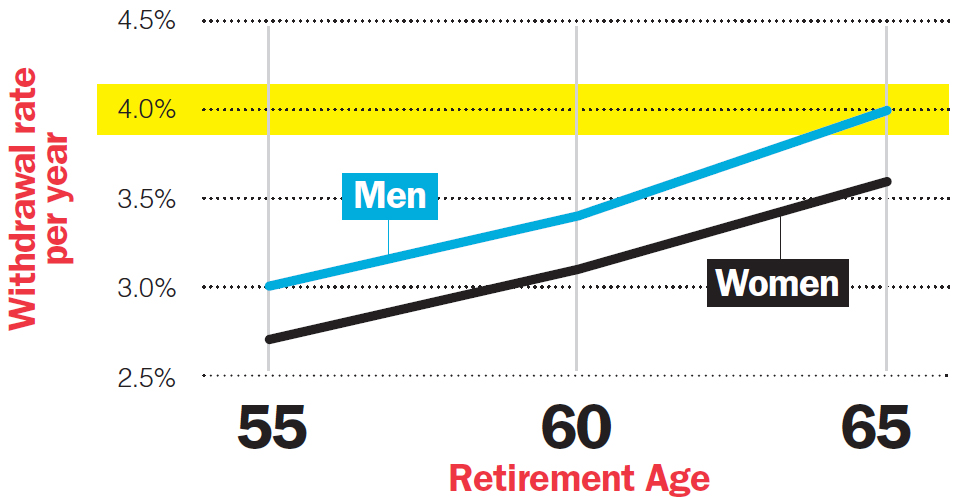

Women should instead budget for 3.6% or less for retirement withdrawals

Advertisement

Women should instead budget for 3.6% or less for retirement withdrawals

Assumptions: Initial withdrawals are increased annually for inflation. Portfolio is invested 50% in stocks and 50% in bonds, and the inflation rate is 2%. Source: M. Milevsky and F. Habib, CANNEX

Assumptions: Initial withdrawals are increased annually for inflation. Portfolio is invested 50% in stocks and 50% in bonds, and the inflation rate is 2%. Source: M. Milevsky and F. Habib, CANNEX

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Experts explore whether financial independence is compatible with long-term travel, highlighting remote work, geoarbitrage, and cost-efficient “bleisure” lifestyles.

Robert has been taking RRIF withdrawals beyond the minimum required amount to gift to his kids and to reinvest...

A University of Calgary study found that over one-third of senior homeowners worry about affording basic home maintenance, suggesting...

It’s almost impossible to do, but the mindset around spending all your savings can help you make the best of the...

In the likelihood of a protracted conflict, these experts think people in or close to retirement need to review...

Rising costs, debt, and delayed planning are leaving many Canadians unprepared. Here’s what’s behind the gap and how to...

Canadians moving to the U.S. may be able to unlock a locked-in RRSP after 24 months of non-residency—but tax...

Vanguard’s VRIF ETF is tilting toward bonds to provide retirees stable income, balancing caution with a 4% annual payout...

Explore retirement living options—from aging in place to assisted care—and learn how to start supportive, practical conversations with aging...

Retirement planning for couples with a significant age difference calls for realistic projections but also flexibility.