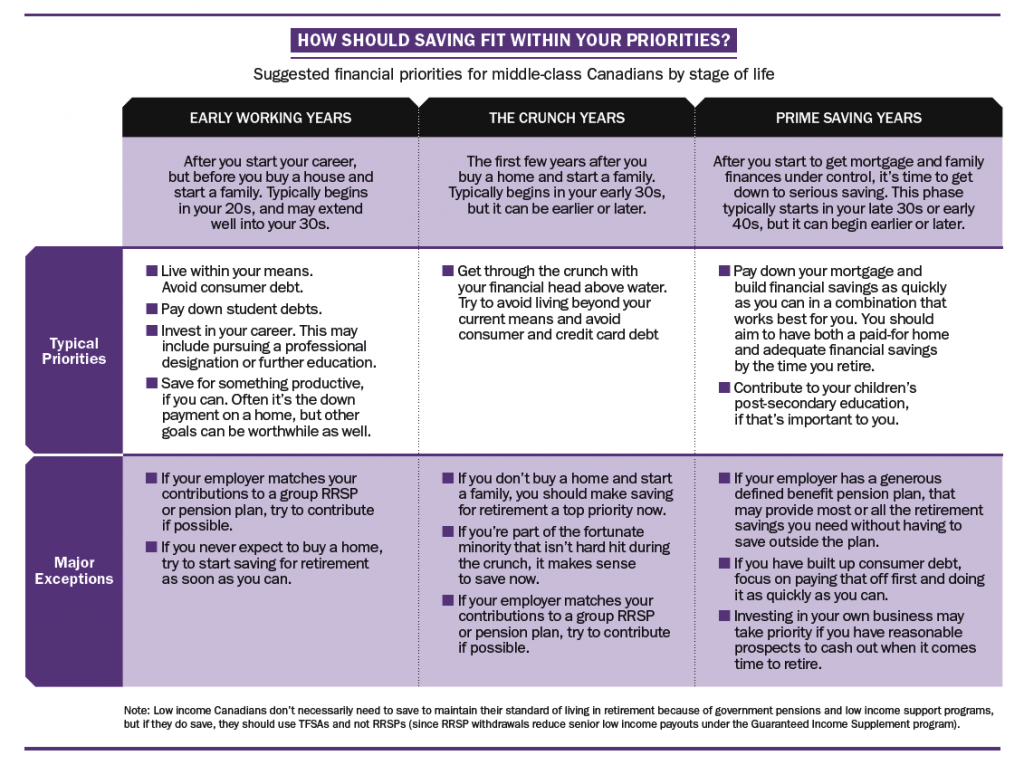

The right time to save for retirement

Your stage of life should help determine when you save

Advertisement

Your stage of life should help determine when you save

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

As the grocer reports sales growth of Canadian products, the clothing retailer plans to increase its U.S. footprint. Here...

Created By

Ratehub.ca

Find out which Canadian robo-advisors offer the lowest fees, best support, top returns, and more, with MoneySense’s 2025 guide.

Once you start RRIFing, how do you make sure you have enough cash, and should you dial down risk?

Nvidia plans to manufacture AI chips in the U.S. for the first time.

Canada’s Consumer Price Index fell in March amid the start of a tariff war with the U.S., the end...

The Alberta Child and Family Benefit is a provincial financial assistance program. Learn who’s eligible for the ACFB...

There are several personal, trust and corporate income-tax-filing extensions for Canadians this year. Which ones apply to you? ...

Whether you have renters in your home or another property, know that the money you make can affect your...