How does earthquake insurance work?

In this guide to earthquake insurance for Canadian homeowners, learn what earthquake protection covers, whether you should buy it, and where you can get it.

Advertisement

In this guide to earthquake insurance for Canadian homeowners, learn what earthquake protection covers, whether you should buy it, and where you can get it.

Earthquake insurance may not be on the minds of many Canadians. And earthquakes may not top the list of likely natural disasters in Canada, but your home could be at risk. According to a study commissioned by the Insurance Bureau of Canada, a major earthquake could devastate communities across the country in the coming years—and such an event is far from unlikely. Read on to learn about earthquake insurance protection, what it covers, what it excludes, and whether you should buy this coverage.

Standard home insurance typically includes personal liability coverage and protection for damage or loss to a home related to a narrow set of perils, like fire or theft. Damage from earthquakes is not included in standard coverage, but you can purchase it as an optional add-on to protect yourself against losses in the event of an earthquake. For example, should your gas main get damaged in an earthquake and start a fire, this kind of insurance would protect your investment. In some cases, you can even apply for living expenses if you’re unable to return home for some period of time.

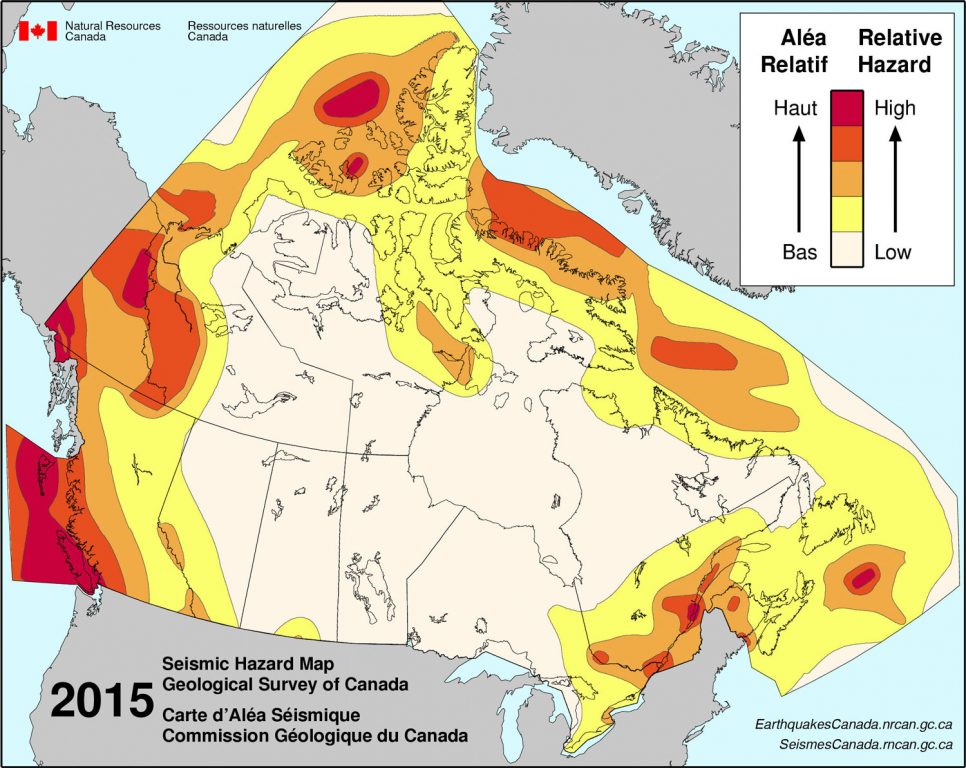

Although earthquake insurance is available to all Canadians, it’s going to appeal especially to those who live in regions most at-risk, like the coast of British Columbia, which government studies indicate has a 30% chance of an earthquake causing significant damage in the next 50 years. The same studies note a 5% to 15% chance for the corridor between Ontario and Quebec. Saskatchewan and Manitoba are among the lowest-risk regions in the country.

The varying risk of an earthquake across the nation is one of many factors for earthquake insurance costs. Policy fees are calculated based on your insurance earthquake zone; the construction of your home, including how many storeys you have; the value of your home and contents; coverage limits; and the deductible.

“Geography plays a significant role in determining the cost of earthquake insurance,” says Jesse Bajwa, customer care manager at Sonnet Insurance Company. “In cities like Toronto or Kitchener, it could be $25 a month on average, whereas in Vancouver, it could be much greater. Vancouver is a combination of lower risk and extremely high risk zones. Lower risk zones could be $250 per year, and the highest risk zones are up to $900 a year or more.”

Also keep in mind that earthquake insurance usually has a higher deductible than other kinds of insurance—generally ranging from 2% to 20% of the damage. On a $400,000 home, your deductible would be $8,000 at 2%, but this rises to a whopping $80,000 at 20%.

“Earthquake insurance has a separate deductible that is expressed as a percentage of the overall cost to replace your home, not as a dollar amount,” Bajwa says. “That said, there’s no deductible applied to the additional expenses associated with finding somewhere else to live, should you have to.”

Watch: Home Insurance & Climate ChangeWhen you purchase earthquake home insurance, you receive protection against loss and damage to your property in the event of an earthquake. But what exactly does that mean? While different policies might include different terms, you can expect (or ask for) coverage for more than the basics.

When you think of earthquake house damage, you probably imagine a cracked foundation. However, that’s likely not the extent of your policy. Earthquake coverage can include, depending upon the insurance provider you go with, loss or damage to your property caused directly or indirectly by the earthquake. That can include snow slide, landslide or other earth movements resulting from an earthquake shock. So, loss or damage caused by wind, hail, rain or snow entering the building can be covered. Your policy might also protect you from fire should a gas line break. And, living expenses might be included if you can’t remain at home during repairs.

It’s important to know what is covered and what isn’t. “Earthquake coverage does not cover loss or damage caused directly or indirectly by a flood of any nature, including waves, tidal waves, tsunamis, high water, waterborne objects, or ice—whether or not caused by the earthquake,” according to Bajwa. For claims against these disasters, you might consider special flood insurance.

It depends on your risk tolerance. If you live in a region with a low probability of experiencing an earthquake—and you’re willing to forgo the peace of mind insurance can provide—the money you would have spent on earthquake insurance might be better put to an emergency fund. On the other hand, if you’re a homeowner in an earthquake hot spot, going without is a gamble. Despite the annual costs and high deductible, this kind of coverage is a smart investment.

Not every insurance company provides earthquake home insurance because of its risk and high payout. Even among the insurers who do, there may be a wide range in policies and costs. A good place to start your research is with your own bank. This will give you a baseline against which to compare other policies and, if you’re satisfied with it, you can enjoy the ease of keeping your products and services consolidated.

The decision of whether to get earthquake insurance is a personal one, but there are guidelines to help make your decision easier and better informed. Let your location, the likelihood of an earthquake in your geographical region, the value of your home and contents, and your personal comfort guide you.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Presented By

Equifax

Credit cards with car rental insurance provide coverage if your rental car is damaged or stolen. These are the...

Drivers in Calgary pay some of the highest average auto insurance premiums in Canada. Here’s how to get and...

A Certified Financial Planner looks at the different strategies to ask your own advisor: Is life insurance the answer?

The Ford F-150 is Canada’s best-selling vehicle, and the Lightning is its all-electric model. See what’s new for 2025,...

VW’s 2025 ID. Buzz adds retro flair to our list of top EVs in Canada. It’s also thoroughly modern...

If you’re looking for a used electric vehicle, put the Mustang Mach-E on your list. This award-winning EV offers...

In this excerpt from Wealthier, authors Daniel R. Solin and Mark McGrath offer practical tips on estate and financial...

If you need high-risk driver insurance in Ontario, here’s how to find it—and what you can do to lower...

As the affordable first car becomes increasingly hard to find for young buyers, auto experts offer these tips for...

What does “Act of God” cover in an insurance policy?

An earthquake is an “Act of God” since God created the earth and the heavens, so why do we have to buy earthquake insurance separately?

I have a commercial building in Toronto near Victoria park subway. Is this area earthquake prone? Should I take earthquake insurance?