Higher rates could spell comeback for 5-year mortgages

Rates are rising with a flood of mortgage renewals coming up. Time to lock in?

Advertisement

Rates are rising with a flood of mortgage renewals coming up. Time to lock in?

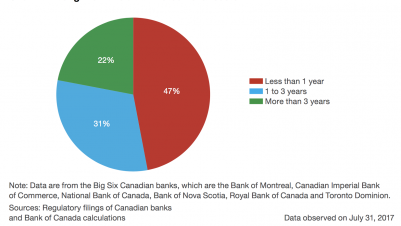

In January, a stress test that goes into effect that includes new rules introduced by the Office of the Superintendent of Financial Institutions (OFSI) on mortgage lending. OSFI is setting a new minimum qualifying rate, or “stress test,” for uninsured mortgages (mortgage consumers with down payments 20% or greater than their home price). The rules now require the minimum qualifying rate for uninsured mortgages to be the greater of the five-year benchmark rate published by the Bank of Canada (presently 4.89%) or 200 basis points above the mortgage holder’s contractual mortgage rate. So no matter how much money a homebuyer puts down to purchase a home, they will have to pass the stress test.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Created By

Ratehub.ca

What to consider when deciding to incorporate a company with friends to buy real estate and more.

Sponsored By

Coast Capital

How much can you afford on your first home? Should you buy or continue renting? We answer these questions...

You have so many options for finding the best mortgage rate for you. Here’s how you can compare some...

Created By

Ratehub.ca

Interest rates, inflation—not to mention tariffs or a recession—can make finances stressful. But keeping a cool head is important....

What is the cost of buying your first home as a Gen Z? Find out the total costs you’re...