Toronto housing bubble: Is it ready to pop?

Toronto’s surging housing market faces uncertainty. Learn about soaring prices, economic factors and the future of affordable home ownership.

Advertisement

Toronto’s surging housing market faces uncertainty. Learn about soaring prices, economic factors and the future of affordable home ownership.

The Toronto real estate market has experienced remarkable growth over the past two decades. The average home price in Toronto surged by a staggering 489% from 2000 to 2022, according to the Toronto Real Estate Board (TRREB). This rapid price growth has raised concerns about the future of affordable homeownership. And with good reason.

For instance, the average Toronto home in 2021 was $1,095,175, while the median household income was $84,000, which equates to a price-to-income ratio of 13. To put that in perspective, the price to income ratio in 2010 was 7.4.

The fact is: wages have not kept up with home prices. For future generations, the goal of owning a home in the Greater Toronto Area is looking more like a pipe dream. This has prompted many who live here to wonder: are we on the brink of a bubble ready to burst, or is this simply a passing phase of the Canadian real estate landscape?

Before delving into the future of Toronto real estate, let’s look at what exactly a “housing bubble” is.

A housing bubble emerges as property prices skyrocket to unsustainable levels, fuelled by speculative investment, where individuals buy with the primary goal of future profits, and by irrational, overly optimistic purchases regardless of intrinsic value. This phenomenon can result in a precarious and artificially inflated real estate market.

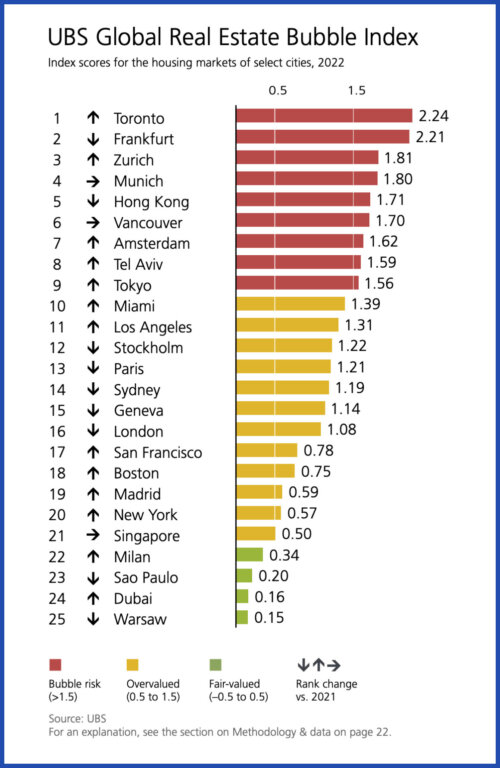

Notably, the UBS Global Real Estate Bubble Index, which assesses housing bubble risks around the globe, ranked Toronto as the world’s highest-risk city in 2022 due to factors like price-to-income and price-to-rent ratios. Although Toronto’s ranking has decreased with a slight dip in home prices since their peak in May 2022, affordability remains a challenge, as prices are still far from reaching a reasonable level.

Since the 2008 financial crisis, interest rates in Canada have closely mirrored those in the United States, remaining historically low. Nevertheless, Canada managed to avert a housing price collapse in 2008 and has outpaced the U.S. and in home prices by a wide margin for the last 15 years.

This really is an insane chart comparing income to house price growth in the U.S vs Canada. pic.twitter.com/Sf5uwEZLGg

— ac_eco (@ac_eco) April 30, 2021

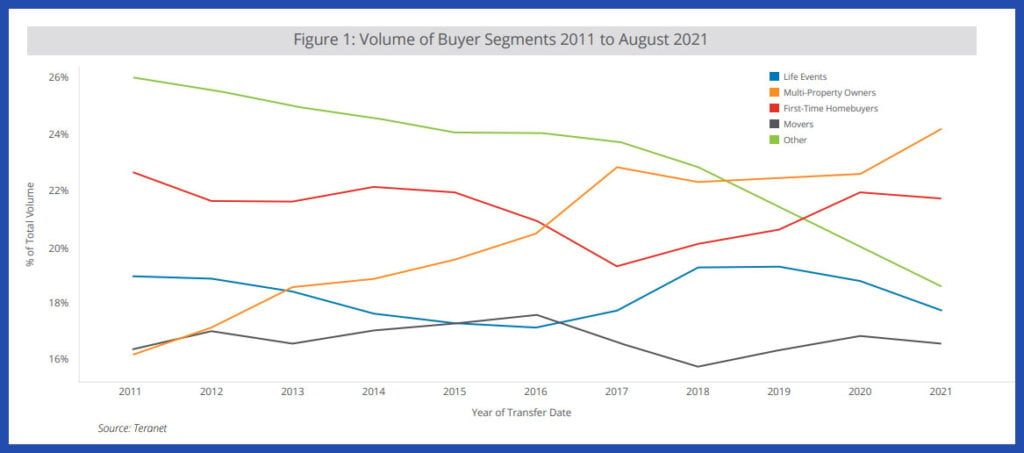

Low-interest rates have not only facilitated first-time homebuyers’ entry into the market but also made ownership an attractive prospect for real estate investors. For example, over half of condos built in Toronto from 2016 onwards are used as investment properties, according to Statistics Canada. The investor segment has been the fastest-growing in Ontario’s real estate market, with multiple property owners accounting for 29% of Toronto’s housing stock, according to a 2022 Teranet report.

There are several compelling factors that point to a future decline in Toronto house prices. With inflation peaking in 2022, the Bank of Canada (BoC) has been attempting to reduce spending by raising the overnight rate. That is meant to make borrowing with loans and mortgages more expensive, and in turn, dampening demand for housing. Once inflation gets to a reasonable level and economic activity slows, the BoC would contemplate lowering rates. However, addressing inflation and its subsequent impact on the economy is a complex, multi-quarter, or even multi-year endeavor.

The latest BoC monetary policy report doesn’t forecast inflation returning to target until 2025. Until then, the central bank may be cautious about lowering interest rates or signalling rate reductions. These actions could potentially reignite economic activity and drive up inflation, including home prices. So, the Bank has reason to maintain the current interest rate level or possibly implement further rate hikes until inflation reaches their defined target or a deemed reasonable level, while not slowing economic activity so much that it ignites a deep recession.

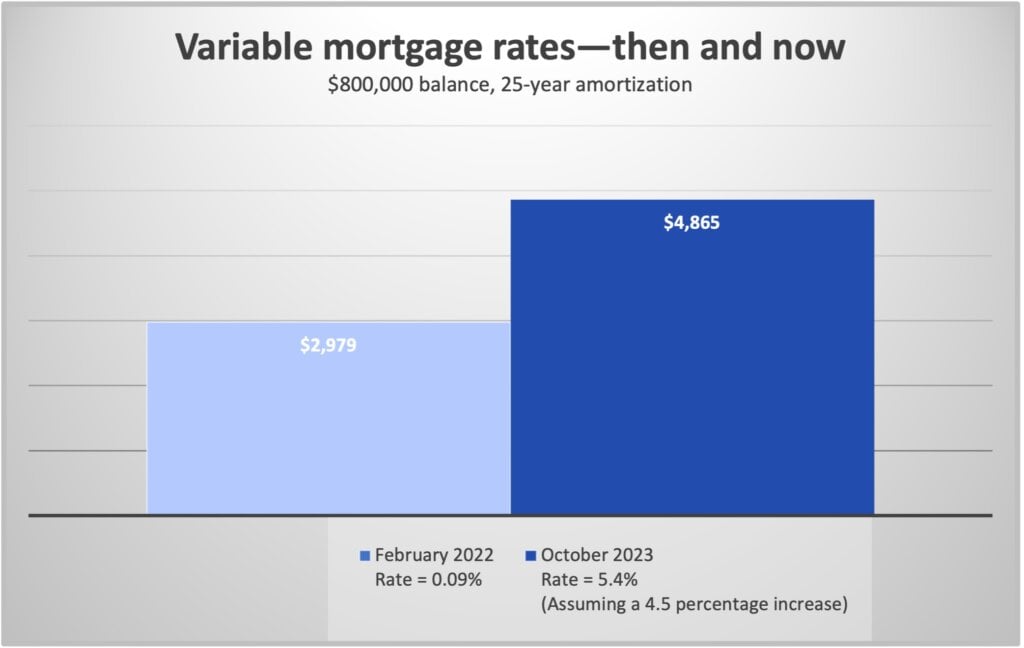

For prospective home buyers, specifically first-time home buyers, the increase in rates means reduced mortgage affordability. (Which is why the FHSA was created, according to the government. More on this type of account below.) For those who purchased homes before the rate hikes started in March 2022 and opted for variable-rate mortgages, the hit has been particularly challenging. Some have witnessed their interest rate climb by as much as 4.5%.

As an example, someone who considered themselves fortunate to secure a 5-year variable rate mortgage at 0.9% in early 2022 may have seen their interest rate soar to 5.4%, leading to a significantly higher required payment. For some, this situation is painful, and for others, it becomes unmanageable. In extreme cases, selling the home they purchased just a few years ago, because they can no longer afford it, may be their only recourse.

Furthermore, demand from foreign buyers has also been curtailed by the Canadian government’s recent ban on non-Canadians purchasing property. Resident investors, who have significantly contributed to home price inflation, are also likely to be affected by higher interest rates and diminishing cash flow.

When will the Toronto real estate bubble burst? While pinpointing the exact timing of Toronto’s potential real estate correction remains challenging, signs of deflation may already be underway. The TRREB has its benchmark prices, designed to estimate the value of a typical home in the area without distortion from outliers. In October, the real estate board reported the benchmark at $1,103,600, indicating a 2.1% dip from September’s $1,127,000.

The prospect of a prolonged period of increased interest rates, driven by the Bank of Canada’s cautious stance amid inflation concerns, alongside reduced affordability, restrictions on foreign buyers, and decreased local investor activity due to higher interest rates, suggests the potential for further market deflation.

Prices are dropping in Toronto, and in Canada as a whole. However, it’s uncertain whether prices will continue to decline or not. The Canada Mortgage and Housing Corporation (CMHC) forecasted home prices to increase in 2024. And according to recent stats from real estate firm Wahl’s 2023 GTA Housing Snapshot Report, underbidding has been rising over the past five months (81% in October). To me, the growth underbidding indicates there are less buyers and lower prices.

Optimists may argue we’ve seen this environment before, with affordability as the ongoing issue. They may contend that the lack of housing supply and the resilience of the housing market will continue to drive up home values. However, certain conditions such as astronomical inflation and rapid interest rate increases have not been seen in decades. This present landscape contains a new set of headlines, setting the stage for potential falling home prices.

While it’s impossible to definitively predict if and when the Toronto real estate market will experience a downturn, it’s evident that skyrocketing prices have created an affordability problem for many.

Simultaneously, though, it disproportionately benefited others, such as property investors. Despite current conditions suggesting diminishing housing demand, including that of investors, policy makers in Canada, including Toronto, must address and moderate this type of demand in the future. Even after interest rates come down.

I’m not saying property investment should be eliminated altogether. It plays a vital role in the housing market, particularly in providing much-needed (affordable) rental housing. Measures like the first home savings account (FHSA), a tax-free registered account aiding first-time home buyers in saving for a down payment, are beneficial. But additional efforts are needed to address the bigger issues in the local housing market. The housing market shouldn’t perpetuate conditions that favour owners of multiple properties (like a second home or vacation property) and even real estate investors at the expense of younger generations striving for affordable housing. Nonetheless, if a decline in house prices is in the cards, it can at least help level the playing field.

Affiliate (monetized) links can sometimes result in a payment to MoneySense (owned by Ratehub Inc.), which helps our website stay free to our users. If a link has an asterisk (*) or is labelled as “Featured,” it is an affiliate link. If a link is labelled as “Sponsored,” it is a paid placement, which may or may not have an affiliate link. Our editorial content will never be influenced by these links. We are committed to looking at all available products in the market. Where a product ranks in our article, and whether or not it’s included in the first place, is never driven by compensation. For more details, read our MoneySense Monetization policy.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Whether you have renters in your home or another property, know that the money you make can affect your...

Here’s how proposals from the NDP, Liberals, Conservatives and Green Party could affect your cash flow—and maybe help decide...

What to consider when deciding to incorporate a company with friends to buy real estate and more.

Sponsored By

Coast Capital

Can you retroactively change the valuation of a rental property before selling it to reduce capital gains tax in...

On the heels of a pandemic boom, the recreational real estate market has slowed. But property prices are still...

How much can you afford on your first home? Should you buy or continue renting? We answer these questions...

When is capital gains tax payable on the sale of property? And at what rate are capital gains taxed?...

Everything went up not even the real estate, 1 I phone around $2000 cooking oil $20/4 liter,gas close to$2

If we compare with those things still acceptable

Good article

Some day we are all gonna find out this bubble came from the real estate market and private equity raising prices via hidden bids and backdoor handshakes