Millionaire by age 41

Gerry and Fiona make a middle-class $82,000 a year, but thanks to some heavy saving and savvy investing, they’re already worth more than $1.5 million. Do they have enough to retire in middle age?

Advertisement

Gerry and Fiona make a middle-class $82,000 a year, but thanks to some heavy saving and savvy investing, they’re already worth more than $1.5 million. Do they have enough to retire in middle age?

Gerry and Fiona Garda of Vernon, B.C., have one big dream—to retire now. “I’ve been investing since I was 16 years old,” says Gerry, 41, an administrative assistant with the B.C. Ministry of Transportation. “In the early years I made and lost big money, but I always stuck with it—and it’s paid off. It’s been an exhilarating ride.”

Gerry and Fiona (we’ve changed their names to protect their privacy) have stock investments valued at $1.27 million and a pair of rental properties. After paying off their debts, their net worth would be well over a million. In fact, Gerry thinks he and Fiona can quit their jobs today and live off the income from their investments for the rest of their lives.

“I just finished a sabbatical from my job and it’s given me a taste for life outside the office,” says Gerry, who spent most of his year off being a stay-at-home dad to his two-year-old daughter, Phoebe. “I’m ready to move on to a new phase of my life.”

There is one wrinkle, however—they have another baby due in September. “Fiona and I have always lived on less than one income,” says Gerry. “But we know kids are expensive. Can we continue living frugally with two kids? We’re not sure.”

Fiona, who is 36, earns $22,000 a year as a part-time social worker, while Gerry earns $60,000. In their spare time, they do volunteer work with the cancer society, several local charities, and with a girls’ orphanage in Costa Rica. “If we have enough money, why not just quit our jobs and do more of what we love—charitable work?” says Fiona.

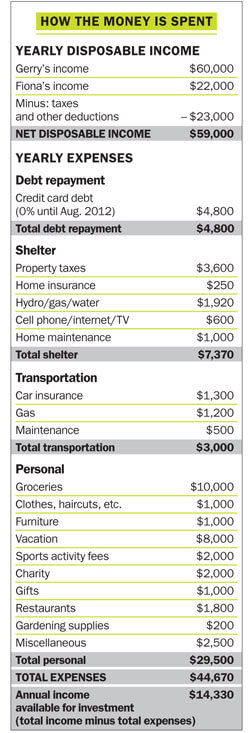

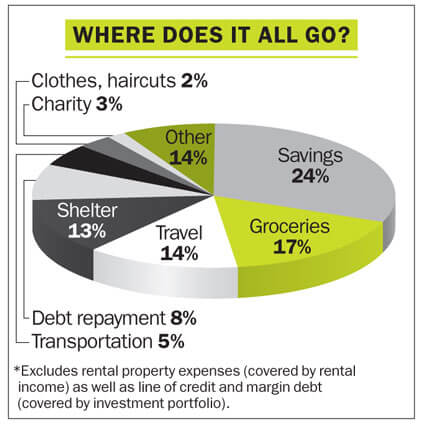

Gerry has run the numbers and feels his family can live on $45,000 in after-tax income a year. But he’s not sure their investments will be able to generate enough money to cover their expenses for the rest of their lives. “I don’t mind working part-time a few more years if I have to,” says Fiona. “But I really think we may have enough assets to provide us with a good income to old age.”

Even if they have enough, there’s another problem: the couple’s portfolio is full of risky, volatile stocks. Gerry knows he needs to restructure his portfolio so that it is more conservative and tax-efficient. “I know I’m not the one to do that,” says Gerry. “I know nothing about conservative portfolios. It will be our biggest challenge.”

One of their strengths, on the other hand, is the fact that the Gardas have more than their stock portfolio to depend on in retirement. By the time Gerry turns 55, he expects to have paid off the mortgages on his two properties, which will provide $20,000 a year in rental income. He’ll also start collecting a pension of $1,600 a month, earned during his years with the provincial government. But even with all that, Gerry is apprehensive. “I think we’ll need $45,000 a year, but I could be wrong. We need to be certain we’re really ready to go it alone before we leave our jobs. Can you help us?”

Fiona has always been good with money. She grew up in Vancouver, where her mother was a nurse and her dad a car salesman. “My parents’ biggest investment was their home, which they bought in Vancouver for $60,000 in 1976,” says Fiona. “It’s worth $1.2 million today.”

Fiona worked part-time through high school at the local McDonald’s before enrolling at university in Victoria in 1992. During her four years there, she took part-time jobs while completing a bachelor’s degree in social work. By the time she graduated, she had $20,000 in the bank. “I never had student debt,” says Fiona. “I worked constantly, lived frugally and grew my savings the whole time I was at university.”

Gerry’s early home life wasn’t as comfortable. He was born in Regina, and when he was three his father left, leaving his mother to raise both him and his older brother, Matthew. She remarried when Gerry was 12. “Mom worked as a waitress during the day and attended university at night. When I was 10, she graduated with a teaching degree. She taught us kids to be industrious.”

At nine, Gerry had his own paper route. In high school he worked evenings at the local Woolco store and read investment books voraciously. “I just wanted to make money,” remembers Gerry. “Those were the days when you had to call your broker to buy and sell a stock. I wasn’t old enough, so I had my brother place the trades for me.”

Gerry studied for a couple of years at the University of Regina, but quit before earning his degree. Instead, he went to technical school where he studied resource management. All along, Gerry kept investing and his portfolio grew to about $18,000 in 1994. Then the bottom fell out. “I had all my money in gold stocks,” he says. “When the market turned, I lost everything. Even today, I won’t touch commodity stocks.”

In 1995, Gerry got a job with the Ministry of Transportation in Vernon, and with a small down payment he bought a house. That’s also when he met Fiona at a friend’s barbecue. A year later they moved in together. Gun-shy from his losses, Gerry temporarily gave up stock picking and concentrated on saving instead. “Fiona and I parked every penny we made in mutual funds for six years, and we had $150,000 saved by the time I turned 30. We were cheap. We didn’t own a car, we grew our own vegetables, biked everywhere and bought very little furniture.”

In 1997, the Gardas married and received a cash gift of $45,000 from Gerry’s mom. They invested the money, along with $20,000 of Fiona’s savings, in their home and the two rental properties they still own today.

It wasn’t until 2001 that Gerry decided to sell the $150,000 worth of mutual funds that he and Fiona had accumulated and give stock investing another try. “I’m drawn to small caps—especially when everyone hates them,” says Gerry. “If their price drops, I buy more. As long as the stock’s main narrative hasn’t changed, I’ll hold on.”

Gerry is a focused investor. He only invests in sectors that he understands—communications, technology, and health care—and he never owns more than 10 stocks at a time. Most importantly, he stays engaged. “I spend three hours a day doing research. I ignore what’s happening in the daily news—that’s just noise.”

Gerry is a focused investor. He only invests in sectors that he understands—communications, technology, and health care—and he never owns more than 10 stocks at a time. Most importantly, he stays engaged. “I spend three hours a day doing research. I ignore what’s happening in the daily news—that’s just noise.”

Right now, Gerry’s portfolio includes Cisco, Intel and RIM, as well as a couple of “cloud computing” companies that Gerry believes are the way of the future. “The new direction for tech stocks is in its infancy,” he says. “Tech stocks are just starting a new cycle of growth.” He’s quite happy to wait out a few ups and downs, as long as he knows he’ll never have to sell in a panic. “If I lost all my stock money tomorrow, I wouldn’t worry, but that’s because I earn a good salary. But I can’t invest this way if I don’t have a regular salary. Now that’s risky.”

In 2006, Gerry and Fiona discovered a new love: giving back to their community. They also have a connection with a special charity. “We were in a bar in a tiny town in Costa Rica,” says Fiona. “We asked what there was to see nearby, and one of the locals took us to a girls’ orphanage. We were hooked.”

The Gardas donate about $2,000 annually to the orphanage—enough to send a couple of girls to university every year. “Do you know how rewarding that is—knowing you can change someone’s life for so little?” says Fiona. “It’s a fantastic feeling.”

If the couple retires now, their big concern will be having enough income to pay expenses for the next 15 years, until they can get by on Gerry’s pension and their rental income. “For the near future, our investments have to do all the heavy lifting,” says Gerry. “That’s crucial for our plan to work.”

If the couple retires now, their big concern will be having enough income to pay expenses for the next 15 years, until they can get by on Gerry’s pension and their rental income. “For the near future, our investments have to do all the heavy lifting,” says Gerry. “That’s crucial for our plan to work.”

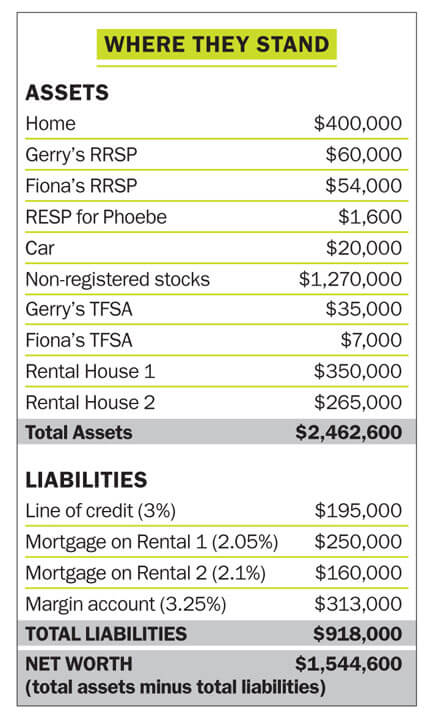

The Gardas are carrying some large debts. Their mortgage is structured as a $195,000 line of credit, which they service with the income form their stock portfolio. They also owe $313,000 in a margin account at 3%. Their two rental houses have mortgages totalling $410,000, which will be paid off by the time Gerry turns 55.

The couple has always kept their expenses low. With both of them working, they save more than $14,000 a year, which goes directly into RRSPs and Gerry’s stock portfolio. “We’re big do-it-yourselfers—renovations, cooking and gardening,” says Gerry. “It keeps costs down, savings up and us busy.”

One thing is certain: when the couple does retire, Gerry won’t miss his job one bit. “I’m just going through the motions now,” he says. “I want to do something more meaningful with my life. We’re keeping our fingers crossed, hoping a new life is just waiting for us to grab it.”

What the experts say

What the experts say

Karin Mizgala, CEO of Money Coaches Canada, says the Gardas will be relieved when they crunch the numbers. “Over the long run, their income will cover their expenses.” The key, she says, is the couple’s frugal lifestyle. “The less you spend, the earlier you can retire,” Mizgala says. “But few people ever consider a more frugal life until I walk through the numbers with them. They have become convinced by the media that they need $2 million before they can retire. For most of us, it’s much, much less than that.” Here’s what the Gardas should do.

Calculate what they have now

Once they pay off the margin loan and their line of credit, the Gardas’ investment accounts will be valued at about $920,000. This is the money they will have to depend on, at least until age 55, to fund almost all of their $45,000 in annual after-tax expenses.

Start deleveraging

The couple cannot retire with a leveraged stock portfolio. “They are in danger territory,” says Jim Otar, a Certified Financial Planner and author in Toronto. “Their exposure to risk is highly amplified.” Otar notes that a not-so-unusual 40% correction in their holdings means the couple would lose 62% of their net investments. “They should pay off all their debts before quitting their jobs,” says Otar.

Give the portfolio a makeover

Selling their stocks may take the Gardas up to three years, because it will trigger capital gains or losses. The Gardas need to spread these over two or three years to minimize taxes. They should get help from a tax accountant to do this.

Then the portfolio needs to be rebuilt. Laura Wallace, vice-president and portfolio manager with Scotia Asset Management in Toronto, recommends a mix of 50% equities and 50% fixed income. To ensure regular income, inflation protection and tax-efficiency, the portfolio should include at least 20 dividend-paying stocks, as well as government and corporate bonds with staggered maturities. Most of the dividend stocks should be Canadian, as the dividends get favourable tax treatment. “Such a portfolio can be expected to generate an after-tax return of about 5%—enough to cover their annual expenses,” says Wallace.

Consider working six more years

Although Gerry and Fiona could probably retire today, the experts hesitate to recommend this strategy. That’s because as their kids get older, $45,000 in income may not be enough. “The likelihood that expenses will increase substantially after the kids turn five is high,” says Wallace.

That’s why if Gerry really wants to retire now, Fiona should consider keeping her part-time job for a few more years. “They should take only what income they need from the portfolio while Fiona is still working.” If Fiona is bringing in $20,000 after taxes, they will only have to draw about $25,000 from their investments, says Wallace. “This will provide a good financial cushion.”

Otar is more cautious. He’d like to see both Gerry and Fiona work six more years, until Gerry is 47. “If the couple is unlucky enough to experience a worst-case scenario in the coming years—higher inflation, a steep stock market decline, a crash in the housing market—their investments will take a big hit,” he says.

If the Gardas take Otar’s advice, then at age 55 their investment portfolio should still be worth about $1,000,000—even with $45,000 to $50,000 in annual withdrawals over those eight years. At that time, the couple will also have at least $1,600 in monthly income from Gerry’s government pension (a bit more if he works until 47) as well as $20,000 annually from their then fully paid-off rental houses. With CPP payments at 60, that should be more than enough to last the Gardas well into their 90s.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Now’s the time to help pay for their education

It's time to discuss how they can start saving for larger purchases

Now's the time to toss the piggy bank and open a bank account instead

It's important to start teaching your kids about money early

Breaking your mortgage to get a better interest rate could save you thousands of dollars. Here’s what you should...

Has your home insurance premium gone up? We get to the bottom of why rates are on the rise...

You've poured lots of money into your RRSP. How do you get it out without paying a fortune in...

Thinking about a career change or worried you won’t escape the next round of layoffs? Follow our tips to...

You can do more than survive in Canada—choose where to put your wisely and over the long term you'll...