Must-knows to file this year’s taxes

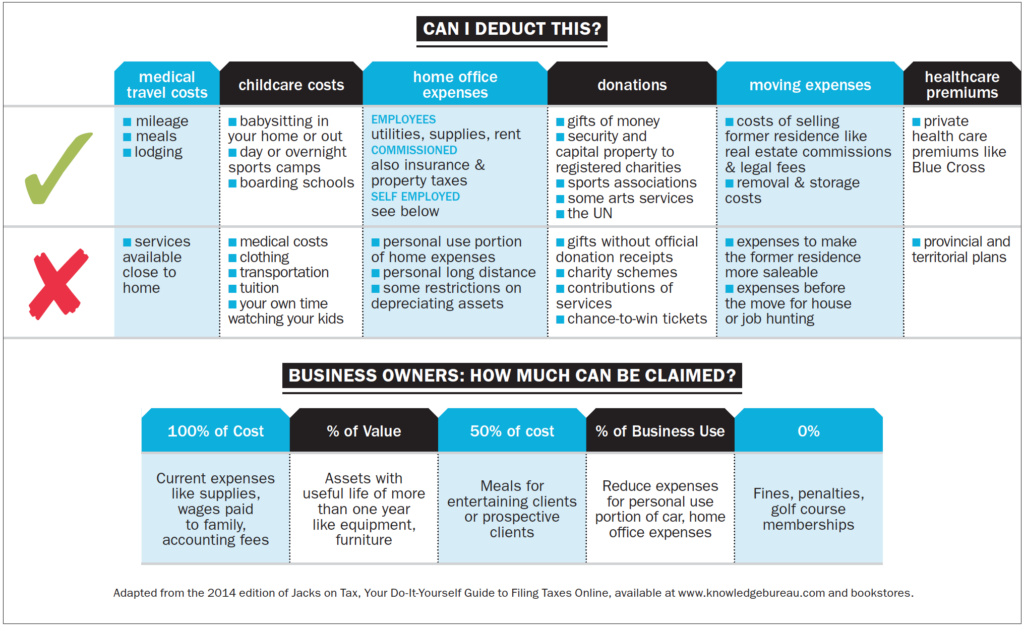

Here are the tax changes affecting families plus info on what you can, and can't, deduct.

Advertisement

Here are the tax changes affecting families plus info on what you can, and can't, deduct.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

There’s more than one way to optimize your income after retiring. Some strategies can boost wealth, and others may...